3 Reasons Why BKU Poses Risks and One Alternative Stock Worth Considering

BankUnited’s Recent Performance

Over the past half year, BankUnited has delivered a 24.8% return, outperforming the S&P 500 by 18.2%. Its share price has reached $48.60, thanks in part to strong quarterly earnings. This impressive run may leave investors considering their next move.

Should you add BankUnited to your portfolio now, or is caution warranted?

Reasons BankUnited May Not Be the Best Choice

While we’re pleased to see investors benefit, our outlook for BankUnited remains reserved. Here are three factors that suggest there are more attractive options than BKU, including a stock we prefer.

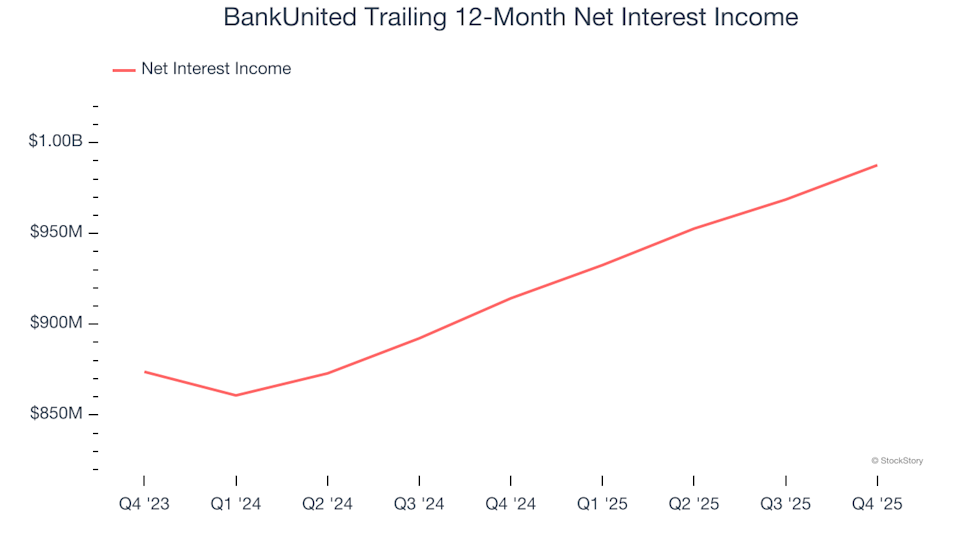

1. Net Interest Income Indicates Weak Demand

Net interest income is a key metric for banks, valued more highly than one-off fees due to its reliability. BankUnited’s net interest income has increased at an annual rate of 5.6% over the past five years, lagging behind industry peers. This growth was mainly driven by a higher net interest margin, even as the bank’s loan portfolio contracted.

BankUnited Trailing 12-Month Net Interest Income

2. Efficiency Ratio Set to Decline

Revenue growth is important, but profitability is crucial. The efficiency ratio, which measures non-interest expenses as a percentage of total revenue, is a key indicator for banks. Investors pay attention to changes in this ratio, as expense structures differ across banks. Lower efficiency ratios mean greater efficiency and profitability.

Analysts expect BankUnited’s efficiency ratio to rise to 57.8% over the next year, up from 42.5% previously, signaling reduced profitability.

BankUnited Trailing 12-Month Efficiency Ratio

3. Minimal EPS Growth

Tracking earnings per share (EPS) over time reveals whether a company’s growth is translating into profits. BankUnited’s EPS has grown just 4.9% annually over the past five years, mirroring its revenue trends. This suggests the bank has maintained profitability per share, but growth has been modest.

BankUnited Trailing 12-Month EPS (Non-GAAP)

Our Verdict

BankUnited is a decent business, but it doesn’t make our shortlist. Despite its recent market outperformance and a fair valuation at 1.1× forward price-to-book ($48.60 per share), the upside appears limited compared to the risks. We believe there are stronger investment opportunities available. Consider exploring the leading endpoint security platform as a better alternative.

Alternative Stocks Worth Considering

This year’s market rally has been driven by just four stocks, which account for half of the S&P 500’s total gains. Such concentration can make investors uneasy. While many chase popular names, savvy investors seek quality in overlooked areas, often at much lower prices. Discover our curated selection in the Top 6 Stocks for this week, featuring high-quality companies that have delivered a 244% return over the past five years (as of June 30, 2025).

Our list includes well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, and lesser-known firms such as Tecnoglass, which achieved a remarkable 1,754% five-year return. Find your next standout investment with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Trump Asserts That Costs Are Dropping. This Is Why That Could Harm the Economy

何时是抄底时机?华尔街分析师:英伟达关键底部可能在这里

Immunic: Fourth Quarter Financial Overview

International Seaways: Fourth Quarter Earnings Overview