Nordson Corporation (NDSN): A Bull Case Theory

We came across a thesis on Nordson Corporation on Danny’s Substack by Danny Green. In this article, we will summarize the bulls’ thesis on NDSN. Nordson Corporation's share was trading at $299.29 as of February 18th. NDSN’s trailing and forward P/E were 35.04 and 26.53 respectively according to Yahoo Finance.

Nordson Corporation (NDSN) represents a high-quality industrial compounder with cyclical exposure, currently positioned for a constructive inflection as macro conditions stabilize. The company operates across diversified end markets including Industrial Precision, Medical & Fluid Solutions, and Advanced Technology, reducing reliance on any single sector while maintaining exposure to industrial capex cycles.

Although recent organic sales have been flat to modestly negative in pockets such as polymer processing and advanced systems, management’s fiscal 2026 outlook assumes improving customer demand, signaling confidence that macro softness is bottoming. Nordson delivered record fiscal 2025 revenue of $2.8 billion and EBITDA of $900 million, with adjusted EPS rising approximately 5% year over year, while Q3 revenue grew 12% year over year and free cash flow conversion remained exceptionally strong. Backlog entering fiscal 2026 stands near $600 million, providing revenue visibility despite modest Q4 organic softness.

The company’s durable moat stems from technological expertise, entrenched customer relationships, recurring industrial spend, and a strong margin profile of roughly 32–34% EBITDA margins. Capital allocation remains disciplined, with free cash flow supporting dividends, share repurchases, and selective acquisitions under structured frameworks such as NBS Next and Ascend.

While exposure to FX and cyclical capex creates volatility risk, strong cash generation and backlog conversion provide downside support. If sequential organic growth reaccelerates in Industrial Precision and Advanced Technology, multiple expansion is likely. With moderate growth expectations embedded in valuation and robust cash flow underpinning earnings, Nordson offers an attractive risk/reward skew for investors anticipating a cyclical recovery.

Previously, we covered a

Nordson Corporation is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

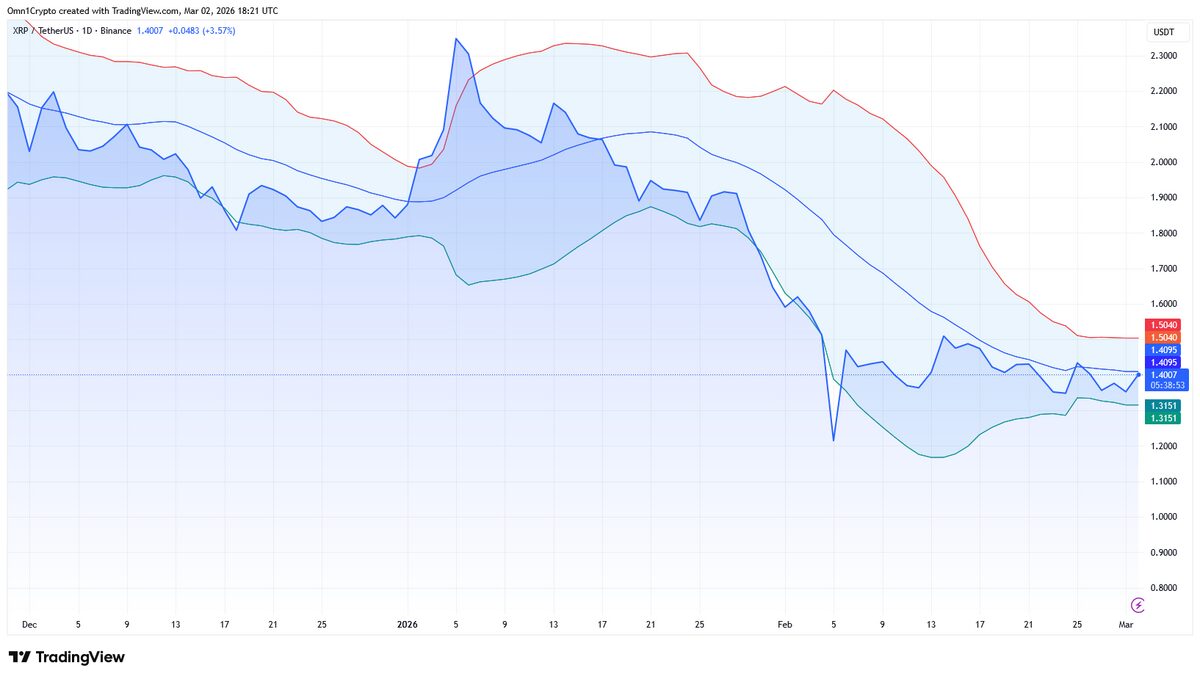

Is XRP Facing The Most Price Turbulence This Week?