Canadian Pacific Kansas City Limited (CP): A Bull Case Theory

We came across a bullish thesis on Canadian Pacific Kansas City Limited on Roche Capital’s Substack by Pedro Ortiz. In this article, we will summarize the bulls’ thesis on CP. Canadian Pacific Kansas City Limited's share was trading at $83.71 as of February 12th. CP’s trailing and forward P/E were 25.21 and 21.79 respectively according to Yahoo Finance.

Canadian Pacific Kansas City Limited, together with its subsidiaries, owns and operates a transcontinental freight railway in Canada, the United States, and Mexico. CPKC has emerged as a compelling long-term investment following a highly disciplined operational performance in 2025. The company reported C$15.1 billion in revenue, a 4 percent increase over 2024, with revenue ton-miles also up 4 percent, reflecting primarily organic growth. Operational efficiency remains best-in-class, with an adjusted operating ratio of 59.9 percent for the year and a record 55.9 percent in Q4, underscoring superior cost control.

Adjusted EPS rose 8 percent to C$4.61, outpacing revenue growth, while operating cash flow reached C$5.3 billion, with profit-to-cash conversion at 75 percent and a target of 90 percent by 2028. CPKC’s unique integrated network linking Canada, the U.S., and Mexico positions it to capture trilateral trade flows efficiently, with merger synergies already generating C$1.2 billion in 2025 and expected to exceed C$1.4 billion by 2026.

Operational improvements post-merger include a 13–14 percent increase in train and car traffic speeds, higher locomotive productivity, and industry-leading safety with 0.85 accidents per million train miles. The company’s portfolio is well-diversified, spanning bulk commodities, general cargo, and intermodal transport, while intermodal and Mexico-focused corridors show early-stage but promising growth.

ROIC is improving on the larger post-merger capital base, with incremental returns above cost of capital, supported by disciplined investment and a 5 percent share buyback program. Risks include tariffs, trade agreement negotiations, sector consolidation, agricultural volatility, and execution in new intermodal services. For long-term investors, CPKC offers a durable, high-barrier infrastructure business with predictable earnings growth, strong management, and a clear path to compounding value, though near-term entry requires prudence given the market’s current valuation.

Pedro Ortiz shares a similar perspective but emphasizes CPKC’s operational execution, merger synergies, and network integration across Canada, the U.S., and Mexico as key drivers of long-term value. . As per our database, 54 hedge fund portfolios held CP at the end of the third quarter which was 60 in the previous quarter. While we acknowledge the risk and potential of CP as an investment, our conviction lies in the belief that some AI stocks hold greater promise for delivering higher returns and doing so within a shorter time frame. If you are looking for an AI stock that is more promising than CP and that has 10,000% upside potential, check out our report about this

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Microsoft Stock Testing 2 Key Levels as Options Traders Pounce

Elon Musk's xAI to repay $3 billion debt early, Bloomberg News reports

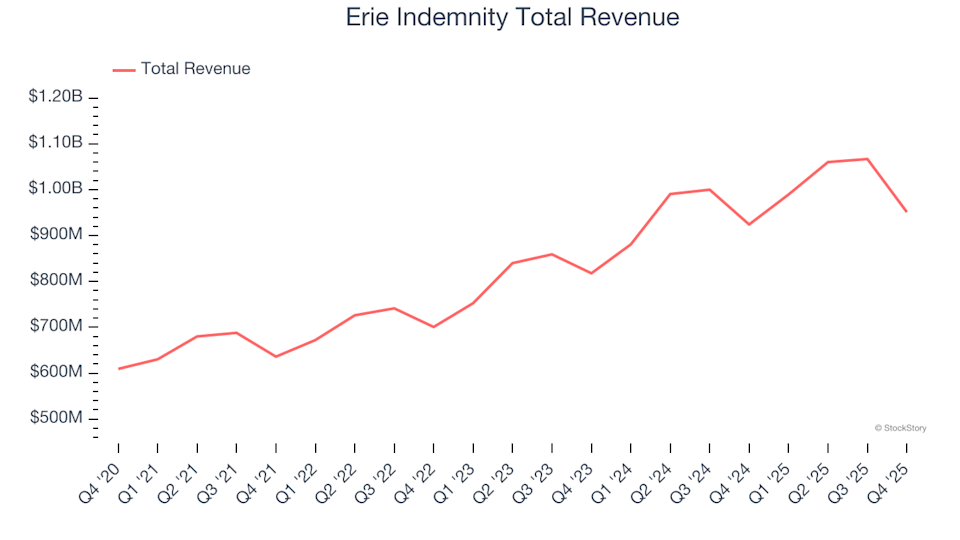

Q4 Summary: Erie Indemnity (NASDAQ:ERIE) Compared to Other Property and Casualty Insurance Shares

Top 10 Crypto Assets In Accumulation Zone: RENDER and BONK Lead the List