2 Things to Appreciate About FRSH (and 1 Drawback)

Freshworks Stock: Recent Performance and Investor Sentiment

Freshworks shareholders have faced a challenging half-year, with the share price tumbling 45.6% to its current value of $7.17. This significant decline may leave investors reconsidering their strategies moving forward.

With the stock at these levels, is this a favorable moment to consider buying FRSH?

What Fuels the Debate Around FRSH?

Freshworks (NASDAQ:FRSH) began as a customer support platform and has since evolved into a robust suite of AI-driven software tools. The company now delivers cloud-based solutions that streamline customer service, IT management, sales, and marketing for businesses.

Key Strengths of Freshworks

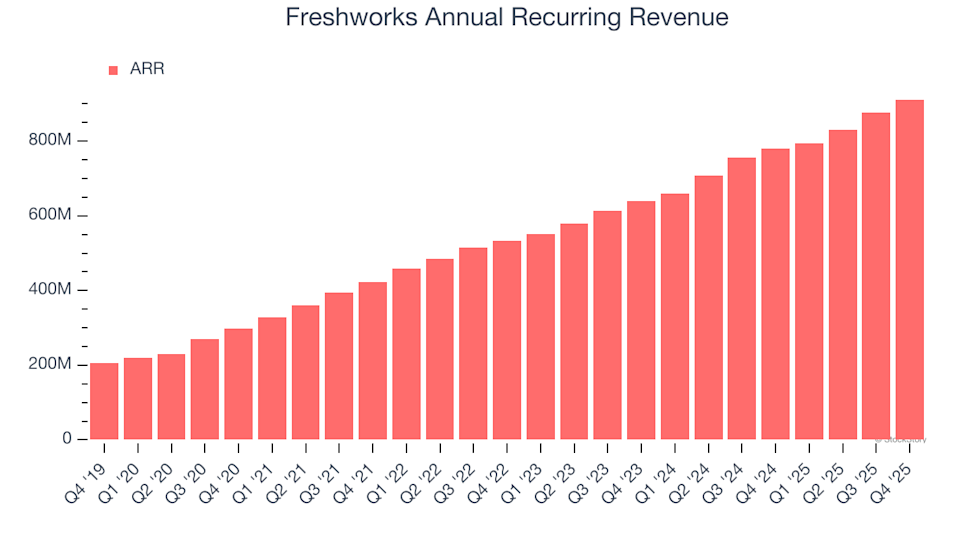

1. Consistent ARR Growth Supports Reliable Revenue

Unlike total revenue, which can be influenced by lower-margin services such as implementation fees, annual recurring revenue (ARR) focuses solely on contracted software subscriptions—providing a clearer picture of sustainable, high-margin income. In the fourth quarter, Freshworks reported ARR of $911.8 million, with an average annual growth rate of 17.7% over the past year. This steady expansion highlights the company’s ability to retain clients and secure long-term agreements, enhancing both revenue predictability and company valuation—qualities highly valued by investors in the SaaS sector.

2. Exceptional Gross Margins Reflect a Strong Business Model

The appeal of the SaaS model lies in its scalability—once the software is built, ongoing delivery costs are minimal, typically limited to infrastructure and support. Freshworks stands out with one of the highest gross margins in the industry, thanks to its efficient operations and pricing power. This financial strength allows the company to reinvest in innovation and sales, fueling further growth and profitability. Over the past year, Freshworks maintained an impressive 85% gross margin, meaning only $15.04 of every $100 earned went toward direct costs.

Investors pay close attention not only to current gross margins but also to their trajectory. Freshworks has improved its gross margin by 2.3 percentage points over the last two years—a notable achievement in the software space.

Potential Risk: Customer Retention

Customer Churn Could Impact Long-Term Growth

A major advantage of SaaS businesses is their ability to increase revenue from existing clients over time, which often justifies premium valuations. However, customer retention remains a critical factor in sustaining long-term growth.

Freshworks’s net revenue retention rate—a measure of how much existing customers spend compared to the previous year—stood at 105% in Q4. This indicates that, even without acquiring new clients, the company would have grown revenue by 5% over the past year.

While this retention rate suggests Freshworks is generally able to keep its customers, it falls short of the top-performing SaaS companies, which often achieve net retention rates exceeding 120%.

Conclusion: Is Freshworks a Buy?

On balance, Freshworks’s strengths outweigh its challenges. After the recent decline, the stock is trading at 2.1 times forward price-to-sales, or $7.17 per share. Should you consider investing now?

Building a Resilient Portfolio with High-Quality Stocks

Relying on just a handful of stocks can leave your investments vulnerable. Now is the time to diversify with top-tier assets before market conditions shift and attractive prices vanish.

Don’t wait for the next market swing. Discover our Top 5 Strong Momentum Stocks for this week—a handpicked selection of high-quality companies that have delivered a remarkable 244% return over the past five years (as of June 30, 2025).

This list features well-known leaders like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known success stories such as Exlservice, which achieved a 354% five-year return. Start your search for the next standout performer today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

US: Jobs data and Fed timing – ING

Shopify Inc. (SHOP) GMV Growth Reaccelerates as AI Integration Strengthens Investment Case