Evaluating SkyWest: Competitive Advantage, Safety Margin, and Risk Assessment

SkyWest: A Model of Efficient Regional Airline Operations

SkyWest exemplifies a streamlined, asset-light approach to regional aviation, thriving through robust, long-term partnerships. The company’s foundation is its capacity purchase agreements with major airlines, such as United, which handle ticket sales and scheduling. In this arrangement, SkyWest receives payment based on completed flights, ensuring steady income and insulating the company from the unpredictable swings in passenger demand and fare competition that challenge traditional carriers. Rather than relying on brand recognition, SkyWest’s competitive edge comes from being an essential, cost-effective partner within larger airline networks.

Operational Excellence Reflected in Financial Performance

SkyWest’s financial achievements highlight its operational strengths. In the second quarter of 2025, the company posted a net margin of 11.62%, outpacing industry peers and showcasing its ability to manage costs effectively. The company’s growth trajectory is equally impressive: for the full year 2025, SkyWest reported net income of $428.3 million, marking a 32.6% increase year-over-year. This surge was fueled by increased block hour production and disciplined expense management, underscoring SkyWest’s capacity to generate and grow shareholder value.

Shareholder Returns: A Testament to Value Creation

Perhaps the most striking evidence of SkyWest’s successful model is its three-year total shareholder return of 440.83%. This remarkable performance far exceeds broader market averages and is a direct result of the company’s consistent profitability and expanding earnings. For value-focused investors, the combination of high margins, accelerating profits, and outstanding long-term returns signals a business with a lasting competitive advantage. The partnership with United is not merely a contract—it is the cornerstone of a resilient, capital-efficient enterprise that has repeatedly demonstrated its ability to build wealth for shareholders.

Financial Strength and Capital Deployment

SkyWest’s 2025 results reveal a company focused on per-share value and prudent capital allocation. Diluted earnings per share climbed to $10.35, up from $7.77 the previous year, reflecting the company’s ability to translate revenue growth into tangible returns for investors.

Management is actively returning profits to shareholders. The company’s updated 2026 guidance projects earnings in the mid-$11 per share range, coinciding with progress on a multi-year share repurchase initiative. This approach—combining forward-looking guidance with buybacks—demonstrates a commitment to maximizing shareholder value, especially when the stock trades below its estimated intrinsic worth.

SkyWest’s balance sheet supports this disciplined strategy. As of June 2025, the debt-to-equity ratio stood at 0.78, a conservative level for a company with minimal capital requirements. This ratio has steadily declined, reflecting reduced financial risk and leaving room to fund growth projects, such as the upcoming Embraer E175 deliveries in 2026, without overextending the company’s finances.

In summary, SkyWest’s financial health—characterized by rising earnings, manageable debt, and ongoing capital returns—provides a solid foundation for sustained value creation.

Valuation: Assessing the Margin of Safety

From a value investing perspective, the key question is whether SkyWest’s intrinsic value significantly exceeds its current market price. As of January 2026, the company trades at a trailing P/E ratio of 9.30, well below both its historical average and the broader market, offering a clear margin of safety. This discount suggests that investors may be underestimating the durability of SkyWest’s competitive advantages and profitability.

Discounted cash flow analysis further supports the investment case. Using a five-year growth projection, SkyWest’s intrinsic value is estimated at $149.97 per share. With shares trading near $116 in August 2025, this points to a potential upside of 29.1%. The range of DCF outcomes—from $91.85 to $292.66—reflects the sensitivity of valuation to future growth and discount rate assumptions. For a company whose fortunes are closely tied to airline partnerships and fleet upgrades, this uncertainty is real. Thus, the margin of safety is best viewed as a protective range rather than a fixed number, with the current price comfortably below the midpoint.

Ultimately, SkyWest offers a compelling value proposition: high-quality earnings, a significant moat, and a market valuation that leaves room for upside. While the DCF model highlights potential gains, it also reminds investors of the importance of caution in forecasting. For those seeking disciplined, long-term opportunities, SkyWest’s combination of business strength and valuation buffer is attractive.

Key Drivers, Risks, and Monitoring Points

The investment thesis for SkyWest depends on effective execution. The main catalyst is the successful rollout of its fleet expansion plan. The company has firm orders for 69 Embraer E175 jets, with 20 scheduled for delivery in 2026 to support United Airlines. This modernization effort is vital, as it underpins SkyWest’s capacity agreements and enables the higher block hour production that fueled its recent revenue growth. Timely delivery and seamless integration of these new, fuel-efficient aircraft are crucial near-term milestones that will reinforce the company’s growth outlook and valuation.

However, SkyWest’s heavy reliance on United Airlines introduces concentration risk. While the company maintains code-share agreements with several major carriers, most of its capacity and revenue are linked to United. Any disruption in this relationship—whether from strategic shifts, contractual disputes, or broader market downturns—could have immediate consequences for SkyWest’s financial performance. This dependency is the primary counterbalance to its operational strengths.

Other industry-wide risks include a persistent pilot shortage and unpredictable fuel costs. The shortage of qualified pilots limits the ability of regional airlines to expand capacity, while volatile fuel prices can quickly erode profit margins. For SkyWest, which often serves as a training ground for new pilots, these challenges could restrict the full utilization of its growing fleet. Spikes in oil prices, driven by global events, force airlines to choose between raising fares or absorbing higher costs, directly impacting profitability.

In conclusion, investing in SkyWest requires ongoing vigilance. The success of the fleet expansion is the immediate catalyst, but its realization depends on flawless execution. Concentration risk and industry headwinds are persistent challenges that management must continually address. For investors, the current valuation offers a margin of safety, but this protection is only as strong as the company’s ability to navigate these evolving risks. Key areas to monitor include the delivery schedule for new E175s, any developments in the United partnership, and trends in pilot availability and fuel expenses.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Negative Funding Rates Drive Short Positions in Bitcoin Futures

Buried Libra, Meta returns with a more cautious stablecoin strategy

ETHZilla stock climbs on Forum rebrand as firm pushes further into tokenized assets

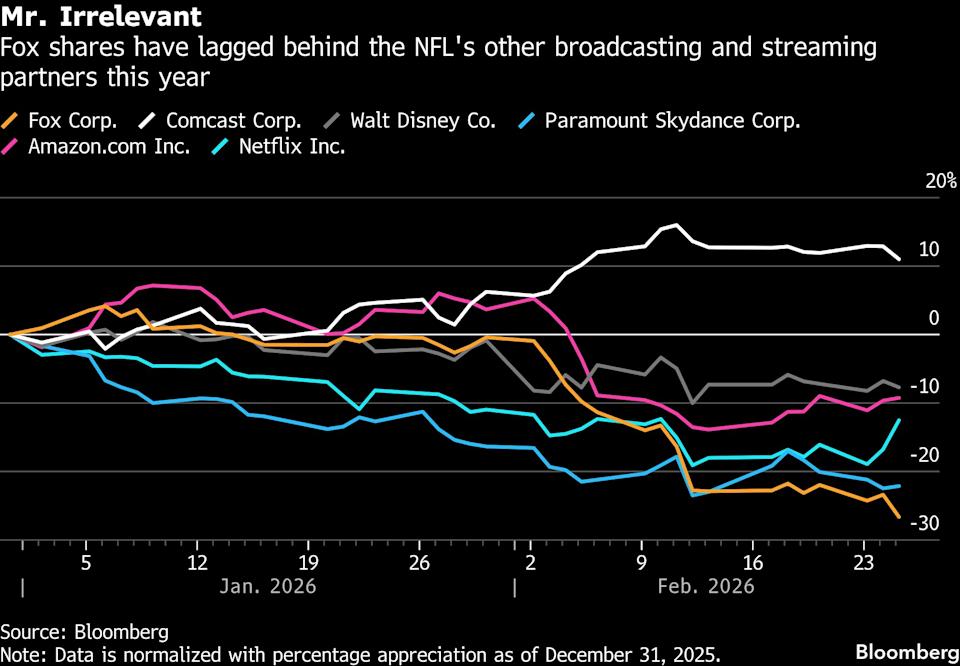

NFL contract concerns lead BofA to slash Fox shares with two-level downgrade