After the Valuation Crash of Software Stocks, Is the Era of Major AI Mergers and Acquisitions Coming?

Deutsche Bank believes that most companies' AI implementation progress is currently far behind market expectations, while volatility in AI-related market capitalization is driving companies to accelerate their M&A strategies.

According to Wind Chaser Trading Desk, on February 26, the Deutsche Bank research team published a report pointing out that recent stock market fluctuations and the sell-off of AI concept stocks have forced CEOs to urgently formulate AI strategies and clearly articulate these strategies to investors.

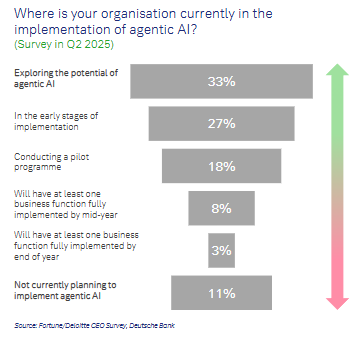

However, by 2025, only 11% of companies may have fully implemented at least one AI-related business function. This means most CEOs are under immense pressure to accelerate AI adoption. In the face of AI rollout pressure, mergers and acquisitions are becoming a core strategy for many CEOs to catch up with their peers.

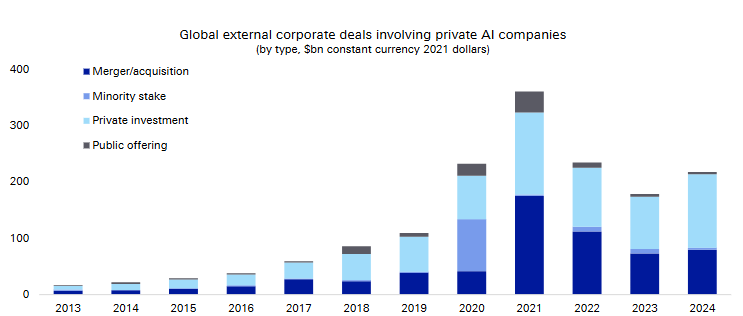

Data shows that the scale of global external corporate transactions involving private AI companies (including acquisitions, minority equity investments, private financing, and public offerings) has surged from virtually negligible levels around 2013 to nearly $40 billion annually between 2021 and 2024.

(Global external corporate transaction scale for private AI companies)

(Global external corporate transaction scale for private AI companies)

The report suggests that three main trends—unprecedented software sector repricing, continued intensification of private AI company M&A activity, and increasing divergence in global M&A paces—will profoundly impact asset allocation decisions over the next one to two years. Regulatory uncertainty and regional divergence in the macro interest rate environment will be the biggest variables affecting M&A pace and pricing.

Most Enterprises Lag Severely in AI Adoption, CEOs Under Great Pressure

Deutsche Bank points out that current AI adoption is uneven, with startups and large enterprises being the frontrunners. Citing survey data for Q2 2025:

Only 8% of companies said they would fully implement at least one AI business function by mid-year;

Only 3% expect to complete this by the end of the year;

11% of companies explicitly stated they had no plans to implement intelligent agent AI.

The International Monetary Fund (IMF) estimates that about 40% of jobs globally will be affected by AI, especially "cognitive" jobs. Analyzing keyword frequency in S&P 500 companies' earnings calls:

AI and machine learning remain the top trending topics, with layoffs, chip shortages, and R&D investment also among the fastest-growing topics;

M&A discussions have rebounded significantly after hitting a low following the spring 2025 tariff impact, and their frequency of mention has surpassed that of dividends and buybacks;

The fastest-growing capital allocation theme in the past six months is capital expenditure and R&D.

(Increase in mentions of specific topics in S&P 500 earnings calls)

From an individual company perspective, leading companies across industries such as Marriott International, Amgen, and S&P Global have all clearly expressed a positive strategic stance towards AI in their earnings reports, viewing it as a net business positive rather than a threat.

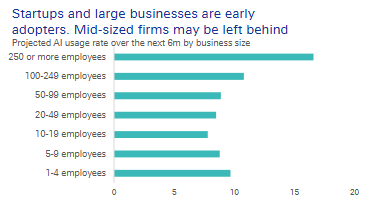

It is worth noting that medium-sized enterprises with 50 to 249 employees have a significantly lower AI usage rate.

They lack both the agility and focus of startups and the resources and data scale of giants, making them the most likely to fall behind in the race. Acquiring ready-made AI capabilities through M&A is a realistic shortcut for them.

Software Valuations Plummet, M&A Window Opens Quietly

Fortunately, the market is providing an acquisition window.

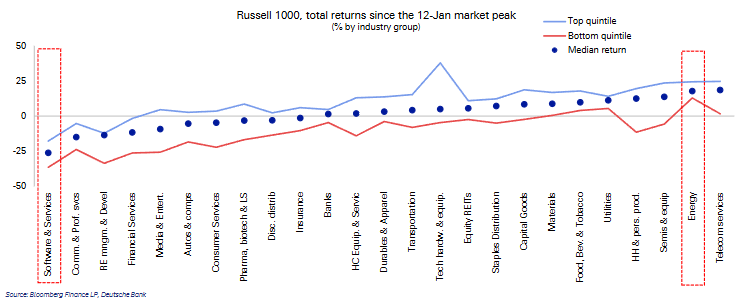

Since the market peaked in mid-January this year, the software and services sector has been the worst-performing industry group in the Russell 1000 Index, with a median decline of 25%. Its valuation ranking has dropped from third to ninth place.

(Since January 12, software has been the worst-performing sector in the Russell 1000 Index)

(Since January 12, software has been the worst-performing sector in the Russell 1000 Index)

More importantly, when adjusted for growth expectations, software company valuations have become relatively average. In the US market, their price/earnings-to-growth ratio ranking has plummeted from 7th to 17th, and in Europe from 3rd to 15th. The valuation bubble has been significantly squeezed, giving corporate buyers more leverage at the negotiating table.

(Based on PEG ratio adjusted for growth expectations, valuation ranking dropped sharply from 7th to 17th)

(Based on PEG ratio adjusted for growth expectations, valuation ranking dropped sharply from 7th to 17th)

Looking at the M&A outlook, the US will likely hold steady, while Europe will see “uneven” conditions. Deutsche Bank’s M&A leading indicators show:

United States: The rebound in M&A activity in Q1 may slow as we enter Q2, due to increased policy uncertainty and mixed signals from capital issuance;

(M&A momentum may slow in Q2 2026)

Eurozone: Rising sovereign bond yields are dragging down the M&A outlook, putting short-term pressure on deals;

United Kingdom: Benefiting from lower bond yields and strong stock market performance, the M&A recovery pace is expected to outstrip current market expectations.

(Forecast for the number of M&A deals in the Eurozone and UK over the next three months)

So what kind of AI companies are most likely to be acquired? Deutsche Bank believes that the more specialized an AI company is, the more attractive it is to industry giants. These companies need tools that deeply address specific vertical fields and solve concrete problems.

Private Equity Dominates Deals, but Exits Are Essential

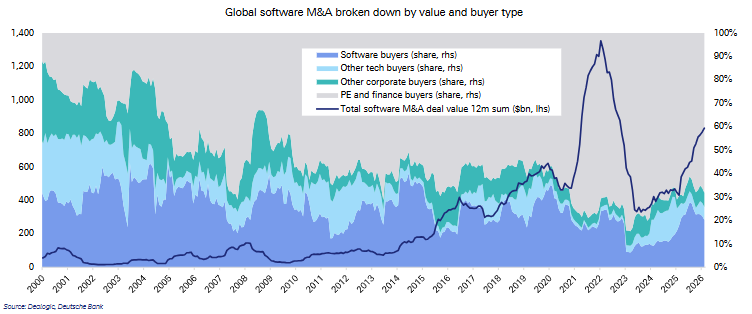

A key structural change in the market is that financial buyers such as private equity have dramatically increased their share of global software M&A deals.

Data shows that the share of financial buyers such as private equity has soared from 28% in the 2000s to 72% in the 2020s, while non-tech companies’ share of software M&A has shrunk from 17% to 5%.

(Global software M&A by amount and buyer type)

(Global software M&A by amount and buyer type)

These large private equity deals will eventually need an exit. Selling assets to entities seeking AI capabilities will be a key exit route.

Citing data, the report notes that between 2022 and 2024, M&A deals accounted for an average of 42% of total external corporate transactions for private AI companies, while IPOs accounted for only 3%.

Many AI challenger companies are small and continue to operate at a loss, while large incumbents have proprietary data, trusted brands, and scale advantages—especially in highly complex regulated industries, which startups can hardly replicate.

Risks and Lessons from History

M&A is not a panacea. Integration failures, cultural clashes, loss of key talent, and high ongoing investment are all risks.

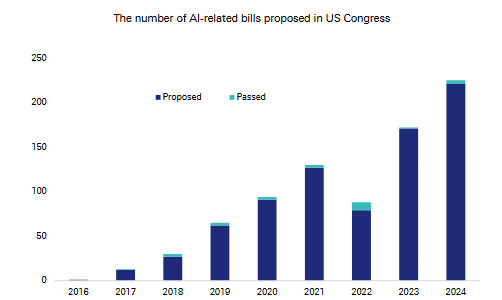

Deutsche Bank points out that the number of AI-related bills introduced in the US Congress soared from about 80 in 2022 to over 200 in 2024, indicating rising regulatory uncertainty.

(Growth in the number of AI-related bills introduced in the US Congress)

(Growth in the number of AI-related bills introduced in the US Congress)

History provides a long-term perspective. During the tech boom of the 1990s, the Nasdaq experienced several corrections of more than 10%, but still posted an average annual gain of 32%.

At that time, regulatory evolution ultimately reinforced scale effects, leading to market concentration. This time, the giants with capital, data, and scale advantages may once again hold a favorable position in the long AI race.

The report argues that what is unique about the current moment is that as the AI wave rises, large tech companies possess unusually abundant free cash flow. They are among the few entities in the world that can afford massive AI capital expenditures and withstand potential losses. The entry threshold for this race has been high from the very start.

Ultimately, for investors, the AI M&A cycle is moving from the conceptual phase to tangible implementation. Valuation resets are creating potential strategic buying opportunities, but regulatory risk, opaque pricing of unlisted targets, and macro uncertainties remain the main constraints. In the medium term, companies capable of proactively steering AI M&A strategies will gain the upper hand as the competitive landscape is reshaped.

~~~~~~~~~~~~~~~~~~~~~~~~

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Nutanix's $250M Flow: A Liquidity Test for AI Infrastructure Stocks

GBP/USD: Returns to range following unsuccessful breakout – UOB

RBC's Initiation: Assessing Lilly's Path to Obesity Market Leadership

Can Ethereum’s price rally to $2,400 after BlackRock’s latest bet?