Marriott’s Shares Rise Even as Trading Volume Falls 39.53% to 263rd Place, Following Analysts’ Upgraded Profit Forecast

Marriott Market Overview

On February 26, 2026, Marriott (MAR) ended the trading session up 0.90%, despite a significant drop in trading volume. The day’s volume reached $0.52 billion, marking a 39.53% decrease from the previous session and ranking 263rd in daily activity. This price increase, even with lower volume, points to investor confidence, likely fueled by recent analyst upgrades and earnings news. The overall market remained quiet, with investors adopting a cautious stance ahead of major corporate announcements.

Main Influences on Performance

Analyst Upgrades and Earnings Forecasts

Marriott’s stock benefited from several analyst upgrades and improved earnings projections. Zacks Research raised its Q1 2026 EPS estimate to $2.54 per share, up from $2.49, reflecting stronger expectations. Other firms, including JPMorgan Chase, Barclays, and Evercore, also increased their price targets, with JPMorgan setting its target at $356. Citigroup and Truist Financial followed suit, signaling confidence in Marriott’s operational strength and growth prospects. The consensus EPS estimate for fiscal year 2026 is $11.50, and Q1 guidance is now between $2.50 and $2.55, indicating a more precise outlook.

Expansion Initiatives and Operational Progress

Investor sentiment was further lifted by Marriott’s ongoing expansion and operational achievements. The company recently entered new markets, such as launching the Le Méridien Dehradun Resort & Spa in India, reinforcing its long-term growth plans. Management’s focus on technology, including AI-driven efficiencies, has attracted industry attention. Marriott reported a 4.1% year-over-year revenue increase in Q4 2025, demonstrating its ability to meet travel demand and optimize assets. The FY2026 guidance includes an expected EBITDA margin of 9.93%, highlighting the company’s commitment to profitability amid competition.

Insider Activity and Institutional Investment

Recent insider transactions have sent mixed signals to investors. CEO Anthony Capuano sold 63,000 shares at an average price of $359.22, reducing his stake by 35.67%, while David S. Marriott sold 4,747 shares. Although such sales are not unusual, they may be viewed as a negative sign by some. However, institutional investors countered this with increased holdings—Woodline Partners LP and Intech Investment Management LLC boosted their stakes by 39.6% and 21.8%, respectively, in Q1 2026. With institutional ownership at 70.70%, confidence in Marriott’s long-term prospects remains strong despite short-term fluctuations.

Earnings Trends and Guidance Changes

Marriott’s recent earnings have been somewhat inconsistent. Q4 2025 EPS came in at $2.58, slightly below the consensus of $2.61, but revenue surpassed expectations at $6.69 billion, beating estimates by $20 million. Over the last four quarters, the average EPS surprise was just 0.02%, indicating steady but modest performance. Looking forward, Zacks Research has lowered its 2027 EPS forecasts, including reductions for Q1 and Q2, and adjusted the full-year estimate to $12.72 from $12.81. These changes introduce some uncertainty for long-term growth projections, tempering optimism about the near-term outlook.

Competitive Position and Valuation

Marriott’s stock remains highly valued, with a price-to-earnings ratio of 36.61 and a PEG ratio of 3.03, suggesting investors are paying a premium for anticipated growth. The company’s market cap of $92.06 billion makes it a major player in the hospitality industry, competing with Hilton Worldwide and InterContinental Hotels Group. Analysts point to Marriott’s strong brand and diverse portfolio as key advantages, especially in luxury and premium segments. However, a negative return on equity of 84.23% in Q4 2025 raises concerns about capital efficiency, emphasizing the need for ongoing cost management and asset optimization.

Upcoming Catalysts and Potential Risks

The Q1 2026 earnings report, scheduled for May 5, 2026, is expected to be a pivotal event for Marriott’s stock. Analysts are watching to see if the company can achieve or surpass the EPS estimate of $2.55 and revenue target of $6.57 billion. Marriott’s participation in the J.P. Morgan Gaming, Lodging, Restaurant & Leisure forum on March 12 may also shed light on its strategic priorities and margin expansion plans. Risks include possible declines in travel demand due to economic uncertainties and the effects of rising interest rates on capital spending. Nevertheless, Marriott’s robust balance sheet, with a 28.24% dividend payout ratio and 10.68% insider ownership, offers some protection against short-term challenges.

Conclusion

Marriott’s stock performance is shaped by a mix of analyst optimism, strategic growth, and insider activity. While recent upgrades and operational successes support a positive outlook, cautious guidance for 2027 and insider sales introduce some uncertainty. Investors will be closely monitoring upcoming earnings and management commentary to gauge the sustainability of Marriott’s current trajectory.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Can Ethereum capture the AI agent market set to hit $236B by 2034?

Diversified Energy Achieves Milestone Year: What Was Anticipated and Future Outlook

Nvidia's Results: Surpassing Expectations but Failing to Make a Significant Impact

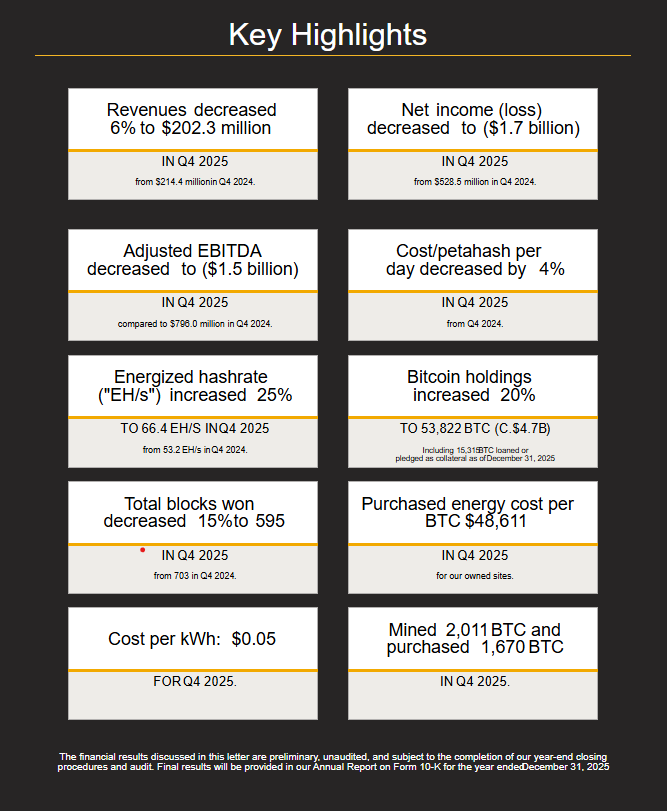

Bitcoin miner MARA posts $1.7B quarterly loss on BTC slump