Sunstone Hotel Investors, Inc. (SHO): A Bull Case Theory

We came across a bullish thesis on Sunstone Hotel Investors, Inc. on Canadian Cashflow’s Substack. In this article, we will summarize the bulls’ thesis on SHO. Sunstone Hotel Investors, Inc.'s share was trading at $9.22 as of February 13th. SHO’s trailing and forward P/E were 461.00 and 175.44, respectively according to Yahoo Finance.

Sunstone Hotel Investors, Inc. represents a capital-structure mispricing opportunity centered on its preferred shares rather than the common equity. The company owns a concentrated portfolio of 14 upper-upscale and luxury hotels totaling roughly 7,000 rooms, diversified across resort, convention, and urban assets in key U.S. markets including San Diego, Maui, Miami, San Francisco, Washington, D.C., and Boston.

Many properties operate under strong global brands such as Marriott, Hilton, Hyatt, and Andaz, supporting resilient demand through loyalty ecosystems and high-quality management. Several major renovations and brand conversions, including the reopening of Andaz Miami Beach, are still ramping up, creating embedded EBITDA growth even before considering any corporate action.

The core thesis centers on the preferred shares, which offer a low-7% cash yield while sitting senior to common equity and supported by a substantial equity cushion, with over 60% of the capital stack represented by common equity at current prices. Sunstone’s leverage remains modest relative to peers, limiting downside risk. Activist pressure from Tarsadia and improved asset stabilization increase the plausibility of a sale, and in a typical take-private scenario, preferred shares would likely be redeemed at par, implying roughly 20–25% upside.

Meanwhile, the common trades at a high-single-digit FFO yield and at a discount to NAV, reflecting temporarily depressed earnings from renovations rather than structural weakness. Overall, the preferred shares offer a paid-to-wait structure with asymmetric upside tied to corporate action and limited downside supported by asset quality and balance sheet strength.

Previously, we covered a

Sunstone Hotel Investors, Inc. is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

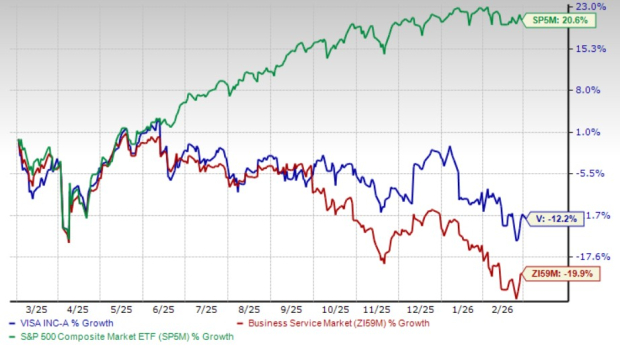

Why Visa's Prisma and Newpay Deals Come at a Critical Moment

Is Palomar (PLMR) a Solid Growth Stock? 3 Reasons to Think "Yes"

Fabrinet Eyes 800ZR and Co-Packaged Optics as Growth Catalysts

Stantec (STN) is an Incredible Growth Stock: 3 Reasons Why