AI Initiatives & Extensive Partner Network: Is Adobe Stock Poised for a Comeback?

Adobe’s AI Strategy and Expanding Partnerships

Adobe is strengthening its position in a challenging market by broadening its network of partners and investing heavily in artificial intelligence. While many traditional SaaS companies are being impacted by the rise of AI, Adobe’s innovative AI-driven product lineup is designed to help the company stay competitive against major players like Microsoft and Alphabet. Despite these efforts, Adobe’s stock has declined by 27.1% so far this year.

The company’s extensive partnership ecosystem includes industry leaders such as Amazon Web Services (AWS), Microsoft Azure, Copilot, Google Gemini, HUMAIN, and OpenAI. Adobe’s Firefly, Express, and Creative Cloud platforms now incorporate AI models from partners like Google, OpenAI, Black Forest Labs, Luma, Runway, Topaz Labs, and Eleven Labs. Recently, Adobe expanded its collaboration with WPP to deliver integrated, AI-powered solutions for global brands, streamlining the planning, creation, and deployment of creative and media assets at an accelerated pace.

Growth Driven by AI Integration

Adobe’s future outlook is supported by the increasing adoption of its cloud-based services, including Acrobat and Express, which now feature advanced AI tools such as Firefly and Acrobat AI Assistant. These enhancements are enabling users to generate content and manage documents more efficiently, which is boosting subscription renewals and encouraging upgrades to premium plans. The company is also introducing new AI chat features for PDFs, allowing users to interact with documents using natural language. By combining Acrobat and Express, Adobe is making it easier and faster to create presentations and podcasts from documents using AI. These capabilities are available in Acrobat Studio, which brings together advanced PDF tools, AI Assistant, and PDF Spaces in a single productivity-focused platform.

More users are turning to Acrobat AI Assistant for faster content consumption and using Express to design richer PDFs, personalized presentations, and animated graphics. The demand for creative features within Acrobat is rising, and Adobe is seeing strong adoption of Express premium plans among individuals, small businesses, and enterprises. This momentum is expected to fuel revenue growth in fiscal 2026, with consensus estimates projecting sales of $26.04 billion—a 9.5% increase over fiscal 2025.

Competitive Landscape in AI

Although Adobe is making significant strides in AI, its presence in this space is still much smaller compared to Microsoft and Alphabet. Microsoft’s Intelligent Cloud division is experiencing robust growth, driven by Azure AI services and the success of its Copilot product. By leveraging existing customer relationships, Microsoft is able to reduce acquisition costs and increase revenue per user. The company’s remaining performance obligations total $625 billion, and there are 15 million paid seats for Microsoft 365 Copilot, highlighting strong enterprise demand for AI solutions.

Alphabet is also prioritizing AI across its products, including Search and Google Cloud. Features like AI Overviews and AI Mode are increasing both general and commercial search queries, creating new monetization opportunities. The introduction of personal intelligence in AI Mode and the Gemini app further strengthens Alphabet’s growth prospects.

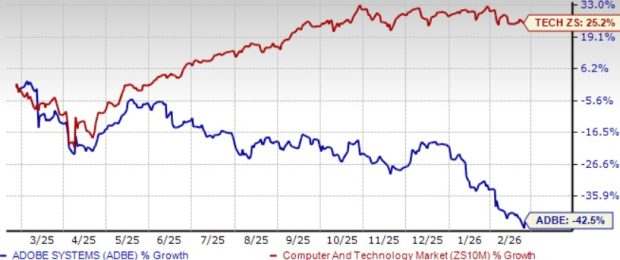

Adobe’s Stock Performance and Valuation

Over the past year, Adobe’s share price has dropped by 42.5%, significantly underperforming the broader Computer and Technology sector, which saw a return of 25.2%.

Adobe’s Stock Lags Behind the Sector

Source: Zacks Investment Research

Currently, Adobe’s stock appears undervalued, earning a Value Score of B. When looking at the forward 12-month price-to-sales ratio, Adobe trades at 3.94, which is lower than the sector average of 6.38.

Adobe Shares Offer Value

Source: Zacks Investment Research

The consensus estimate for Adobe’s fiscal 2026 earnings stands at $23.47 per share, unchanged over the past month, and represents a projected 12.1% increase from fiscal 2025.

Adobe Inc. Price and Consensus

Currently, Adobe holds a Zacks Rank #3 (Hold).

Top Semiconductor Stock Highlighted by Zacks

A lesser-known company in the semiconductor industry is emerging as a key player, offering products that giants like NVIDIA do not. Positioned to capitalize on the next wave of market growth, this company is just beginning to gain attention.

With robust earnings and a growing customer base, it is well-placed to meet the surging demand for Artificial Intelligence, Machine Learning, and the Internet of Things. Global semiconductor manufacturing is expected to soar from $452 billion in 2021 to $971 billion by 2028.

Get More Insights from Zacks

Looking for the latest stock recommendations? Download the “7 Best Stocks for the Next 30 Days” from Zacks Investment Research.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Can XPL bulls absorb the $10.79 mln token unlock? Assessing…

FirstEnergy’s $36 Billion Gamble: Is This a Quality Strategy or Overpaying for Growth?

FirstEnergy's $36B Bet: A Quality Factor Play or Growth-at-a-Price?

Exclusive-Nintendo plans around $1.9 billion share sale by Kyoto bank and others, sources say