ACV Auctions's (NYSE:ACVA) Q4 CY2025 Sales Beat Estimates, Stock Soars

Online used car auction platform ACV Auctions (NASDAQ:ACVA) reported Q4 CY2025 results

ACV Auctions (ACVA) Q4 CY2025 Highlights:

- Revenue: $183.6 million vs analyst estimates of $182 million (15.1% year-on-year growth, 0.9% beat)

- EPS (GAAP): -$0.11 vs analyst estimates of -$0.12 (in line)

- Adjusted EBITDA: $7.62 million vs analyst estimates of $5.88 million (4.1% margin, 29.7% beat)

- Revenue Guidance for Q1 CY2026 is $202 million at the midpoint, below analyst estimates of $203.7 million

- EBITDA guidance for the upcoming financial year 2026 is $75 million at the midpoint, below analyst estimates of $78.13 million

- Operating Margin: -9.7%, up from -16.2% in the same quarter last year

- Free Cash Flow was -$23.37 million compared to -$1.25 million in the previous quarter

- Market Capitalization: $1.15 billion

Company Overview

Founded in 2014, ACV Auctions (NASDAQ:ACVA) is an online auction marketplace for car dealers and wholesalers to buy and sell used cars.

Revenue Growth

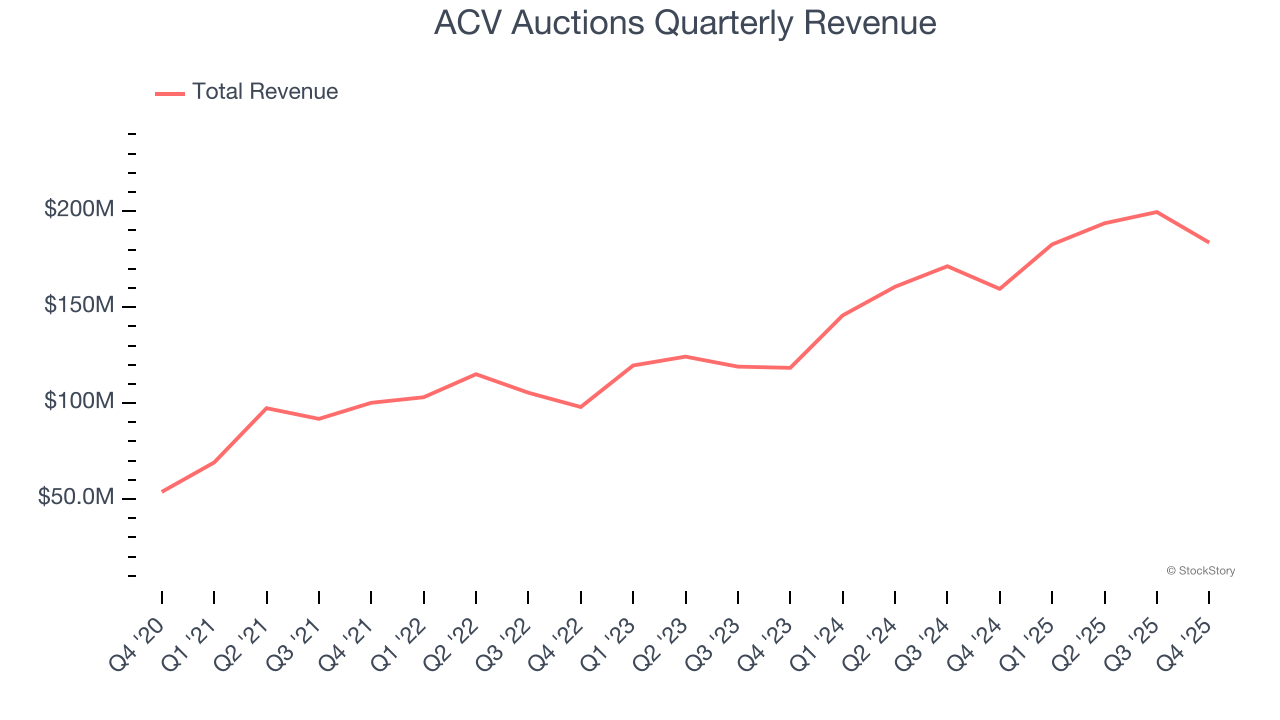

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, ACV Auctions’s 21.7% annualized revenue growth over the last three years was impressive. Its growth beat the average consumer internet company and shows its offerings resonate with customers.

This quarter, ACV Auctions reported year-on-year revenue growth of 15.1%, and its $183.6 million of revenue exceeded Wall Street’s estimates by 0.9%. Company management is currently guiding for a 10.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.4% over the next 12 months, a deceleration versus the last three years. Still, this projection is noteworthy and indicates the market is forecasting success for its products and services.

Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

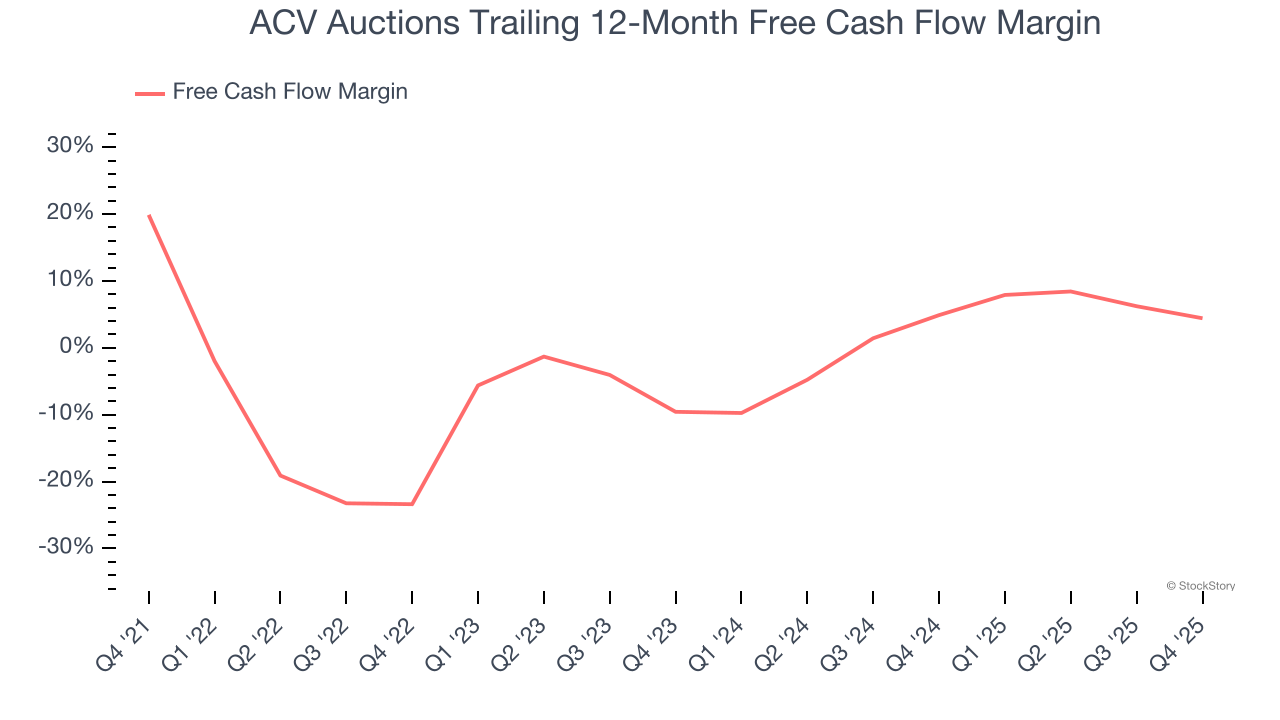

ACV Auctions has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.6%, subpar for a consumer internet business.

Taking a step back, an encouraging sign is that ACV Auctions’s margin expanded by 27.8 percentage points over the last few years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

ACV Auctions burned through $23.37 million of cash in Q4, equivalent to a negative 12.7% margin. The company’s cash burn was similar to its $11.19 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business.

Key Takeaways from ACV Auctions’s Q4 Results

We were impressed by how significantly ACV Auctions blew past analysts’ EBITDA expectations this quarter. On the other hand, its full-year EBITDA guidance missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 9% to $6.19 immediately following the results.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

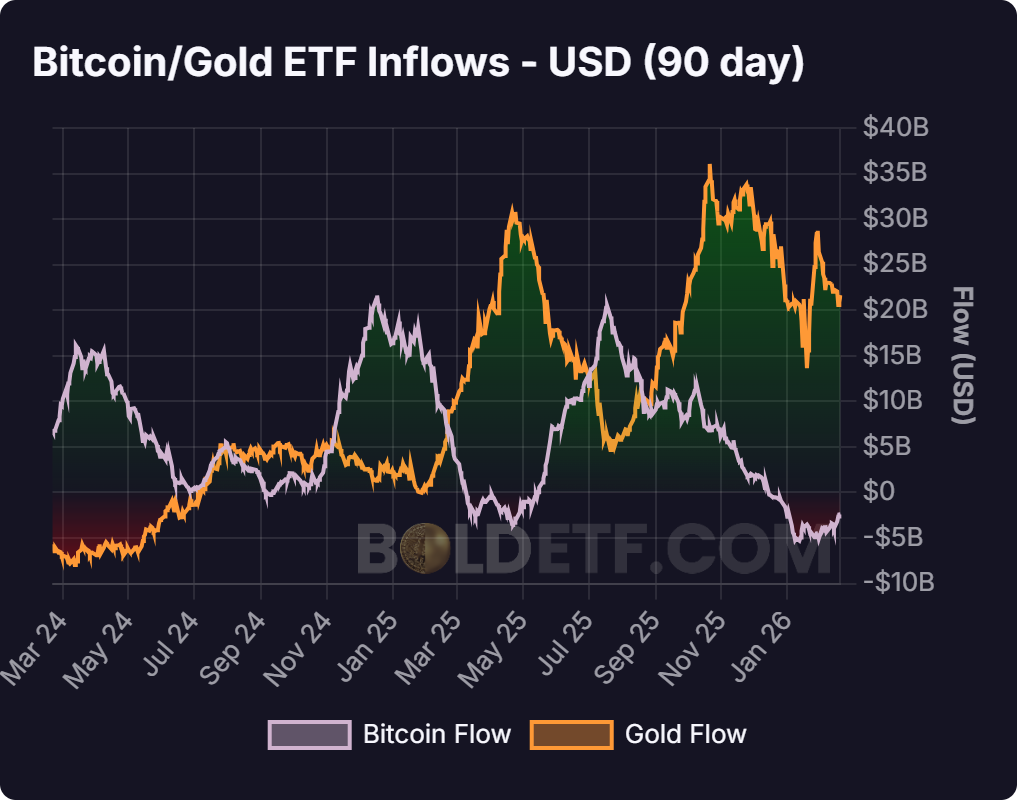

Bitcoin Faces Fourth Straight Monthly Decline as Historical Patterns Reemerge

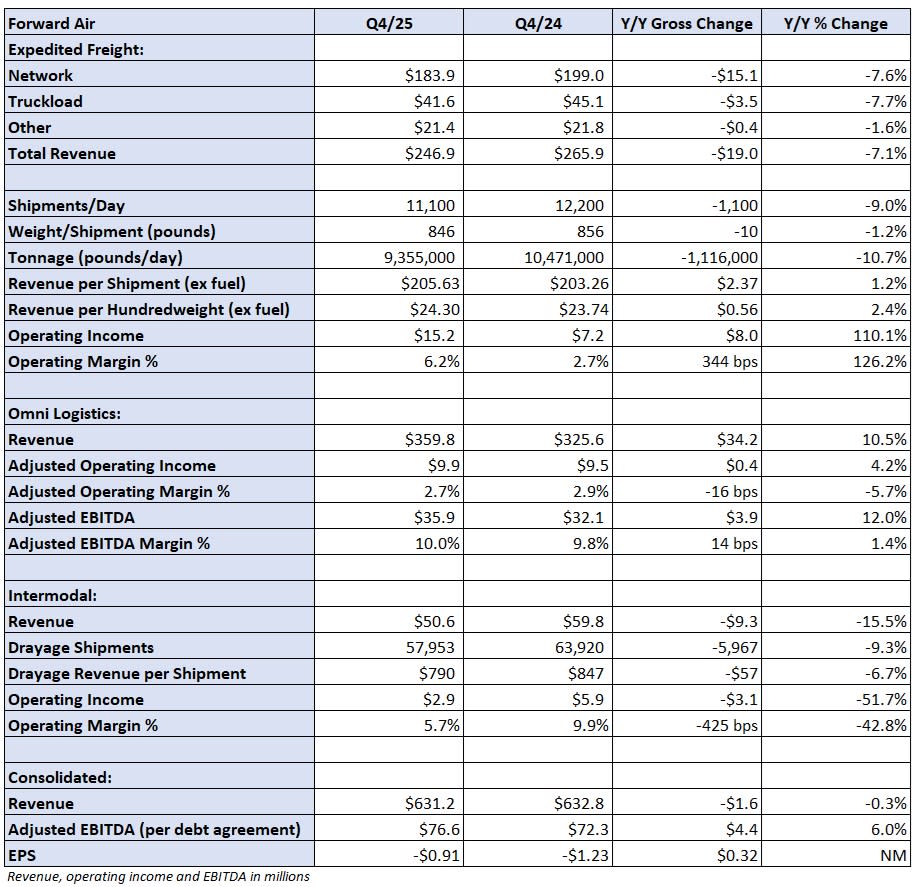

Forward Air states that its strategic review is close to completion

Implied Volatility Surging for Kirby Stock Options

Are Bitcoin ETFs quietly accumulating or just not selling? The flow data that matters