Fidelis Insurance (NYSE:FIHL) Announces Q4 CY2025 Revenue Falling Short of Analyst Projections

Fidelis Insurance (FIHL) Q4 2025 Earnings Overview

Fidelis Insurance (NYSE: FIHL), a provider specializing in niche insurance products, reported fourth-quarter 2025 revenue of $600.9 million—a 10.8% decrease compared to the same period last year and below analyst forecasts. However, the company posted a non-GAAP earnings per share of $1.09, slightly exceeding consensus estimates by 1.3%.

Q4 2025 Performance Highlights

- Net Premiums Earned: $552.9 million, missing expectations of $621.3 million (down 12.9% year-over-year, 11% below estimates)

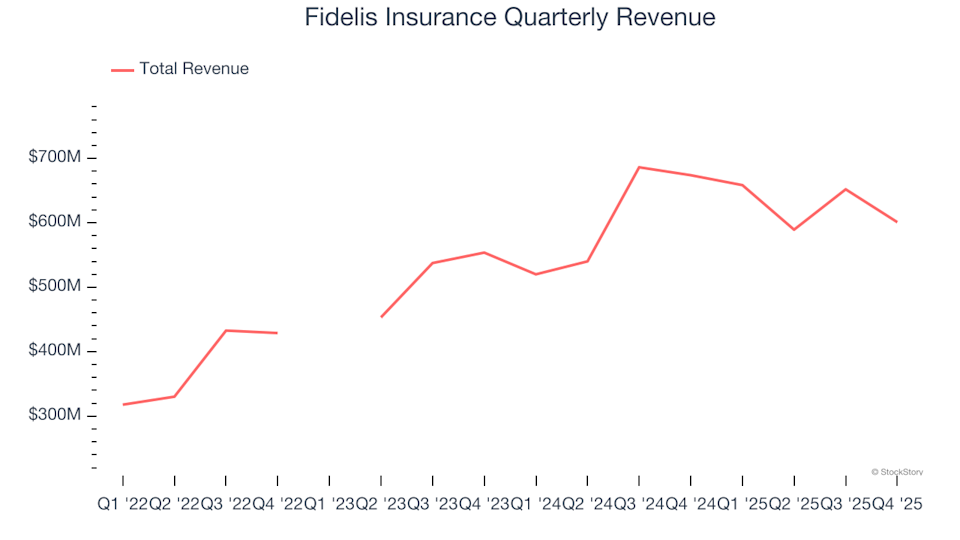

- Total Revenue: $600.9 million, compared to the anticipated $706.8 million (a 10.8% decrease year-over-year, 15% below projections)

- Combined Ratio: 80.6%, outperforming the expected 84.5% by 390 basis points

- Adjusted EPS: $1.09, slightly above the $1.08 forecast (1.3% beat)

- Book Value per Share: $24.61, in line with the $24.51 estimate (12.3% annual growth)

- Market Cap: $2.07 billion

Dan Burrows, CEO of Fidelis Insurance Group, stated: “Our strong fourth quarter, marked by an 80.6% combined ratio and an annualized Operating ROAE of 18.3%, highlights the resilience of our business model and our ability to achieve our strategic objectives as we manage capital allocation.”

About Fidelis Insurance

Established in Bermuda in 2014, Fidelis Insurance (NYSE: FIHL) operates globally in the specialty insurance and reinsurance sector. The company is structured to respond quickly to changing market dynamics, focusing on value creation through strategic capital deployment, expert risk assessment, and long-term underwriting partnerships.

Revenue Trends

Insurance companies generate income through three main channels: underwriting (premiums earned), investment returns on collected premiums (the “float”), and fees from services such as policy administration or annuities. Over the past three years, Fidelis Insurance achieved a remarkable 24.4% compound annual revenue growth rate, outpacing industry averages and indicating strong market demand for its offerings.

Note: Certain quarters are excluded due to extraordinary investment gains or losses that do not reflect the company’s ongoing business fundamentals.

While we prioritize long-term growth, it’s important to consider recent shifts in interest rates, market performance, and industry trends. Over the past two years, Fidelis Insurance’s annualized revenue growth slowed to 9.2%, below its three-year average, but still suggests steady demand for its services.

Recent Revenue and Premiums Performance

This quarter, Fidelis Insurance fell short of Wall Street’s revenue expectations, reporting a 10.8% year-over-year decline to $600.9 million. Net premiums earned accounted for 78.6% of total revenue over the past four years, underscoring the central role of core insurance operations in the company’s business model.

Note: Certain quarters are excluded due to extraordinary investment gains or losses that do not reflect the company’s ongoing business fundamentals.

Investors and analysts typically place greater emphasis on growth in net premiums earned, as it is a key indicator of underwriting performance and market reach.

Book Value Per Share (BVPS)

Insurance companies are fundamentally balance sheet-driven, collecting premiums upfront and paying claims over time. The “float”—premiums held before claims are paid—is invested, forming an asset base offset by liabilities. Book value per share (BVPS) measures the value of these assets (including investments, cash, and reinsurance recoverables) minus liabilities (such as claim reserves and debt), representing the value available to shareholders.

BVPS is a crucial metric for assessing the long-term quality of an insurer’s business, as it is less susceptible to short-term accounting adjustments than earnings per share. Over the past two years, Fidelis Insurance’s BVPS increased at a modest 8.8% annual rate.

Note: Certain quarters are excluded due to extraordinary investment gains or losses that do not reflect the company’s ongoing business fundamentals.

Looking ahead, analysts expect Fidelis Insurance’s BVPS to rise by 30% over the next year, reaching $24.51—a notably strong growth rate.

Final Thoughts on Q4 Results

Overall, the latest quarterly results were underwhelming, with both revenue and net premiums earned missing expectations. The company’s share price remained steady at $20.10 following the announcement.

Is Fidelis Insurance a buy? We believe that one quarter’s results are just a piece of the bigger picture. Evaluating long-term business quality alongside valuation is essential for making informed investment decisions.

Explore More

Technology is transforming every industry, and the demand for tools that support software developers continues to grow.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Pan American Silver Slumps 1.62% Amid 34.42% Volume Surge to $450M Ranks 298th as Institutional Holdings Soar

Atlassian's Stock Gains 2.82% Despite 36% Volume Drop, Ranking 292nd in Market Activity

Ingersoll Rand Stock Plummet Despite 90.96% Volume Surge to $450M Ranks 301st in Market Activity

UPS Buyout Spur $460M Surge, 296th Trading Rank as Shares Slide 1.32% Amid Restructuring Uncertainty