NVIDIA FY2026 Q4 Earnings Highlights: Revenue Surges 73% Beating Expectations, Data Center Soars 75%, Q1 Guidance Sets Record High at $78 Billion

Key Takeaways

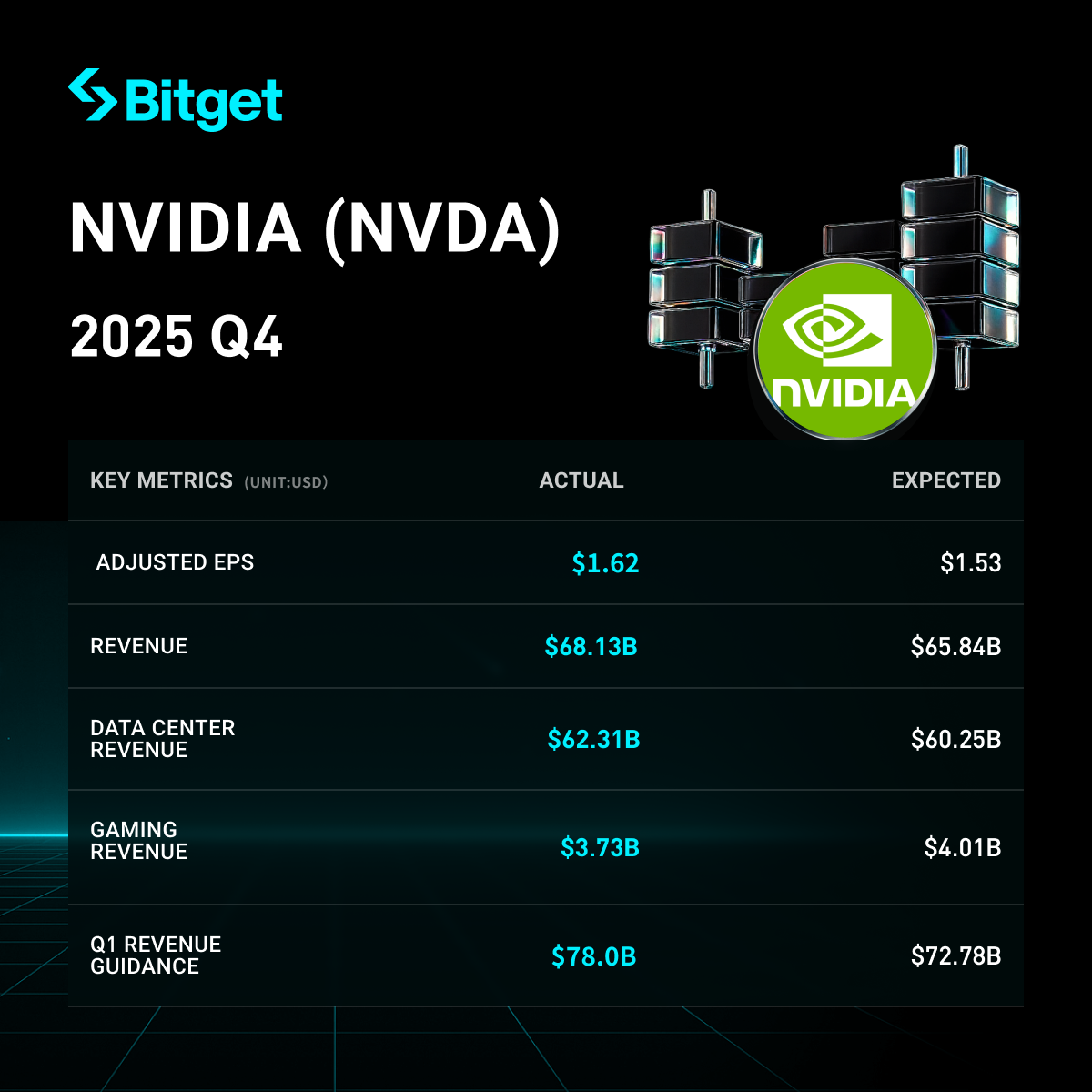

NVIDIA(NVDA.US) delivered a strong beat in its FY2026 fourth-quarter earnings. Revenue reached $68.127 billion, up 73% year-over-year and exceeding both the company’s own midpoint guidance of $65 billion and analyst consensus of $65.84 billion (a beat of roughly 3%). Non-GAAP EPS rose more than 80% year-over-year, surpassing expectations by approximately 5.9%. The Data Center segment, which accounted for over 90% of total revenue, was the primary driver. Full-year revenue hit a record $215.938 billion, up 65% year-over-year. For Q1 FY2027, NVIDIA issued an exceptionally strong outlook with revenue guidance centered at $78 billion (implying ~77% year-over-year growth), well above the Street consensus of $72.78 billion. Shares rose more than 1% intraday on March 25 and briefly surged nearly 4% in after-hours trading before pulling back during the earnings call, reflecting lingering market caution around AI demand sustainability.

Detailed Breakdown

- Overall Revenue and Profit Performance

- Q4 revenue: $68.127 billion, +73% YoY, beating the company’s midpoint guidance of $65 billion and analyst expectations of $65.84 billion (beat of ~3%).

- Full-year revenue: $215.938 billion, +65% YoY, setting a new annual record.

- Q4 non-GAAP gross margin: 75.2%, +1.7 percentage points YoY and +1.6 percentage points QoQ, exceeding the 75.0% consensus and marking the highest level since Q2 2025.

- Full-year non-GAAP gross margin: 71.3%, down 4.2 percentage points YoY due to platform transitions and supply ramp-up.

- Q4 non-GAAP EPS: +80%+ YoY, beating analyst estimates by ~5.9%.

- Data Center Segment Performance

- Q4 revenue: $62.314 billion, +75% YoY (accelerating from 66% in the prior quarter) and beating analyst expectations of ~$60.36 billion; accounted for over 90% of total revenue.

- Data Center Compute: $51.334 billion, +58% YoY (slightly up from 56% in Q3).

- Data Center Networking: $10.98 billion, +263% YoY (sharply higher than 162% in Q3), driven by NVLink compute fabric for GB200/GB300 systems and growth in Ethernet and InfiniBand platforms.

- Hyperscalers represented slightly over 50% of Data Center revenue, but the majority of sequential growth came from other enterprise and data center customers, signaling broadening demand.

- Other Business Segments Performance

- Gaming: Q4 revenue $3.727 billion, +47% YoY (accelerating from 30% in the prior quarter) but down 13% QoQ and below the $4.01 billion consensus. Strong Blackwell demand was offset by post-holiday channel inventory normalization; supply constraints are expected to remain a headwind into Q1 and beyond.

- Professional Visualization: Q4 revenue $1.321 billion, +159% YoY (accelerating from 56% in the prior quarter), well above the $0.771 billion consensus and up 74% QoQ, fueled by Blackwell ramp.

- Future Plans and Outlook

- CEO Jensen Huang raised the company’s chip revenue target, stating it will exceed the previous $500 billion goal (originally set for 2025–2026 orders including the Rubin platform). He emphasized that “supply will meet demand through next year,” highlighted exploding demand for AI compute and agentic applications, and noted that customers are racing to build out AI infrastructure.

- Next-Quarter Guidance (FY2027 Q1)

- Revenue guidance: Midpoint $78 billion (range $76.44–$79.56 billion, ±2%), implying ~76.9% YoY growth (accelerating from Q4) and beating both Street consensus midpoint of $72.78 billion and buy-side optimistic targets of $74–75 billion by ~4%. The guidance excludes China Data Center compute revenue.

- Non-GAAP gross margin guidance: 75% (±50 basis points), in line with buy-side optimism and expected to reach a new high since Q2 2025 (versus sell-side consensus of 74.7%).

- Note: Starting in Q1, non-GAAP metrics will include stock-based compensation (SBC) expense, adding ~$1.9 billion to operating expenses.

- Market Context and Investor Concerns

- Market backdrop: The AI boom continues to demonstrate resilience despite new Anthropic product launches and Citrini’s bearish “doomsday” report.

- Key tensions: Sustained high operating expense growth and the upcoming inclusion of SBC in non-GAAP results, which could alter perceptions of profit expansion.

- Investor and analyst reaction: Positives include the Data Center and total revenue beats, gross margin expansion from Blackwell ramp, and robust Q1 guidance that reinforces the AI compute demand narrative. However, the post-call pullback in shares indicates persistent concerns about potential AI overheating.

Bitget U.S. stock festival is live! Enjoy fees as low as 0

Disclaimer: This content is for reference only and does not constitute investment advice.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Writeonix and TomaTok Partner to Revolutionize AI-Powered DeFi Messaging on Solana

US Dollar Index falls to near 97.50 as White House policy doubts linger

Bitcoin Diverges From Gold In Rare Shift