Bond traders are wagering that Federal Reserve rate reductions will extend into 2027

Market Shifts: Traders Anticipate Extended Fed Rate Cuts

US futures and options traders are increasingly betting that the Federal Reserve will continue lowering interest rates well into next year, moving away from expectations of rate hikes. Spreads tied to the Secured Overnight Financing Rate (SOFR), which closely mirror anticipated Fed actions, have become sharply inverted. This suggests that investors foresee a longer period of monetary easing by the central bank.

Top Bloomberg Headlines

Previously, many traders expected the Fed to resume raising rates in 2027 after two anticipated quarter-point cuts by the end of this year. However, concerns about how artificial intelligence might affect employment are prompting a reassessment. Federal Reserve Governor Lisa Cook recently cautioned that the central bank may struggle to offset job losses caused by AI adoption.

Since last week, SOFR spreads have flattened rapidly, coinciding with a wave of AI-related worries that triggered a surge in long-term Treasury bonds. Jack McIntyre, a portfolio manager at Brandywine Global Investment Management, noted, “The main inflationary effect of AI is the expansion of data centers and their energy demands, which is already understood.”

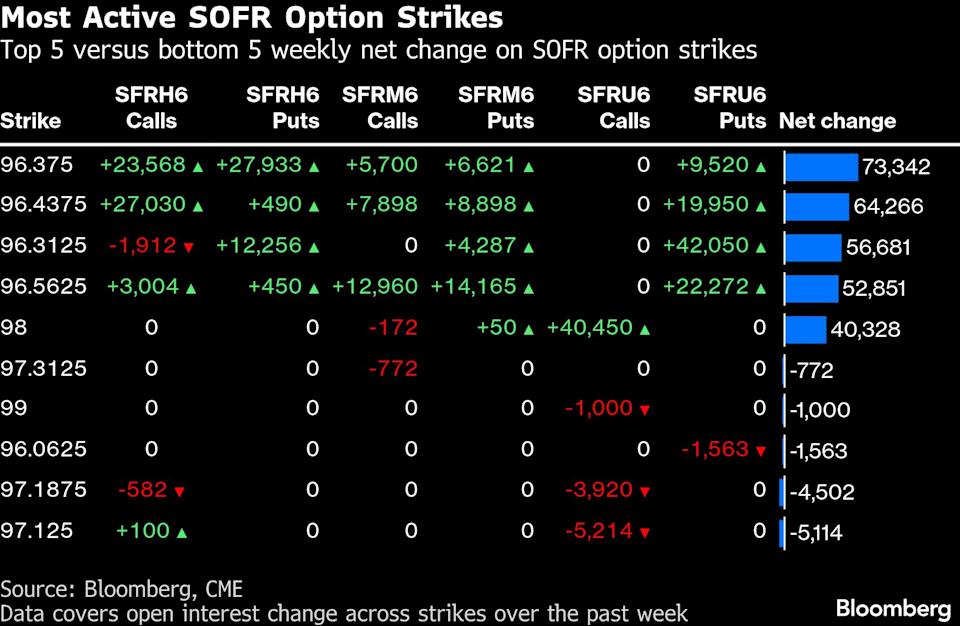

SOFR Spread Trends and Trading Activity

The December 2026 to 2027 SOFR spread turned negative on Friday, deepening to minus 8 basis points by Tuesday. This shift indicates that investors are now pricing in rate cuts for 2027 rather than hikes. Over 150,000 contracts traded in this 12-month spread during Monday’s session.

Options Market Signals

SOFR options trading is also reflecting expectations for multiple rate reductions this year. On Tuesday, positions grew for hedging against the policy rate dropping as low as 2% by year-end. Open interest in December 98.00 calls surged past 400,000 contracts this week. The swaps market currently anticipates a Fed rate near 3.1%—just over two quarter-point cuts—by the end of the year, which is 110 basis points above the options strike price.

SOFR Trade Targeting 2% Year-End Rate Surges to $40 Million

Gennadiy Goldberg, head of US rates strategy at TD Securities, commented, “There’s been a shift toward lower yields after the Fed reaches its terminal rate, with the market expecting a slower rise in yields.”

Uncertainty and Treasury Curve Movements

Goldberg added that uncertainty about AI’s impact on jobs could be influencing these shifts, but longer-term Fed expectations tend to fluctuate significantly, making them hard to interpret. Treasury curve metrics also show the market is pricing in extended rate cuts: the 2- to 5-year spread hit its flattest point since December, and the 2s5s30s butterfly saw its largest single-day move in six months, driven by strong performance in the mid-section of the curve.

In the cash market, traders are unsure how to position themselves in Treasuries. JPMorgan’s latest client survey, covering the week ending February 23, revealed the highest level of neutral positioning since late 2024.

On Wednesday, US Treasuries declined across maturities, with the 10-year yield rising two basis points to 4.05%.

Recent Rates Market Positioning

- JPMorgan Survey: During the week ending February 23, clients reduced short positions by four percentage points and trimmed longs by two percentage points. Short positions are at their lowest since December, while neutral positioning is at its highest since the end of 2024.

- SOFR Options: Over the past week, significant new risk was added to September 2026 puts, mainly through heavy buying of SFRU6 96.4375/96.3125/96.1875 put flies. March calls also saw notable activity, with SFRH6 96.375/96.4375/96.50 call flies being particularly popular.

- Strike Activity: The 96.375 strike is the most active across tenors up to September 2026, with substantial open interest in March and June calls and puts. Recent trades have focused on SFRH6 96.375/96.4375/96.50 call flies and SFRM6 96.5625/96.4375/96.375 1x3x2 put flies.

- Treasury Options Premium: The cost to hedge Treasury risk has shifted further in favor of calls over puts, indicating traders are paying more to protect against a bond rally than a selloff. This premium is highest at the long end of the curve, with 10-year and long-bond options showing the strongest call bias in months.

Most Read from Bloomberg Businessweek

With contributions from Michael MacKenzie and Miles J. Herszenhorn.

Latest price updates included.

© 2026 Bloomberg L.P.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

2 Things to Appreciate About HALO (and 1 Drawback)

Bitcoin Bear Market Isn’t Killing Interest—Newcomers Are Flooding In

3 Bullish Signals for Bitcoin That Investors Are Overlooking Amid Extreme Fear

Fomento Economico: Fourth Quarter Financial Overview