Astec (NASDAQ:ASTE) Surpasses Forecasts with Robust Q4 CY2025 Performance

Astec (ASTE) Q4 CY2025 Earnings Overview

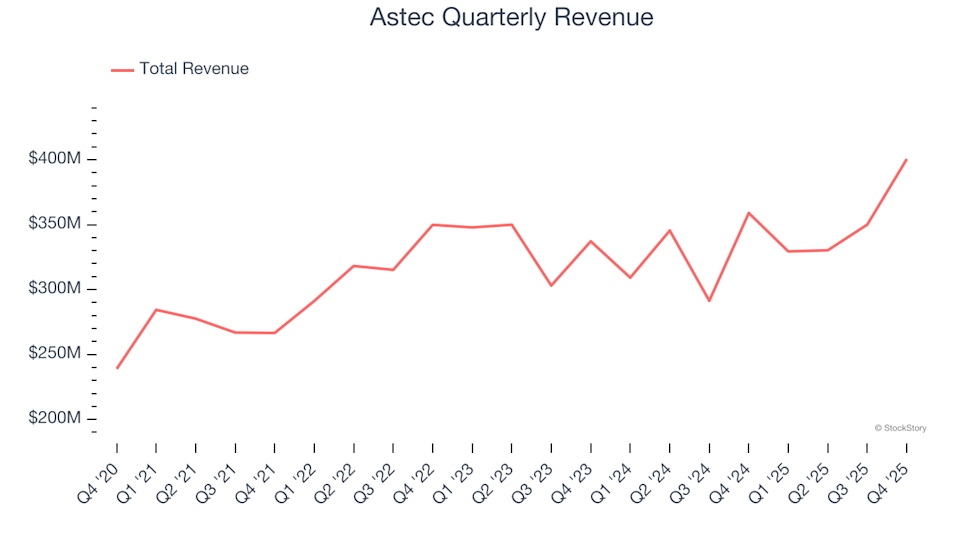

Astec, a manufacturer of construction equipment listed on NASDAQ as ASTE, reported fourth-quarter revenue for calendar year 2025 that surpassed expectations. Sales climbed 11.6% year-over-year, reaching $400.6 million. The company's adjusted earnings per share came in at $1.06, beating analyst forecasts by 27.7%.

Considering these results, is Astec a worthwhile investment right now?

Highlights from Astec's Q4 CY2025 Report

- Revenue: $400.6 million, exceeding analyst projections of $374.2 million (11.6% growth year-over-year, 7.1% above estimates)

- Adjusted EPS: $1.06, compared to analyst expectations of $0.83 (27.7% higher)

- Adjusted EBITDA: $44.7 million, beating estimates of $37.5 million (11.2% margin, 19.2% above forecast)

- Operating Margin: 5.7%, a decrease from 12.2% in the same period last year

- Free Cash Flow Margin: 1.8%, down from 8.9% year-over-year

- Backlog: $514.1 million at quarter-end, up 22.5% from the previous year

- Market Capitalization: $1.34 billion

About Astec

Astec (NASDAQ:ASTE) is known for pioneering the double-barrel hot-mix asphalt plant. The company supplies machinery and equipment used in road construction, material processing, and concrete production.

Revenue Performance

Assessing a company's sustained growth is key to understanding its quality. While short-term gains can occur, consistent expansion over several years is a sign of strength. Astec's annualized revenue growth over the past five years was 6.6%, which falls short of the industrial sector's benchmark and signals moderate performance.

At StockStory, we prioritize long-term growth, but recognize that five-year trends may overlook industry cycles or catalysts like new contracts or product launches. Astec's recent results indicate slowing demand, with two-year annualized revenue growth at 2.7%, below its five-year average. This slowdown is concerning, as it may reflect shifting customer preferences and low barriers to switching. Many construction machinery companies have also seen sales decline due to cyclical challenges. Despite slower growth, Astec outperformed some competitors.

Examining the backlog—orders yet to be fulfilled—provides further insight. Astec's backlog stood at $514.1 million in the latest quarter, but averaged a 13.1% year-over-year decline over the past two years. Since backlog growth trails revenue growth, it suggests Astec may struggle to sustain its current pace in the future.

Future Outlook

This quarter, Astec achieved 11.6% year-over-year revenue growth, with sales exceeding Wall Street's expectations by 7.1%. Analysts forecast a 3.6% revenue increase over the next year, mirroring recent trends. This modest projection indicates that new offerings are unlikely to drive significant top-line improvement soon.

Technology continues to reshape industries, fueling demand for solutions that support software development, such as cloud monitoring, audio/video integration, and content streaming.

Profitability and Operating Margin

Operating margin is a key indicator of profitability, showing how much income remains after production, marketing, and R&D expenses. Over the past five years, Astec has been profitable but its average operating margin of 5.1% is considered low for an industrial company, largely due to a substantial cost base and modest gross margins.

On a positive note, Astec's operating margin improved by 5.1 percentage points over five years, reflecting increased efficiency from sales growth.

In the most recent quarter, operating margin was 5.7%, a drop of 6.5 percentage points year-over-year. This decline, greater than the decrease in gross margin, suggests rising costs in areas like marketing, research, and administration.

Earnings Per Share Analysis

While revenue trends highlight growth, changes in earnings per share (EPS) reveal profitability. Astec's EPS grew at a compounded annual rate of 10.4% over five years, outpacing its revenue growth and indicating improved profitability per share.

Looking closer, Astec's two-year annual EPS growth rate of 11.2% aligns with its five-year trend, demonstrating consistent earnings strength. In Q4, adjusted EPS was $1.06, down from $1.19 a year earlier, but still well above analyst expectations. Wall Street anticipates Astec's full-year EPS to remain steady at $3.29 over the next twelve months.

Summary of Astec's Q4 Results

Astec exceeded analyst EPS forecasts this quarter, and its EBITDA was notably higher than expected. Overall, the results were solid, with shares rising 1% to $59.09 immediately after the announcement.

Although Astec delivered a strong quarter, a single earnings report isn't enough to justify buying the stock. Investment decisions should weigh long-term business quality and valuation alongside recent performance.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.