NVIDIA Surpasses Every Expectation in Fourth Quarter Results, Declares AI Boom Continues

NVIDIA Surpasses Expectations with Strong Q4 FY2026 Results

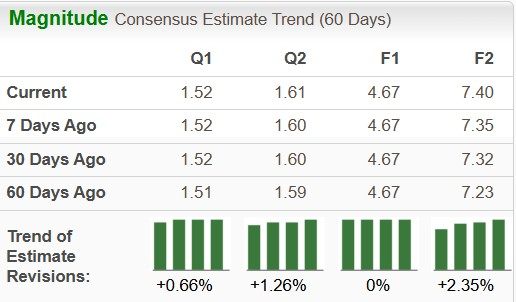

NVIDIA Corp. (NVDA), recognized as the leading force in generative AI-powered GPUs worldwide, posted impressive results for the fourth quarter of its fiscal 2026. The company reported adjusted earnings per share of $1.62, beating both the Zacks Consensus Estimate of $1.52 and last year’s $0.89 per share.

Total revenue reached $68.127 billion, exceeding the consensus forecast of $65.421 billion and significantly higher than the $39.3 billion reported a year earlier. This marks a 73.3% year-over-year increase for the quarter, continuing an eleven-quarter streak of revenue growth above 50% compared to the prior year.

Data Center Business Drives Growth

NVIDIA’s Data Center segment, which accounts for 91% of total revenue, saw a 75% year-over-year jump and a 21.7% increase from the previous quarter, reaching $62.3 billion. This surge was largely fueled by increased shipments of the Blackwell GPU computing platforms.

Within data center revenues, approximately $51.3 billion came from compute (GPU) sales, up 58% from the previous year, while networking revenue soared 263% year over year to nearly $11 billion.

Optimistic Outlook for Fiscal 2027

Looking ahead to the first quarter of fiscal 2027, NVIDIA projects revenue of $78 billion (plus or minus 2%), well above the Zacks Consensus Estimate of $69.25 billion. The company expects a non-GAAP gross margin of 75% (plus or minus 50 basis points) and non-GAAP operating expenses around $7.5 billion. Notably, this guidance excludes any sales from China.

AI Momentum Remains Strong

NVIDIA continues to benefit from substantial investments by AI hyperscalers. CFO Colette Kress noted that hyperscalers contributed just over half of Data Center revenue in Q4, with the remainder coming from a diverse set of customers.

Four of NVIDIA’s largest clients—Microsoft (MSFT), Alphabet (GOOGL), Meta Platforms (META), and Amazon (AMZN)—plan to collectively invest $650 billion in AI infrastructure in 2026, representing a 71.1% increase in capital expenditures for the AI sector compared to the previous year.

CEO Jensen Huang addressed concerns about AI disrupting the enterprise software industry, stating his belief that AI agents will enhance, not replace, existing software tools, making users more productive.

Innovation and Future Plans

At the annual CES technology event in January, NVIDIA introduced its new AI superchip, Vera Rubin. This rack-scale system is expected to deliver ten times the performance per watt compared to its predecessor, Grace Blackwell.

Vera Rubin is scheduled to begin shipping in the second half of 2026. NVIDIA also plans to unveil its roadmap for Rubin Ultra, anticipated in late 2027, and Feynman AI chips, set for a 2028 launch. The company anticipates global AI infrastructure spending to reach between $3 trillion and $4 trillion by the end of the decade, reflecting robust demand.

Diversification and New Opportunities

NVIDIA is expanding its reach into advanced driver-assistance systems, autonomous vehicles, and robotics. Beyond its strong data center and gaming businesses, the automotive sector—especially self-driving and electric vehicles—is emerging as a significant growth driver.

Automotive revenue climbed 6% year over year to $604 million in Q4 FY2026. Management is optimistic that this segment could become a multi-trillion-dollar opportunity in the future.

The Gaming division generated $3.7 billion in sales last quarter, up 47% year over year, while the professional visualization segment saw revenue rise 159% to $1.32 billion.

NVDA Stock: Strong Financials and Growth Potential

NVIDIA boasts a return on equity (ROE) of 99.24%, far outpacing the S&P 500’s 17.15% and the industry average of 2.32%. The company’s forward price-to-earnings (P/E) ratio stands at 26.05, compared to 32.62 for the industry and 19.44 for the S&P 500. Over the next 3-5 years, NVIDIA’s expected EPS growth rate is 47%, well above the S&P 500’s 16.3%.

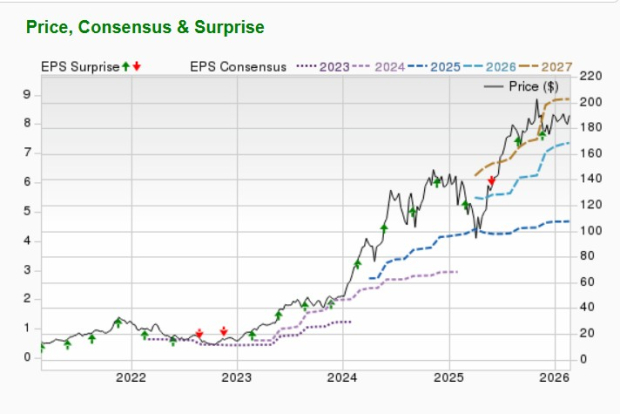

For the current fiscal year ending January 2027, NVIDIA anticipates revenue and earnings growth rates of 47.5% and 58.5%, respectively. The Zacks Consensus Estimate for this year’s earnings has increased by 0.7% in the past week.

Short-Term Upside for NVIDIA Shares

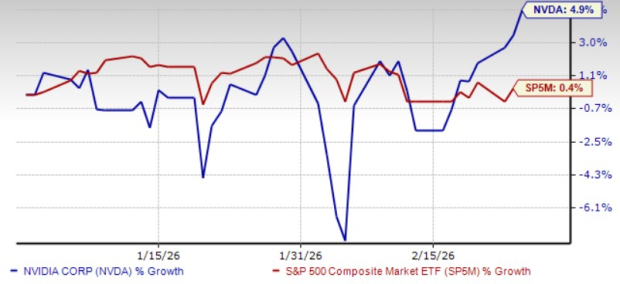

So far this year, NVIDIA shares have returned 4.9%. Brokerage firms’ short-term average price target for the stock suggests a potential increase of 30.7% from the recent closing price of $195.56, with target prices ranging from $140 to $352. This implies a possible upside of up to 80% and a downside risk of 28.4%.

Why Consider Investing in NVIDIA?

NVIDIA currently holds a Zacks Rank #2 (Buy).

The company stands out as a rare investment opportunity, combining a track record of strong execution with significant untapped potential in the AI revolution. The global AI infrastructure market’s rapid expansion, along with NVIDIA’s positive outlook and business resilience—even amid revenue declines in China—make the stock particularly attractive. As a result, analysts expect the average target price for NVIDIA shares to see meaningful near-term gains.

Discover Zacks Top 10 Stocks for 2026

There’s still time to get early access to Zacks’ top 10 stock picks for 2026, curated by Director of Research Sheraz Mian. This portfolio has delivered remarkable and consistent returns.

From its inception in 2012 through November 2025, the Zacks Top 10 Stocks portfolio achieved a gain of +2,530.8%, outpacing the S&P 500’s +570.3% by more than four times.

Sheraz Mian has carefully selected the best 10 stocks from over 4,400 companies covered by Zacks Rank for 2026. Be among the first to access these newly released high-potential picks.

Additional Resources and Free Reports

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

5 Important Facts to Be Aware of Before the Stock Market Starts

Bitcoin’s 4-Year Cycle Still Intact as On-Chain Signals Realign

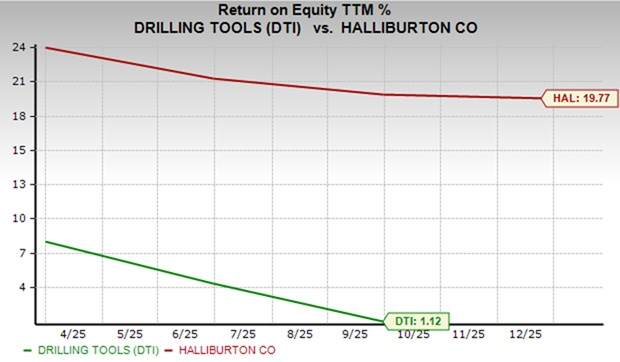

DTI or HAL: Which Oilfield Services Stock Provides Greater Value?

NVIDIA’s China AI Market Projections and Rubin Ramp Timeline Clash in Earnings Call