Biohaven Ltd. (BHVN): A Bull Case Theory

We came across a bullish thesis on Biohaven Ltd. on Danny’s Substack by Danny Green. In this article, we will summarize the bulls’ thesis on BHVN. Biohaven Ltd.'s share was trading at $11.54 as of February 18th.

Biohaven Ltd. is a clinical-stage biotechnology company targeting large global markets with significant unmet needs across neurology, immunology, and oncology, with lead programs such as its Kv7 activator franchise representing potential blockbuster opportunities that could justify a multi-fold increase from its roughly $1.4 billion market capitalization if even one or two Phase 3 trials succeed.

The company’s long-term vision is to evolve into a multi-franchise, platform-driven biopharma powered by proprietary technologies, including MoDE protein degraders and ion-channel modulators, where a single late-stage success could validate the broader platform and create a durable innovation engine. Its competitive advantage stems from proven execution, highlighted by the development and monetization of Nurtec ODT through a major transaction with Pfizer, and a deep, diversified pipeline that provides multiple shots on goal despite inherent clinical risk.

However, fragmentation across therapeutic areas, early-stage platform assets, and the recent Complete Response Letter setback have pressured investor confidence and contributed to volatility. Leadership under CEO Vlad Coric emphasizes entrepreneurial urgency and capital discipline, including a 60% reduction in R&D spend to extend runway, while financing strength has been reinforced by a $600 million non-dilutive agreement with Oberland Capital alongside equity raises that introduce dilution risk.

Financially, the company remains loss-making with negative free cash flow, typical for high-growth biotech, meaning returns hinge on clinical milestones that can dramatically re-rate valuation or destroy capital if trials fail. A potential five-fold valuation to about $7 billion could emerge from concurrent successes across its Kv7, ADC, and degrader platforms, though the market currently discounts this scenario due to execution risk, pipeline uncertainty, and post-asset-sale skepticism, creating a high-volatility but asymmetric long-term opportunity.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

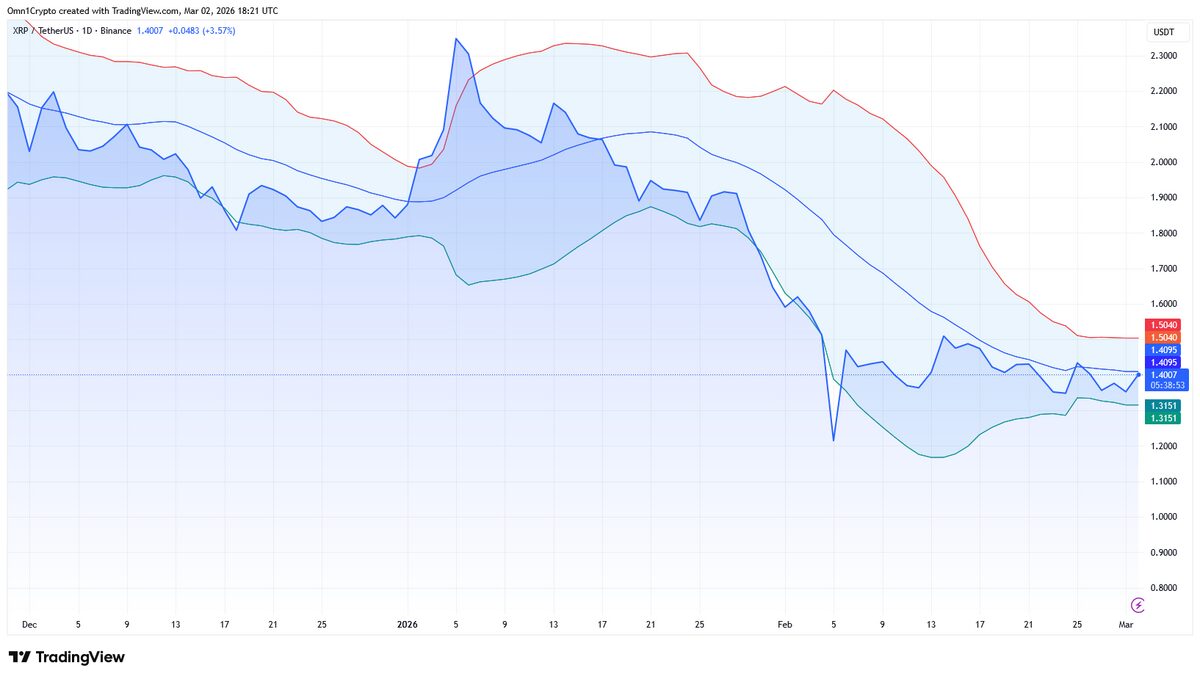

Is XRP Facing The Most Price Turbulence This Week?