Olin Corporation (OLN): A Bull Case Theory

We came across a bullish thesis on Olin Corporation on Penny on the Dollar’s Substack. In this article, we will summarize the bulls’ thesis on OLN. Olin Corporation's share was trading at $25.68 as of February 12th. OLN’s trailing and forward P/E were 19.62 and 42.73 respectively according to Yahoo Finance.

Olin Corporation manufactures and distributes chemical products in the United States and internationally. OLN recently issued preliminary Q4 2025 guidance, projecting adjusted EBITDA of approximately $67 million versus prior expectations of $120 million, representing a 42% miss at the midpoint. The shortfall was concentrated in Chlor Alkali Products and Vinyls, driven by an extended planned maintenance turnaround at Freeport, Texas, unplanned downtime from a third-party raw material supply disruption, and weaker-than-expected pipeline chlorine demand.

While the operational disruptions at Freeport have been resolved, the temporary supply issues and maintenance are considered one-off events that do not impair Olin’s long-term business model. The more notable variable is chlorine demand, which could indicate either a short-term lull or a broader industrial slowdown; the trajectory into 2026 remains uncertain. Management, led by CEO Ken Lane, has emphasized operating assets safely, meeting cost reduction targets, and adhering to a disciplined value-first commercial approach, signaling a strategic shift from the old Olin that might have chased volume into an oversupplied market.

The company is now managing the cycle rather than capitulating to it, preserving pricing power and structural value. Despite the disappointing guidance, Olin remains an asymmetric deep-value opportunity, trading below the replacement cost of its Gulf Coast assets and offering exposure to a housing-driven demand recovery, effectively providing defense-contractor-like stability in a commoditized chemical market.

While the timeline for recovery has extended, the underlying thesis remains intact, and the recent weakness presents a potential buying opportunity. For patient investors, the combination of undervalued assets, disciplined management, and cyclical mispricing supports a favorable long-term risk/reward setup, with the current share price already reflecting much of the near-term bad news.

Previously, we covered a

Olin Corporation is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

US tariff lawsuits returned to trade court to determine next steps

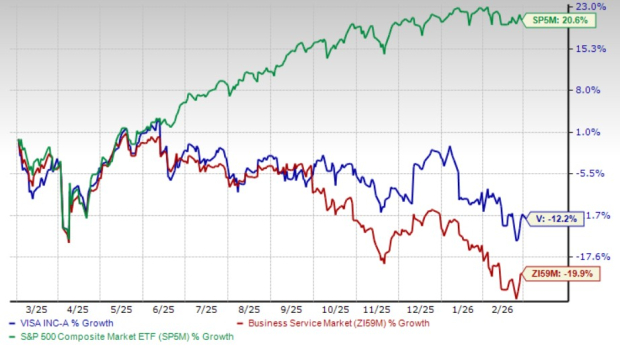

Why Visa's Prisma and Newpay Deals Come at a Critical Moment

Is Palomar (PLMR) a Solid Growth Stock? 3 Reasons to Think "Yes"