IonQ's Earnings: The Expectation Gap on Profitability

The market's reaction to IonQ's report was a classic case of expectation arbitrage. The revenue beat was massive, but the stock's surge was less about the beat itself and more about what was already priced in versus what was a surprise.

The initial gap was enormous. For the fourth quarter, IonQIONQ-6.14% reported revenue of $61.9 million, which beat the midpoint of its own guidance by a staggering 55%. That's a textbook beat. Yet, the stock's 19% surge on the news suggests the market had already baked in this strong performance. The real shock came from the widening losses. While the revenue beat cleared analyst expectations, the company's adjusted net loss widened to $0.20 per share, and its adjusted EBITDA turned redder, from negative $105.7 million to negative $186.8 million for the year. This acceleration in losses was the unexpected element that the market hadn't fully discounted.

Viewed another way, the stock's pop was a "buy the rumor, sell the news" dynamic. The rumor was the hyper-growth narrative, which was already being priced in given the stock's premium valuation. The news was the confirmation of that growth, but also the stark reality of the burn rate. The market's reaction-climbing over $40-indicates that investors were willing to overlook the widening losses for now, betting that the massive revenue acceleration justifies the cash burn. The real test will be whether the company can eventually narrow that gap.

This growth is accelerating at an unprecedented pace. Full-year 2025 revenue of $130 million represented a 202% year-over-year increase, a significant acceleration from prior years. Management's raised outlook for 2026, targeting $225 million to $245 million, implies another nearly doubling of revenue. The expectation gap here is between the market's prior consensus and this new, aggressive forecast. The stock's move higher shows the market is buying into this hyper-growth trajectory, even as it grapples with the financial reality of funding it.

The Guidance Reset: Closing the Profitability Gap

Management's 2026 outlook is a clear reset of market expectations. The company guided for revenue of $225 million to $245 million, a massive leap that implies another doubling of sales. Yet, the accompanying profit forecast is the real pivot. IonQ expects adjusted EBITDA of -$310 million to -$330 million for the year. That's a significant widening from the full-year 2025 loss of -$186.8 million, signaling that the path to profitability is being pushed further out.

This is a classic guidance reset. The market had already priced in hyper-growth, but the new numbers explicitly state that heavy R&D investment will continue unabated. The guidance implies the consensus on profitability is being reset to a longer runway. The expectation gap here is between the aggressive revenue trajectory and the financial reality of funding it. The company is prioritizing technological milestones-like targeting an operational 256-qubit machine by the end of 2026-over near-term margin expansion. This is a bet that today's heavy losses will be justified by future market dominance.

| Total Trade | 5 |

| Winning Trades | 3 |

| Losing Trades | 2 |

| Win Rate | 60% |

| Average Hold Days | 2 |

| Max Consecutive Losses | 1 |

| Profit Loss Ratio | 2.45 |

| Avg Win Return | 19.09% |

| Avg Loss Return | 7.71% |

| Max Single Return | 23.92% |

| Max Single Loss Return | 9.03% |

The company's massive cash position provides the runway for this strategy. IonQ closed 2025 with about $3.3 billion in cash and investments. That war chest, combined with a record $370 million in remaining performance obligations, gives it significant financial flexibility. Yet, it also underscores that the current business model is not yet cash-flow positive. The guidance confirms that the burn rate will accelerate, turning the focus from quarterly profitability to the successful execution of a multi-year technology roadmap. For investors, the question shifts from "Can they grow?" to "How long can they fund this growth before hitting a wall?" The guidance reset answers the first part with a resounding yes, while the second part remains open.

Strategic Moves to Bridge the Gap

IonQ's strategy is a direct attempt to close the expectation gap between its soaring revenue and widening losses. The company is betting that technological superiority and vertical integration will eventually justify today's heavy burn. Its claims of a 99.99% two-qubit gate fidelity and speed advantages of 1,000–10,000x over leading superconducting systems are meant to establish a moat, proving that its current investment is building a future monopoly. The roadmap, targeting an operational 256-qubit machine by late 2026, is a concrete signal that the company is executing on this promise. For investors, this is the "buy the rumor" part of the story: the market is being asked to believe that these technical milestones will one day translate into a dominant, profitable business.

The planned acquisition of SkyWater is the operational arm of this strategy. By securing manufacturing and supply-chain control, IonQ aims to de-risk its path to scaling. This move directly addresses the challenge of meeting demand, which already exceeds supply. The company's $370 million backlog of orders provides a critical near-term revenue anchor, validating the market pull for its systems. The SkyWater deal is a bid to convert that demand into predictable, lower-cost production, which is essential for eventually closing the profitability gap.

Yet, a major hurdle remains. Even with a semiconductor-based roadmap, the bill of materials cost for full fault-tolerant machines is still a key variable. While management suggests it will remain under $30 million, that figure is a target, not a guarantee. Until IonQ can demonstrate a clear, scalable path to bringing these costs down, the expectation gap persists. The company is trading today's massive cash burn for tomorrow's potential market share, but the timeline for that payoff is uncertain. The strategic moves are ambitious and well-aligned with the long-term narrative, but they are also the very investments that are widening the losses in the near term.

Catalysts and Risks: Execution vs. Expectations

The stock's momentum hinges on a narrow path: executing on today's orders while funding tomorrow's technology. The near-term catalyst is clear. IonQ must convert its $370 million backlog of remaining performance obligations into revenue without further compressing margins. This is the bridge between the current premium valuation and future cash flow. The company's guidance for 2026 revenue of $225 million to $245 million implies it needs to book and deliver on a significant portion of that RPO this year. Any stumble in order fulfillment or a shift to lower-margin contracts could quickly reset expectations downward.

The major risk is the continued widening of losses, which threatens the stock's premium multiple. With an enterprise value of $9.78 billion, the market is pricing in a long, successful growth runway. Yet the company expects adjusted EBITDA of -$310 million to -$330 million for 2026, a deepening of the burn. If growth slows even slightly from the guided 73%-88% expansion, or if R&D costs spike unexpectedly, the expectation gap between the soaring revenue and the accelerating losses could reopen. The stock's valuation is a bet on flawless execution; any sign of friction could force a re-rating.

Watch for progress on two key milestones as signals of commercial scalability. First is the target for an operational 256-qubit machine by the end of 2026. This is a critical technical benchmark that validates the heavy investment in R&D. Success here would reinforce the narrative of technological leadership, while a delay would be a major red flag. Second is the timeline for the planned acquisition of SkyWater. Closing this deal is meant to secure manufacturing control and de-risk scaling. Its progress will be a key indicator of whether IonQ can move from selling systems to building them efficiently, a crucial step toward closing the profitability gap.

The bottom line is that the stock is now a pure play on execution. The revenue beat and raised guidance have reset the growth narrative. The coming quarters will test whether IonQ can walk that tightrope-delivering on its massive order book while funding the technological leap that justifies its price. Any misstep on either front could turn the current momentum into a painful reality check.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

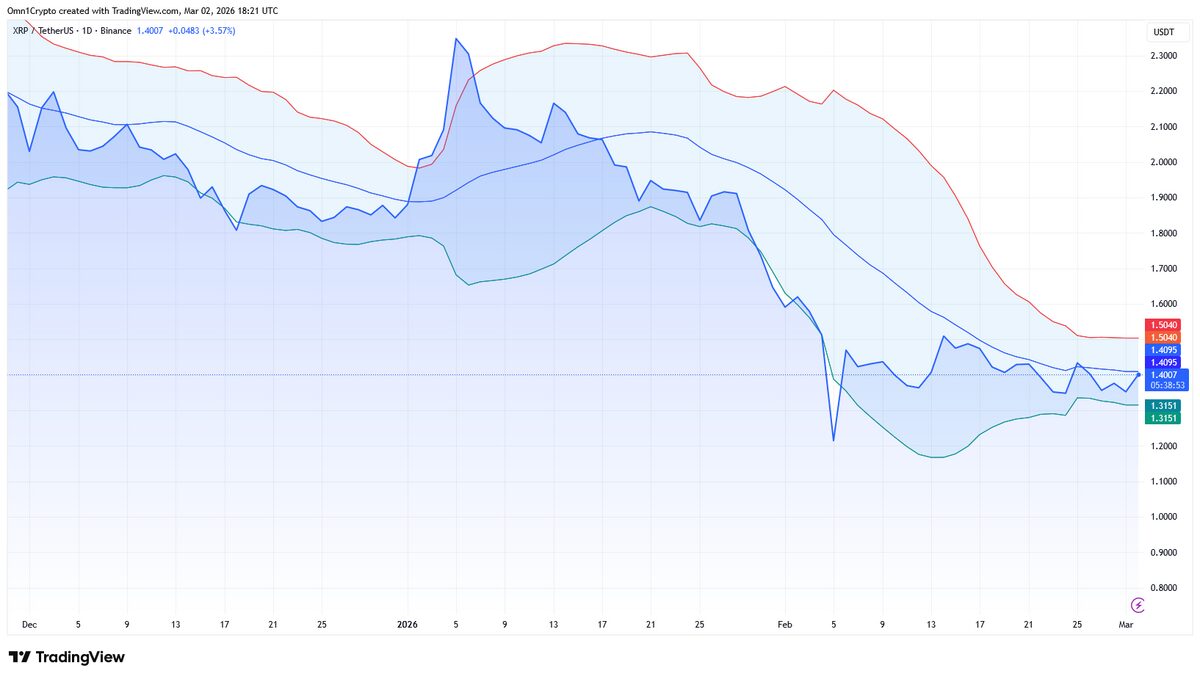

Is XRP Facing The Most Price Turbulence This Week?