Primoris (NYSE:PRIM) Surprises With Strong Q4 CY2025 But Stock Drops

Infrastructure construction company Primoris (NYSE:PRIM)

Is now the time to buy Primoris?

Primoris (PRIM) Q4 CY2025 Highlights:

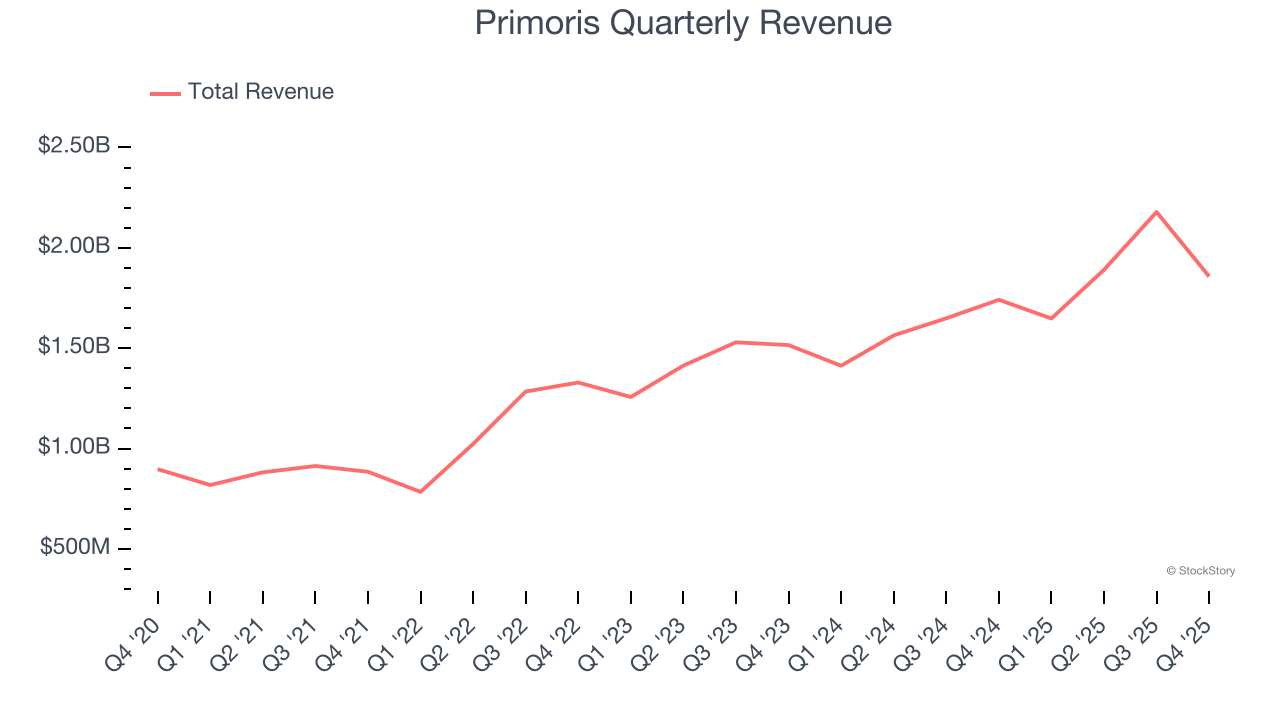

- Revenue: $1.86 billion vs analyst estimates of $1.80 billion (6.7% year-on-year growth, 3.3% beat)

- Adjusted EPS: $1.08 vs analyst estimates of $0.99 (8.9% beat)

- Adjusted EBITDA: $108.2 million vs analyst estimates of $104.7 million (5.8% margin, 3.4% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.90 at the midpoint, beating analyst estimates by 1%

- EBITDA guidance for the upcoming financial year 2026 is $570 million at the midpoint, above analyst estimates of $565.3 million

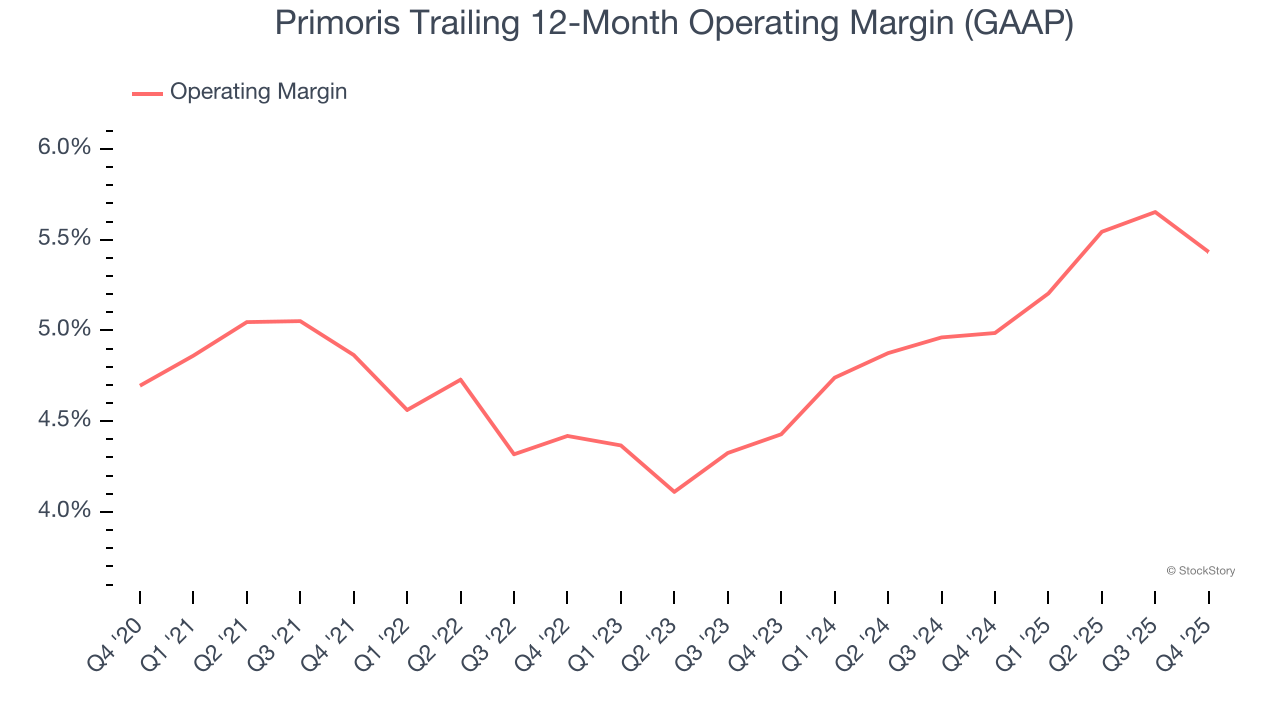

- Operating Margin: 4.2%, in line with the same quarter last year

- Free Cash Flow Margin: 6.5%, down from 15.5% in the same quarter last year

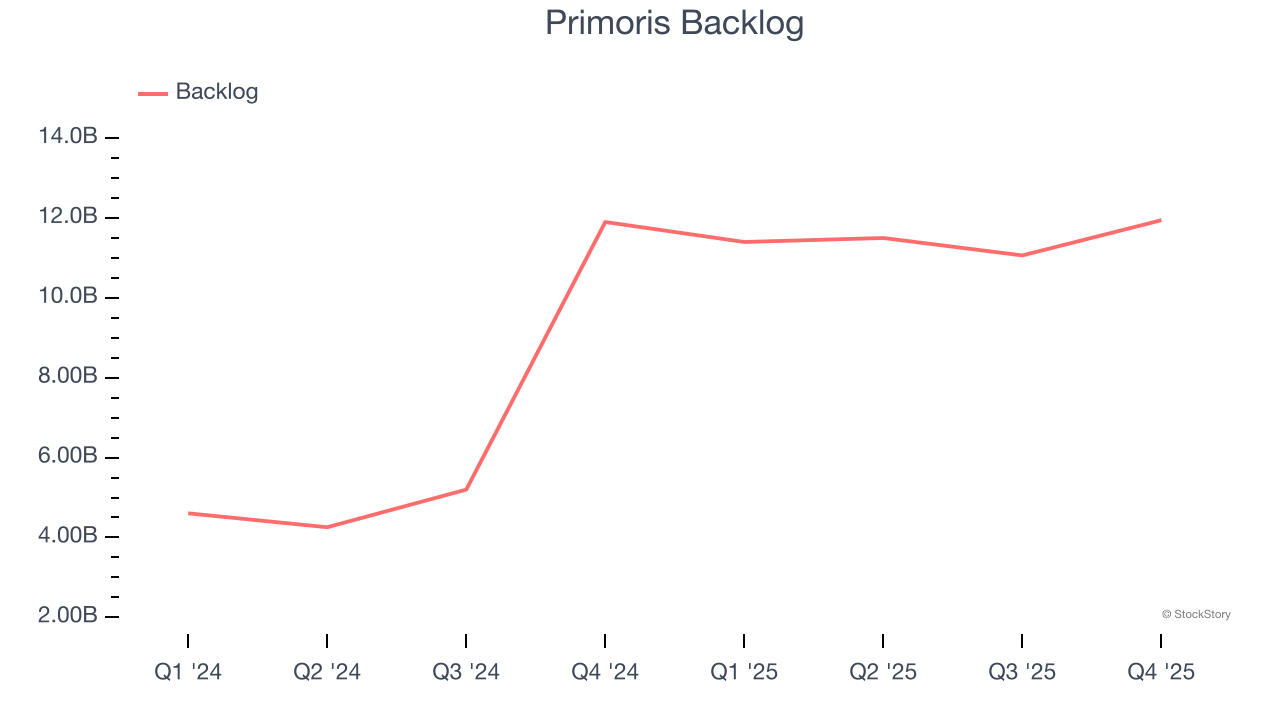

- Backlog: $11.95 billion at quarter end, in line with the same quarter last year

- Market Capitalization: $9.15 billion

“Primoris concluded another year of profitable growth in 2025, delivering record revenue, earnings, and backlog, while putting us ahead of schedule in achieving our multi-year goals. We also strengthened our balance sheet and liquidity position, which will enable us to allocate capital toward opportunities to create further value for Primoris and its stakeholders,” said Koti Vadlamudi, President and Chief Executive Officer of Primoris.

Company Overview

Listed on the NASDAQ in 2008, Primoris (NYSE:PRIM) builds, maintains, and upgrades infrastructure in the utility, energy, and civil construction industries.

Revenue Growth

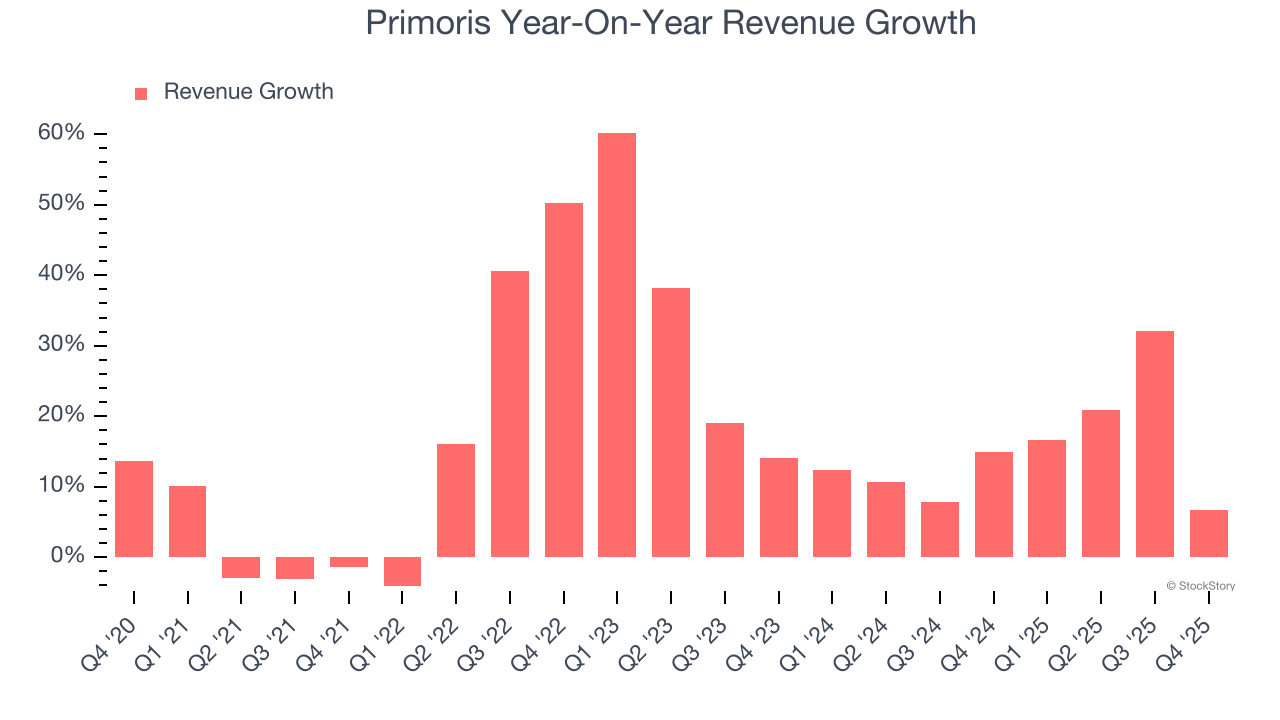

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Primoris grew its sales at an incredible 16.8% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Primoris’s annualized revenue growth of 15.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Primoris’s backlog reached $11.95 billion in the latest quarter and averaged 108% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Primoris’s products and services but raises concerns about capacity constraints.

This quarter, Primoris reported year-on-year revenue growth of 6.7%, and its $1.86 billion of revenue exceeded Wall Street’s estimates by 3.3%.

Looking ahead, sell-side analysts expect revenue to grow 5.9% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming.

Operating Margin

Primoris’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 4.9% over the last five years. This profitability was paltry for an industrials business and caused by its suboptimal cost structureand low gross margin.

Analyzing the trend in its profitability, Primoris’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Primoris generated an operating margin profit margin of 4.2%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

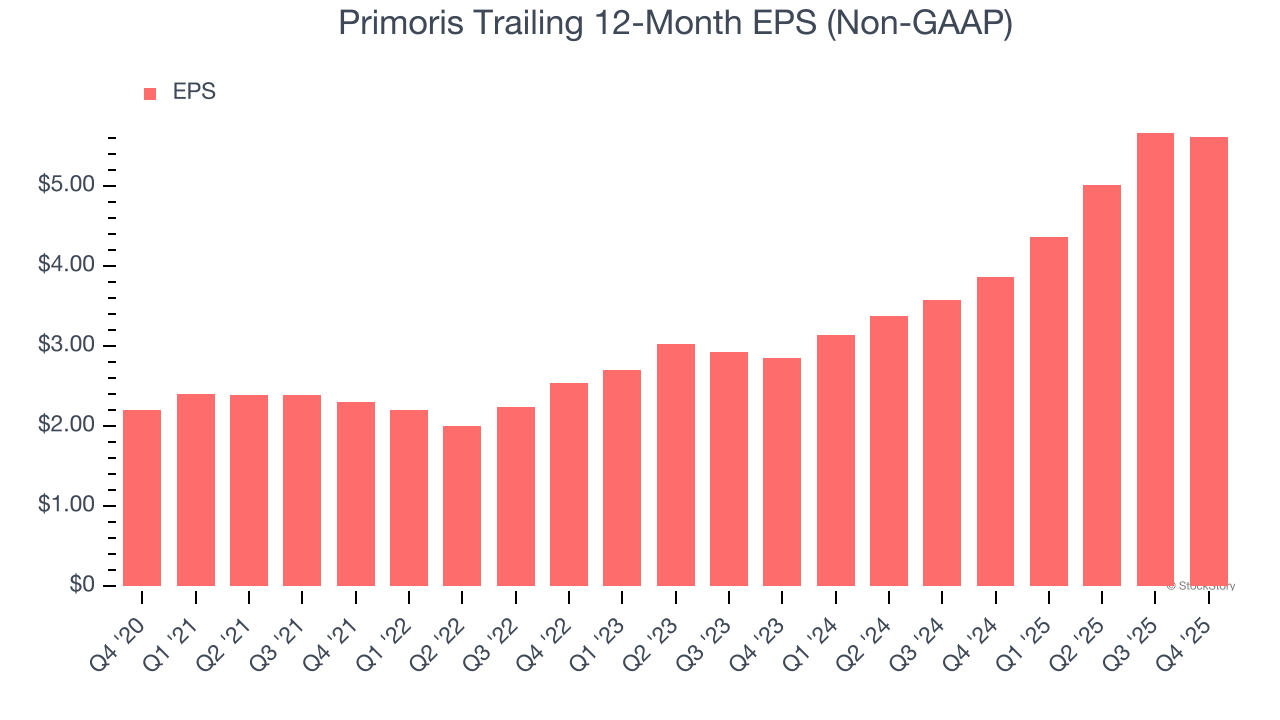

Primoris’s EPS grew at an astounding 20.6% compounded annual growth rate over the last five years, higher than its 16.8% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Primoris, its two-year annual EPS growth of 40.4% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Primoris reported adjusted EPS of $1.08, down from $1.13 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 8.9%. Over the next 12 months, Wall Street expects Primoris’s full-year EPS of $5.62 to grow 5.3%.

Key Takeaways from Primoris’s Q4 Results

We enjoyed seeing Primoris beat analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. Investors were likely hoping for more, and shares traded down 7.7% to $152.83 immediately after reporting.

Is Primoris an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Implied Volatility Surging for Kirby Stock Options

Are Bitcoin ETFs quietly accumulating or just not selling? The flow data that matters

Offshore entity takes $436M Blackrock IBIT stake

Tesla Sues California DMV, Seeks to Overturn Ruling on False Advertising of FSD