New ICO Test

This article delves into how the launches of TROVE and RNGR reflect the evolving trends in crypto fundraising and the mechanisms of trust investors rely on during allocation processes.

Written by: Prathik Desai

Translated by: Block unicorn

At the start of this year, the crypto sector saw several major events unfold. A new round of tariff wars between the US and Europe once again pushed uncertainty to the forefront. Shortly after, there was an unprecedented wave of liquidations last week.

Tariffs were not the only negative news at the start of the year. Several recent crypto fundraising events over the past week have given us ample reason to revisit topics that were hot in the crypto community nearly a decade ago.

Those familiar with crypto history might believe the industry has moved beyond the fundraising era of 2017. While crypto fundraising has changed in many ways since then, last week’s two fundraising events raised many important questions—some longstanding, others entirely new.

Both Trove and Ranger’s fundraising rounds were oversubscribed, but there was none of the 2017-style, Telegram-based countdown hype. Even so, the process reminded the community that fairness in allocation is paramount.

In today’s story, I take a deep dive into how the launches of TROVE and RNGR reflect trends in crypto fundraising and the trust mechanisms investors depend on during allocation processes.

Let’s get to the point.

Trove’s fundraising was recent, held from January 8 to 11, and ultimately raised over $11.5 million—more than 4.5 times its original goal of $2.5 million. The oversubscription clearly signaled strong investor support and confidence in the project, which was positioned as a perpetual exchange.

Trove initially planned to build its project on Hyperliquid to leverage the ecosystem’s permanent infrastructure and community advantages. However, just days after fundraising was completed and before the token generation event (TGE) began, Trove suddenly changed its mind, announcing it would launch on Solana instead of Hyperliquid. This disappointed investors who had placed their trust in Trove based on Hyperliquid’s reputation.

This move unsettled investors and caused confusion. The situation worsened when another detail came to light: Trove’s official team stated that about $9.4 million of the raised funds would be retained for the redesigned plan, with only a few million dollars refunded. This was yet another red flag.

In the end, Trove had to respond.

“We’re not going to take the money and run,” they stated on X.

The team insisted that the project remained focused on building, though the approach had changed.

Even without making any assumptions, one thing is clear: it’s hard to imagine that backers weren’t treated in a way that was unfair and retroactive. Although the funds were originally promised to an ecosystem—Hyperliquid—with a single technological path and an implicit risk profile, the revised plan required them to accept a different set of assumptions without reopening the terms of participation.

It’s like changing the rules of a game for one player after the game has already started.

But by then, the damage was done, and the market punished the loss of confidence. The TROVE token plunged over 75% within 24 hours of its launch, erasing nearly all of its implied valuation.

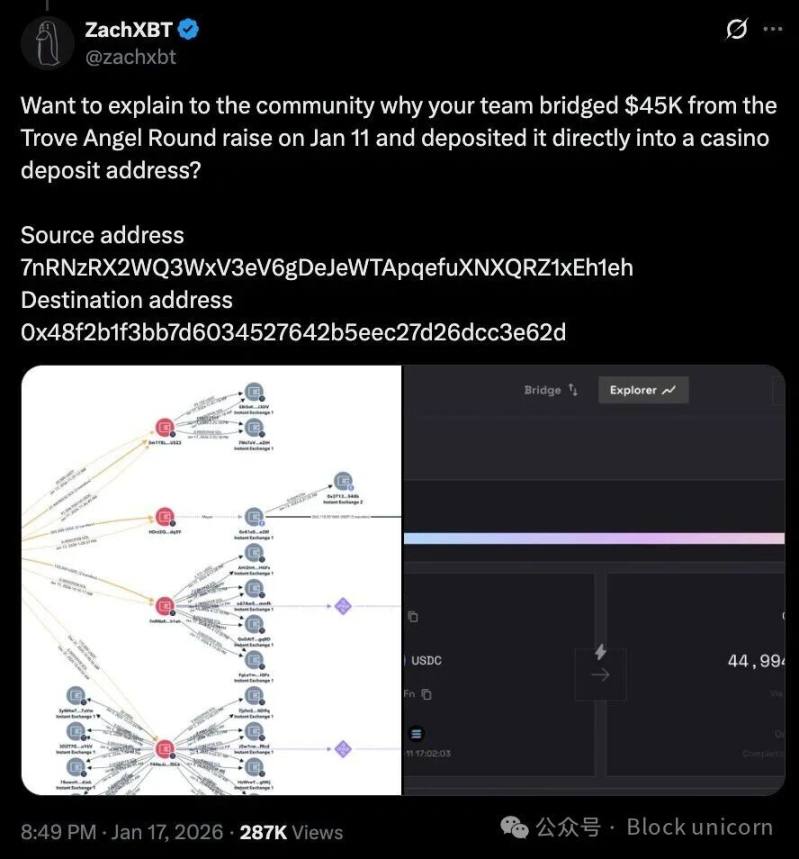

Some in the community stopped relying solely on intuition and began analyzing on-chain transaction dynamics. Crypto investigator ZachXBT discovered that about $45,000 worth of USDC from the angel round ended up on prediction market platforms and even flowed into an address linked to gambling.

Whether this was an accounting oversight, poor fund management, or an actual security risk, remains undetermined. Many users criticized the refund process, noting that only a small portion of users entitled to refunds received them on time.

Throughout all of this, Trove’s statements failed to reassure investors who felt betrayed. Although the statement emphasized that the project would continue—building a perpetual exchange on Solana—it did not adequately address the economic concerns raised by the transition. The statement did not provide updated details on how retained funds would be deployed and managed, nor did it offer any further explanation about the refund roadmap.

While there’s no concrete evidence that the team’s transition was related to misconduct, this incident shows that once trust in the fundraising process erodes, every data point becomes subject to suspicion.

What makes the situation even more untenable is the way the team handled things after the fundraising ended.

Oversubscription effectively shifted both capital and bargaining power to the developers. Once the team pivoted, investors were left with few options besides exiting on the secondary market or exerting public pressure.

In some respects, Trove’s fundraising approach resembled many earlier crypto fundraising events. While its mechanisms were clearer and the infrastructure more mature, both cycles shared a common issue: trust. Investors still had to rely on the team's judgment, with no clear processes to fall back on.

The fundraising for Ranger, which took place just days earlier, provides a sharp contrast.

The Ranger token sale took place from January 6 to 10 on the MetaDAO platform. The platform required teams to predefine key fundraising and allocation rules before the sale began. Once launched, those rules could not be changed by the team.

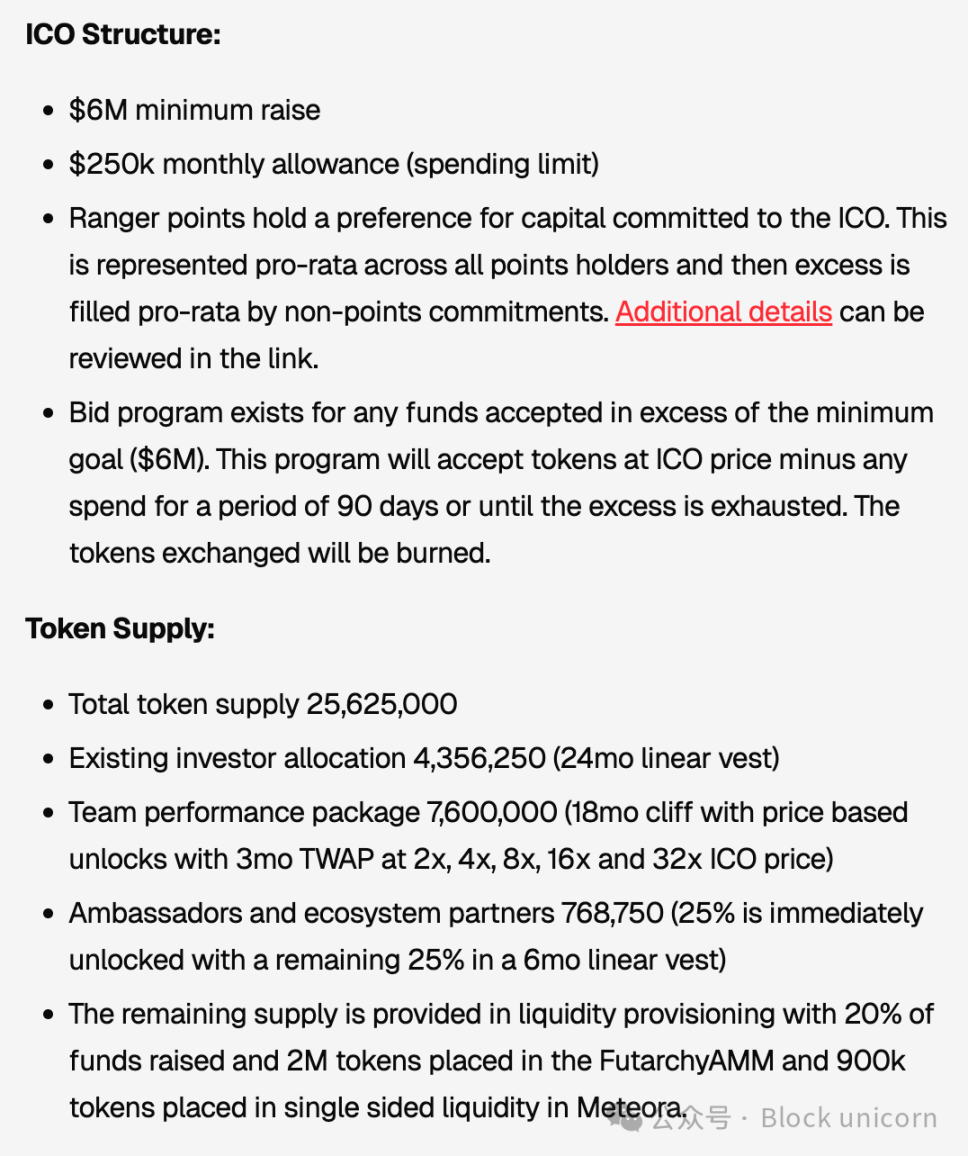

Ranger sought to raise at least $6 million and sold about 39% of its total token supply through a public sale. Like Trove, the sale was oversubscribed. But unlike Trove, MetaDAO’s restrictions meant the team had prepared for this scenario in advance.

When the token sale was oversubscribed, proceeds were deposited in a treasury managed by token holders. MetaDAO’s rules also stipulated that the team could only access a fixed amount of $250,000 from the treasury each month.

Even the allocation structure was more clearly defined. Public sale participants received full liquidity at the token generation event, while presale investors faced a 24-month linear vesting schedule. Most of the tokens allocated to the team would only unlock when the RNGR token hit specific price milestones. These milestones—such as 2x, 4x, 8x, 16x, and 32x the issuance price—would be measured using a three-month time-weighted average, with at least 18 months before any unlocks.

These measures show that the team imposed limitations within the fundraising structure itself, rather than relying on investors to depend on the team’s discretion post-funding. Control over funds was partially delegated to governance rules, and any team proceeds were tied to long-term market performance, thus protecting investors from the risk of early-stage capital flight.

Still, concerns about fairness remain.

Like many modern crypto fundraising projects, Ranger used a proportional allocation model in the event of oversubscription. Theoretically, this means everyone should receive tokens in proportion to their contributions. However, research by Blockworks shows this model often favors those capable of oversubscribing. Smaller contributors typically receive a disproportionately small token allocation.

But there is no simple solution to this.

Ranger attempted to address the issue by reserving a separate allocation pool for users engaged in the ecosystem before the sale. This mitigated the impact but did not eliminate the dilemma between broad token access and meaningful token ownership.

The data from Trove and Ranger together show that crypto fundraising, nearly a decade after its initial boom, remains constrained in many ways. Early models relied heavily on Telegram announcements, narratives, and market hype.

Newer models rely on structured mechanisms to demonstrate restraint: vesting schedules, governance frameworks, fund management rules, and allocation formulas. These tools, often mandated by platforms like MetaDAO, help restrict the issuing team’s discretion. However, these tools can only reduce risk—not eliminate it.

These events raise key questions that every crypto project team will need to address in future fundraising rounds: “Who decides when the team can change the plan?” “Who controls the capital after fundraising?” “What mechanisms are available to contributors when expectations aren’t met?”

These incidents raise some critical questions that every crypto project team will need to answer in the future: “Who decides when the team can change the plan?” “Who controls the funds after fundraising is complete?” “When expectations are not met, what recourse do contributors have?”

However, the Trove case indeed needs to be rectified. Changing the project’s launch chain is not a decision that can be made overnight. The best way to make amends is for Trove to properly manage its relationship with investors. In this case, that might mean full refunds and a renewed sale under the revised assumptions.

Although this is the best solution, Trove still faces considerable challenges in achieving it. Funds may already be committed, operational costs may have been incurred, and partial refunds may have already been issued. Undoing these actions at this stage could bring complex legal, logistical, and reputational issues. But these are the costs of remedying the chaos that led to the current situation.

Trove’s next steps may set a precedent for crypto project fundraising this year. The market is returning to a more cautious stage, one where participants no longer mistake oversubscription for consensus, nor equate participation with protection for backers. Only robust systems can provide a trustworthy (even if not foolproof) crowdfunding experience.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Open USD stablecoin backed by 140 firms launches on Ethereum with Visa, Mastercard, BlackRock

Is Walsh "all talk"? U.S. Treasuries are not convinced

The Federal Reserve has held rates steady for the seventh consecutive month, and the U.S. Treasury market responded accordingly: since Waller is not raising rates, the bond market is tightening on its own. The yield on two-year U.S. Treasury bonds has declined, indicating the market believes there is little chance of a rate hike in the near future; meanwhile, the yield on 30-year bonds surged 14 basis points in a single day to 5.23%, reaching a 19-year high, signaling that the market is demanding a higher inflation risk premium.

Robinhood Sank After a Blowout Quarter: Rebound, or a Slide to $76?

Meta (META.US)'s AI Gamble: Q2 Revenue Hits New High, But Profit Pain Persists as Free Cash Flow Plummets to Four-Year Low

After the market closed on July 29, Meta Platforms (META.US) released its financial report for the second quarter of 2026 ending June 30. In after-hours trading on Wednesday, Meta's stock price once plunged nearly 10%.