Jefferson Capital, Inc. (JCAP): A Bear Case Theory

We came across a bearish thesis on Jefferson Capital, Inc. on The Illiquid Edge’s Substack. In this article, we will summarize the bears’ thesis on JCAP. Jefferson Capital, Inc.'s share was trading at $22.07 as of February 11th. JCAP’s trailing P/E was 9.26 according to Yahoo Finance.

While Jefferson Capital screens attractively at a roughly 20% levered free cash flow yield and has delivered 39% YoY operating income growth, a deeper look at the underlying unit economics suggests the business is less compelling than headline metrics imply.

Mature vintages from 2017–2020 generated approximately 2x gross recoveries and 27%+ IRRs before operating costs, but cash operating expenses average about 40% of collections. After incorporating these costs and discounting long-dated recoveries, implied unlevered returns compress into the high single digits.

Even assuming a 60% after-tax recovery margin, modeled equity values cluster around $300–400 million after subtracting $1.3–1.4 billion of liabilities, suggesting limited upside relative to the current valuation. Although Jefferson Capital appears inexpensive versus peers like Encore Capital and PRA Group on surface multiples, its capital-intensive, reinvestment-heavy model resembles a capital-recycling operation rather than a true compounding business.

Nearly all excess cash flow must be reinvested to sustain portfolio size, as evidenced by a $300 million loan book purchase in late 2025 that absorbed prior cash generation. With sustainable through-cycle ROEs likely in the 12–13% range and governance firmly controlled by its private equity sponsor, Jefferson Capital arguably merits valuation closer to book value than its current premium. Without structurally higher portfolio returns or improved capital allocation, the stock appears overvalued.

SOFI’s stock price has appreciated by approximately 59.79% since our coverage. The Illiquid Edge shares a contrarian but emphasizes on weak underlying unit economics and reinvestment-heavy capital structure at Jefferson Capital, Inc. (JCAP).

As per our database, 16 hedge fund portfolios held JCAP at the end of the third quarter which was 22 in the previous quarter. While we acknowledge the risk and potential of JCAP as an investment, our conviction lies in the belief that some AI stocks hold greater promise for delivering higher returns and doing so within a shorter time frame.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Microsoft Stock Testing 2 Key Levels as Options Traders Pounce

Elon Musk's xAI to repay $3 billion debt early, Bloomberg News reports

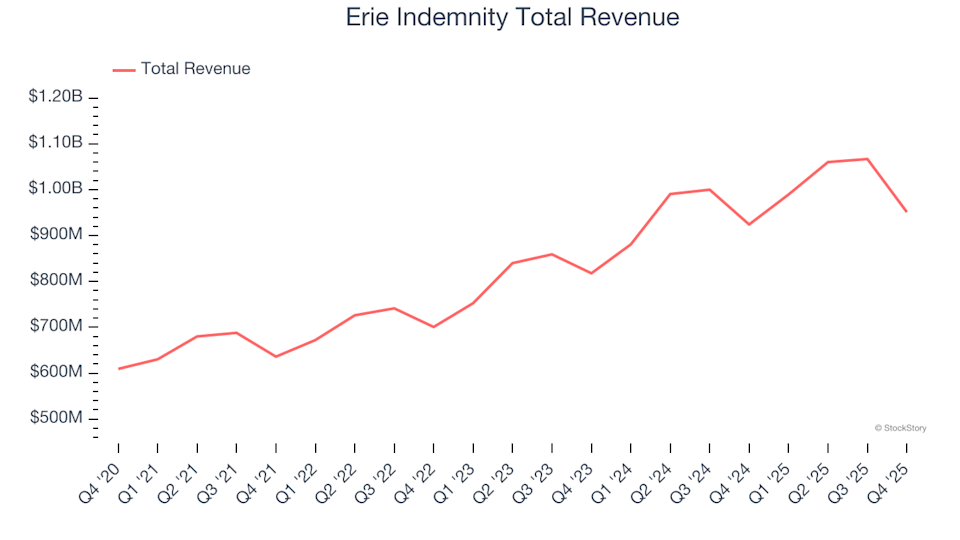

Q4 Summary: Erie Indemnity (NASDAQ:ERIE) Compared to Other Property and Casualty Insurance Shares

Top 10 Crypto Assets In Accumulation Zone: RENDER and BONK Lead the List