Canadian Natural Resources Limited (CNQ): A Bull Case Theory

We came across a bullish thesis on Canadian Natural Resources Limited on Focused Investing’s Substack. In this article, we will summarize the bulls’ thesis on CNQ. Canadian Natural Resources Limited's share was trading at $40.59 as of February 17th. CNQ’s trailing and forward P/E were 17.43 and 20.08 respectively according to Yahoo Finance.

Canadian Natural Resources Limited (CNQ) has declined alongside other Canadian producers amid market concerns about potential Venezuelan supply, but the company’s long-standing financial model and operational trajectory remain intact. Its strategy is straightforward: cash from operations funds sustaining and growth capex, acquisitions are typically debt-financed, and free cash flow is allocated to dividends, share repurchases, and debt reduction while maintaining a strong investment-grade balance sheet, currently rated BBB+ by Fitch Ratings and Moody's Investors Service.

Over recent years, CNQ materially reduced debt during the 2022 oil price surge while growing production and repurchasing shares, before temporarily increasing leverage in 2024 to acquire assets from Chevron Corporation, which boosted output. Management has since resumed deleveraging toward a sub-$12 billion target, although lower oil prices slow—rather than derail—this process. Operationally, CNQ benefits from diversified production across oil sands, conventional crude, and natural gas, with oil sands providing stable, non-declining output and an overall corporate decline rate near 12%.

Cash flow generation remains robust, with operating cash generally covering dividends and capex and, in stronger periods, buybacks and debt paydown. Dividend safety appears solid, with payout ratios around 30% of cash from operations and 60% of free cash flow. At roughly 6× cash flow and 11× free cash flow, valuation appears reasonable rather than deeply mispriced, especially considering steady long-term production growth.

Notably, production has risen significantly over four years while the stock has remained flat, suggesting potential upside over time. The primary investment appeal lies in reliable yield and above-average dividend growth potential, making CNQ attractive for income-focused investors when entry yield thresholds are met and portfolio balance permits.

Previously, we covered a

Canadian Natural Resources Limited is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

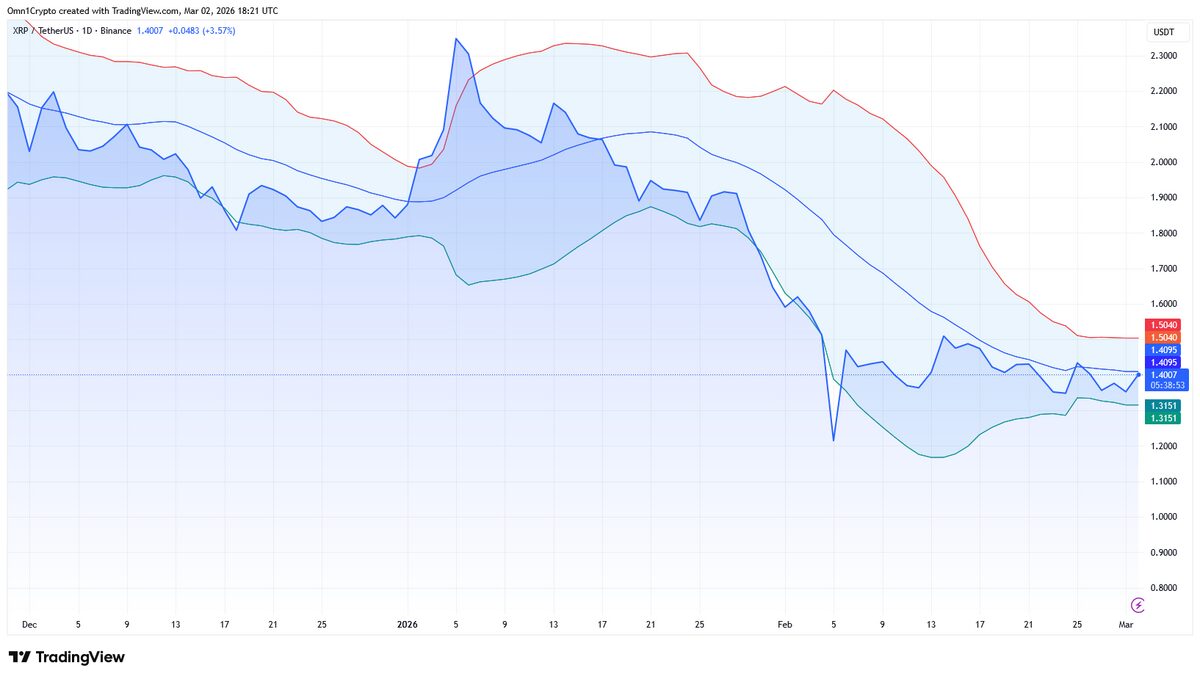

Is XRP Facing The Most Price Turbulence This Week?