Sasol Limited (SSL): A Bull Case Theory

We came across a bullish thesis on Sasol Limited on Penny on the Dollar’s Substack. In this article, we will summarize the bulls’ thesis on SSL. Sasol Limited's share was trading at $7.68 as of February 12th. SSL’s trailing and forward P/E were 11.64 and 7.81 respectively according to Yahoo Finance.

Sasol Limited operates as a chemical and energy company. SSL is one of the most controversial and overlooked opportunities in global energy, trading at an enterprise value of just 2.7x EBITDA, a 60–70% discount to its developed-market chemical peers like LyondellBasell and Dow. Universally criticized for its coal-to-liquids operations, high CO2 emissions, South African jurisdiction, and junk credit rating, the market prices Sasol as if it is heading toward bankruptcy.

Much of this fear stems from the so-called “Gas Cliff” in 2028, when Mozambican gas supplies powering its Secunda facility may run low, combined with looming carbon taxes that could impose billions in costs. Operational challenges, including poor coal quality and underperforming gasifiers, further reinforce the bearish narrative.

Despite these concerns, Sasol’s fundamentals suggest a different story. Its Energy business in South Africa generates substantial cash flow, naturally hedged by costs in Rand versus revenues linked to the U.S. dollar. The International Chemicals division, while currently under pressure, has aggressively cut costs, expanded margins, and is poised to benefit from a global chemical cycle recovery.

A critical engineering solution—the destoning plant—comes online in December 2025, removing rocks from coal before gasification, which is expected to restore production above 7.1 million tons. If successful, Sasol could re-rate to 3.5–4x EBITDA, implying a share price of $10, with a bull case of $14 per share if chemicals and operations perform optimally.

Key catalysts in 2026 include operational updates from the destoning plant, potential dividend resumption as net debt declines, and clarity on the Richards Bay LNG terminal to mitigate the gas risk.

While geological, regulatory, and macro risks remain, the market is dramatically mispricing a solvent company with funded fixes and tangible assets. Sasol represents a deeply asymmetric investment, offering potentially 100% upside against limited downside, making it a compelling high-risk, high-reward special situation.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

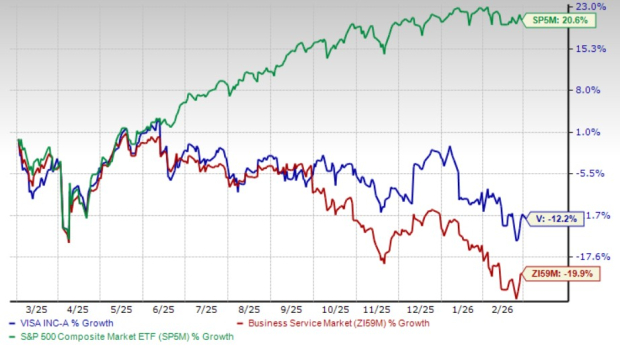

Why Visa's Prisma and Newpay Deals Come at a Critical Moment

Is Palomar (PLMR) a Solid Growth Stock? 3 Reasons to Think "Yes"

Fabrinet Eyes 800ZR and Co-Packaged Optics as Growth Catalysts

Stantec (STN) is an Incredible Growth Stock: 3 Reasons Why