Fifth Third’s 0.8% Gain Defies 302nd-Ranked Trading Volume as Merger Drives Investor Caution

Market Snapshot

On February 26, 2026, shares of Fifth Third BancorpFITB+0.80% (FITB) rose 0.80%, closing at $51.86, despite a relatively low trading volume of $0.46 billion, which ranked 302nd in daily trading activity. The stock’s modest gain contrasted with broader market volatility, as it outperformed the S&P 500’s 0.93% year-to-date return. The upward movement came amid mixed investor sentiment, with pre-market prices dipping 0.12% ahead of the Comerica merger’s finalization. The company’s 3.25% dividend yield, supported by 51 consecutive years of uninterrupted payments, provided a stabilizing factor for income-focused investors.

Key Drivers

Earnings Outperformance and Strategic Momentum

Fifth Third’s Q4 2025 results underscored its operational resilience, with earnings per share (EPS) of $1.04 exceeding forecasts by 4% and revenue hitting $2.34 billion, in line with expectations. The 5% year-over-year increase in adjusted revenues highlighted the bank’s ability to navigate macroeconomic headwinds, particularly in a sector where peer performance has been uneven. This momentum was further amplified by the impending Comerica merger, scheduled for February 1, 2026, which is projected to generate $850 million in expense synergies and bolster market share in key regions. Analysts noted that the acquisition aligns with the bank’s long-term strategy to expand its commercial and wealth management services, positioning it to capitalize on higher net interest income (NII) in a rising rate environment.

Dividend Stability and Investor Sentiment

The bank’s commitment to dividend continuity, with a current yield of 3.25%, remains a critical draw for long-term investors. Fifth Third’s ability to maintain payouts for 51 consecutive years reflects robust capital management and confidence in its earnings trajectory. However, this stability was partially offset by cautious sentiment ahead of the merger integration. Pre-market trading saw a 0.12% decline, as investors weighed potential execution risks and regulatory hurdles. While the transaction is expected to enhance returns on tangible common equity (ROTCE) and drive mid-single-digit loan growth, the short-term dip suggests lingering skepticism about the costs of integration and the timing of synergy realization.

Forward Guidance and Financial Metrics

Fifth Third’s ambitious 2026 targets—19% ROTCE, $8.6–8.8 billion in NII, and mid-single-digit loan growth—underscore its aggressive cost discipline and asset optimization strategies. These metrics align with broader industry trends toward efficiency, particularly as banks adjust to tighter credit conditions and elevated funding costs. The company’s 30.19% profit margin and 12.19% return on equity (ROE) further reinforce its competitive positioning. However, the absence of guidance for specific cost-cutting measures or capital allocation strategies in recent disclosures may have contributed to the muted post-earnings rally.

Sector Context and Valuation Dynamics

The financial sector’s broader underperformance, with the S&P 500 Financials Index trailing the broader market, created a challenging backdrop for Fifth Third’s stock. Despite its strong fundamentals, the bank’s forward P/E ratio of 13.14 and price-to-book ratio of 2.33 suggest a valuation that remains anchored to conservative expectations. Analysts at Evercore ISI Group recently raised their price target to $57 from $52, citing the merger’s potential to unlock value, but emphasized that the stock’s upside depends on execution risks and macroeconomic stability. Meanwhile, the bank’s $850 million in merger-related synergies must be weighed against its $4.56 billion in cash reserves, raising questions about balance sheet flexibility in a potential downturn.

Long-Term Strategic Positioning

Fifth Third’s strategic focus on high-margin businesses, such as wealth management and commercial banking, positions it to benefit from sustained demand for fee-based services. The bank’s 2026 guidance for NII and ROTCE suggests a deliberate shift toward asset quality and cost efficiency, a trend echoed across the industry as banks recalibrate to a post-pandemic environment. However, the absence of detailed risk management disclosures in recent filings—particularly regarding credit exposure and interest rate sensitivity—could limit investor confidence in volatile markets. The bank’s ability to translate its merger synergies into tangible earnings growth will be a key determinant of its long-term trajectory.

In summary, Fifth Third’s stock performance reflects a balance between short-term strategic execution risks and long-term earnings potential. While the Comerica merger and robust dividend policy provide a foundation for investor optimism, the market’s cautious response underscores the need for clear communication on integration timelines and capital deployment strategies. As the bank navigates a complex regulatory and economic landscape, its ability to maintain operational discipline and deliver on ambitious financial targets will remain critical to sustained outperformance.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Diversified Energy Achieves Milestone Year: What Was Anticipated and Future Outlook

Nvidia's Results: Surpassing Expectations but Failing to Make a Significant Impact

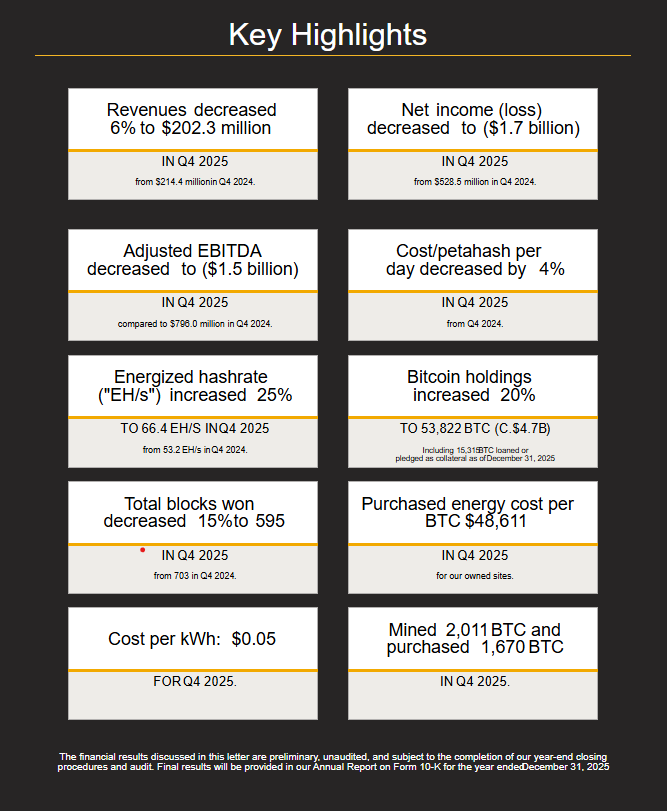

Bitcoin miner MARA posts $1.7B quarterly loss on BTC slump

Forex Today: US Dollar holds steady amid worsening market sentiment