Not Just Outstanding Performance! Goldman Sachs Identifies Three Major Catalysts for NVIDIA, Says the Path to Outperformance in the Coming Months Is Clear

Nvidia's recently released quarterly results and future guidance have completely shattered Wall Street expectations. In its latest research report, Goldman Sachs clearly points out that the path for this chip giant to outperform the market in the coming months has become exceptionally clear.

Driven by sustained robust capital expenditures from hyperscale cloud service providers, Nvidia's first-quarter revenue guidance far exceeded market consensus. According to Chasing Wind Trading Desk, Goldman Sachs analyst James Schneider and his team reiterated their “Buy” rating and maintained a $250 price target, which suggests nearly 28% upside from current levels. This move is expected to further boost market confidence in the entire AI infrastructure sector.

The market's optimism is not just about historical performance being delivered. In its report, Goldman Sachs proactively identified three core catalysts driving Nvidia's sustained strength:Upward revisions in capital expenditure expectations from hyperscale enterprises, increased visibility into spending by AI startups after their financing rounds, and the release of next-generation AI models based on new architectures that will once again confirm Nvidia's technological moat.

In addition, Nvidia’s recent deep strategic cooperation and billion-dollar investment layouts with leading tech giants such as Meta, OpenAI, and Anthropic not only fundamentally secure its future order base, but also deliver widespread positive spillover effects for the global tech supply chain, including sectors like storage and semiconductor equipment.

Performance and Guidance Both Crush Market Expectations

Nvidia achieved Q4 revenue of $68.1 billion, not only exceeding Goldman Sachs’ forecast of $67.3 billion but also significantly beating Wall Street’s consensus of $66.2 billion. The core data center business remains the absolute growth engine, with quarterly revenue reaching $62.3 billion. In terms of profitability, a gross margin of 75.2% and an operating margin of 67.7% both showed solid performance. Adjusted earnings per share came in at $1.76, comprehensively surpassing market expectations.

Even more eye-catching for the market is Nvidia's extremely strong future guidance. The company expects first-quarter revenue to reach a median of $78 billion, far exceeding Wall Street’s expectation of $72.1 billion. Although the company has begun including approximately $1.9 billion in stock-based compensation due to changes in accounting standards in its non-GAAP guidance, the comparable per-share earnings guidance, excluding this impact, is $1.79—still a clear outperformance compared to the market forecast of $1.67.

Three Core Catalysts Establish Outperformance Path

Goldman Sachs clearly states in its report that, unlike in some previous quarters, there are currently three factors that make Nvidia’s path to outperforming the market over the next few months even clearer.

First, forecasts for hyperscale cloud providers’ capital expenditures in 2026 still have upside potential, and early signs of capital expenditure growth in 2027 have already begun to emerge, suggesting that demand support from Nvidia’s core downstream customer base will continue to extend further out.

Second, for non-traditional customers represented by OpenAI and Anthropic, the visibility of their procurement plans through 2027 will be significantly enhanced as their respective financing rounds are completed. Nvidia disclosed that it is still actively negotiating investments and collaborations with OpenAI and expects to sign an agreement soon; meanwhile, it has completed a $10 billion investment in Anthropic, with the agreement including Anthropic training its large language models on the Blackwell and Rubin architectures.

Third, as next-generation AI models trained on the Blackwell architecture are launched to the market, Nvidia will once again demonstrate its technological leadership over competing AI chip makers in the coming months, providing the market with more tangible evidence of differentiated competition.

Alliances with Tech Giants and Resilient Gross Margins

In terms of business expansion, Nvidia is fortifying its ecosystem with intensive investments and collaborations.The report notes that Nvidia is still actively negotiating with OpenAI regarding investment and cooperation, and is expected to finalize an agreement soon. Meanwhile, the company has completed a massive $10 billion investment in Anthropic, which has agreed to train its large language models on the Blackwell and Rubin architectures. Additionally, Nvidia announced an extensive partnership with Meta, providing it with a variety of data center products. The two sides will also collaborate to deploy the Vera CPU in 2027 and introduce the Vera Rubin NVL72 into large-scale applications such as WhatsApp.

Addressing market concerns over the impact of rising high-bandwidth memory prices on profit margins, Nvidia offered reassurance. The company expects to maintain gross margins at around the mid-75% level throughout the 2026 calendar year. Goldman Sachs believes this margin resilience is mainly due to the company’s substantial advance memory-related purchase commitments made in 2025.

Extensive Supply Chain Spillover Effects and Potential Risks

Nvidia’s strong data center guidance is not only positive for itself but also sends a clear bullish signal for the entire semiconductor sector. Goldman Sachs emphasizes that this reflects the current extremely robust AI spending environment, which is most favorable for digital semiconductor names like Broadcom and AMD, and to some extent also benefits Marvell and ARM.

However, Goldman Sachs also highlights four major downside risks at the end of its report for investing in this stock: unexpected slowdown in AI infrastructure spending, market share losses due to intensifying competition, profit margin erosion due to price wars, and ongoing supply chain constraints already evident in the gaming business and expected to persist in the first quarter.

Source: Wallstreet Insights

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

5 Important Facts to Be Aware of Before the Stock Market Starts

Bitcoin’s 4-Year Cycle Still Intact as On-Chain Signals Realign

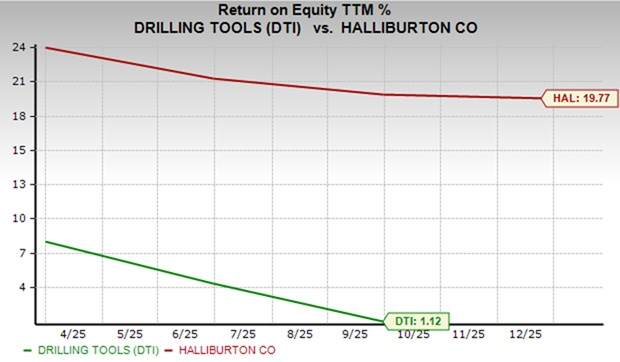

DTI or HAL: Which Oilfield Services Stock Provides Greater Value?

NVIDIA’s China AI Market Projections and Rubin Ramp Timeline Clash in Earnings Call