CCL Achieves All-Time High Prices Amidst Low Market Confidence: What Factors Are Fueling the Demand?

Carnival Corporation Achieves Unprecedented Financial Results in 2025

Carnival Corporation & plc reported its strongest financial year ever in 2025, setting new records in revenue, yields, operating profit, and EBITDA. The company’s net income for the year surpassed $3 billion, marking a 60% increase from the previous year. Yields climbed by over 5.5%, outpacing earlier projections. Notably, each quarter of the year contributed to these exceptional results, demonstrating consistent performance across Carnival’s global operations.

Despite ongoing concerns about U.S. consumer confidence throughout 2025, demand for cruises remained robust. Management pointed out that both North American and European markets saw all-time high pricing, and booking activity for 2026 and 2027 reached unprecedented levels in the last three months. Customer deposits rose 7% year-over-year, hitting a new peak by year-end. Additionally, onboard revenue per guest in the fourth quarter was significantly higher than the previous year, fueled by strong last-minute bookings.

The company credits its success to disciplined revenue strategies and the advantages of a diverse brand lineup. Leadership emphasized prioritizing overall revenue growth over occupancy rates, which helped maintain strong pricing and boost both ticket sales and onboard spending. Bundled packages and targeted promotions have also been effective in balancing passenger volume and profitability across different routes and regions.

Outlook for 2026

Looking ahead, Carnival expects yields to grow by around 2.5% in 2026, or about 3% after adjusting for accounting and deployment changes. This forecast takes into account increased industry capacity in the Caribbean and ongoing economic uncertainties. With no new ships scheduled for delivery in 2026, the company anticipates that cost increases will be kept in check through ongoing efficiency measures and economies of scale.

Overall, management remains optimistic about the long-term appeal of cruising, highlighting its value compared to land-based vacations and Carnival’s adaptability in various markets. With a large portion of 2026 bookings already secured at higher prices and continued strength in onboard spending, Carnival is well-positioned to build on its record-breaking performance.

CCL Stock Performance, Valuation, and Analyst Estimates

Over the past three months, Carnival’s share price has surged 24.7%, significantly outpacing the industry average gain of 5%. During the same period, competitors such as Royal Caribbean Cruises Ltd., Norwegian Cruise Line Holdings Ltd., and OneSpaWorld Holdings Limited saw their stocks rise by 17.8%, 29.9%, and 7.1%, respectively.

Three-Month Stock Price Comparison

Source: Zacks Investment Research

Currently, CCL trades at a forward 12-month price-to-earnings (P/E) ratio of 12.18, which is notably lower than the industry average of 16.15. In comparison, Royal Caribbean, Norwegian Cruise, and OneSpaWorld have forward P/E ratios of 16.92, 9.12, and 19.25, respectively.

Forward P/E Ratios: CCL vs. Industry Peers

Source: Zacks Investment Research

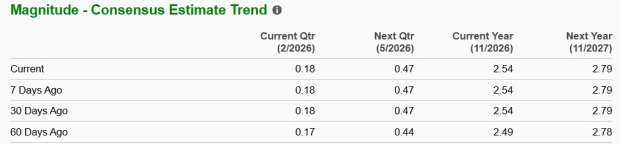

Analyst sentiment for Carnival remains positive, with the Zacks Consensus Estimate for fiscal 2026 earnings per share rising from $2.49 to $2.54 over the past two months. This upward revision reflects growing confidence in the company’s near-term outlook.

EPS Forecast Trend for CCL

Source: Zacks Investment Research

Carnival is projected to deliver a 12.9% increase in earnings for fiscal 2026. By comparison, Royal Caribbean, Norwegian Cruise, and OneSpaWorld are expected to achieve year-over-year earnings growth of 15.7%, 15.9%, and 12.1%, respectively, in 2026.

CCL currently holds a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Tecogen's March 18th Print: Closing the Expectation Gap

Buenaventura: Fourth Quarter Earnings Overview

Fidelity Low-Priced Stock Fund Q4 2025: An Examination of Portfolio Distribution