Netflix delivers solid earnings amid Warner Bros. uncertainty

Netflix added more money, more members, and more ambition this quarter. It showed off its scale and asked for patience. But investors offered neither.

Tuesday after the bell, the company mostly (and modestly) beat fourth-quarter 2025 expectations, hit 325 million paid memberships, and laid out an aggressive 2026 plan — including sharply higher margins — but the stock fell close to 5% after hours, underscoring how tightly the company’s future is tied to ad growth and a looming Warner Bros. Discovery deal. The numbers are clean. The narrative isn’t.

Because while Netflix’s latest earnings report delivered the usual markers of success — growth, profit, scale — the subtext was about what happens when a streaming giant starts behaving less like a disruptor and more like a consolidator with a side business to build. While Netflix’s long-term margin story strengthened, near-term costs get heavier first — including higher content amortization and deal-related expenses that are front-loaded into early 2026. So the destination looks attractive, but investors are looking at a path to get there that looks bumpy.

Revenue came in at $12.1 billion, up 17.6% year over year, and a one-cent earnings per share beat of $0.56; net income came in at $2.42 billion, and operating margin was 24.5% for the quarter. Netflix also reaffirmed its longer-range posture, guiding to $50.7 billion–$51.7 billion in 2026 revenue and a 31.5% operating margin, even after acquisition-related costs. On paper, that’s the profile of a company that believes it has matured into a durable cash machine.

But markets aren’t just grading this quarter in isolation. Investors are weighing whether Netflix’s next chapter — ads, scale, and a potentially balance-sheet-stretching acquisition — adds up to a story that deserves fresh multiple expansion right now. The stock’s answer, at least in the first 20 minutes, was a polite but unmistakable “not yet.”

Ads are no longer the footnote

Netflix disclosed that 2025 ad revenue topped $1.5 billion, more than 2.5 times higher than the prior year, and the company said it expects ad revenue to roughly double again in 2026. That’s not an experiment or a rounding error. That’s a second engine the company is comfortable modeling in public.

What Netflix is really selling here isn’t just ad dollars, but optionality. Ads give the company more room to push pricing without triggering churn, more leverage in content negotiations, and a way to monetize engagement that doesn’t depend on adding tens of millions of new subscribers every year. In a world where pure subscription growth inevitably slows, advertising is how Netflix keeps the growth math feeling elastic.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Smuckers Sales Rise, Losses Deepen And the Stock Still Falls

Barrick's 2025 Performance: Achieving New Highs Amidst a Changing Gold Market

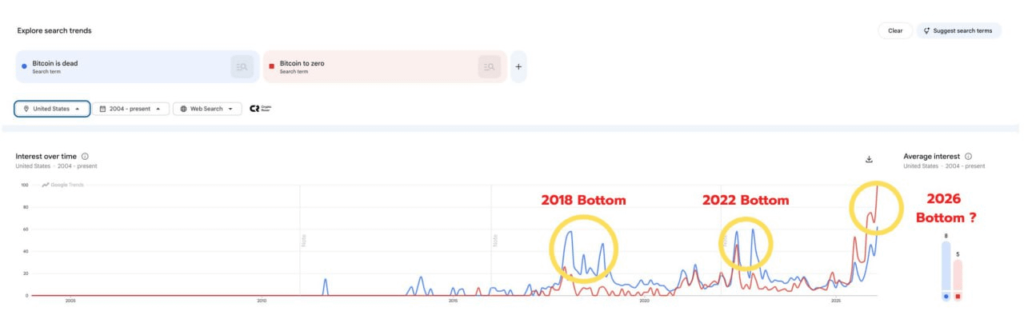

Bitcoin: Google Trends Signals a Shift in User Behavior

Egrag Crypto to XRP Investors: Just Do It “You Must Be Buying, Not Crying”