Kenvue Inc. (KVUE): A Bull Case Theory

We came across a bullish thesis on Kenvue Inc. on Danny’s Substack by Danny Green. In this article, we will summarize the bulls’ thesis on KVUE. Kenvue Inc.'s share was trading at $18.66 as of February 19th. KVUE’s trailing and forward P/E were 24.93 and 17.01, respectively according to Yahoo Finance.

Kenvue, the newly independent consumer health company spun out from Johnson & Johnson, operates a portfolio of category-leading brands such as Tylenol, Neutrogena, and Listerine, giving it moderate but meaningful competitive advantages. These brands command pricing power and retailer shelf-space, supported by global scale and distribution that reduce vulnerability versus regional players.

While brand equity underpins a moat, the consumer health space is not structurally high-moat—competition from generics, private labels, and shifting consumer trends, along with pressure from e-commerce and brick-and-mortar retail, can erode advantages over time. The business is straightforward, offering well-understood products across baby care, skin care, pain relief, and oral care, with revenues closely linked to consumer demand and macroeconomic trends. Kenvue has delivered mid-single-digit organic growth and maintained gross margins above 50%, though post-spin standalone costs and higher SG&A have pressured near-term margins.

Capital deployment focuses on sustaining brand relevance through marketing, innovation, and digital/e-commerce expansion, though transitional costs temporarily weigh on free cash flow. Returns are moderate to strong, benefiting from scale and pricing power, while growth is repeatable, supported by global consumer health trends and emerging market expansion, albeit sensitive to macro swings and competitive pressures.

Cash generation remains solid, reflecting stable consumer demand and effective working capital management, though early stand-alone infrastructure investments temper free cash flow. Management brings experienced consumer brand leadership and a shareholder-focused approach, navigating the post-spin transition while building long-term capabilities in marketing, global reach, and brand stewardship. Overall, Kenvue represents a reasonably valued, moderately durable consumer health business with established brands, steady cash flows, repeatable growth, and clear opportunities for margin and shareholder value expansion as it navigates its early independent years.

Kenvue Inc. is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

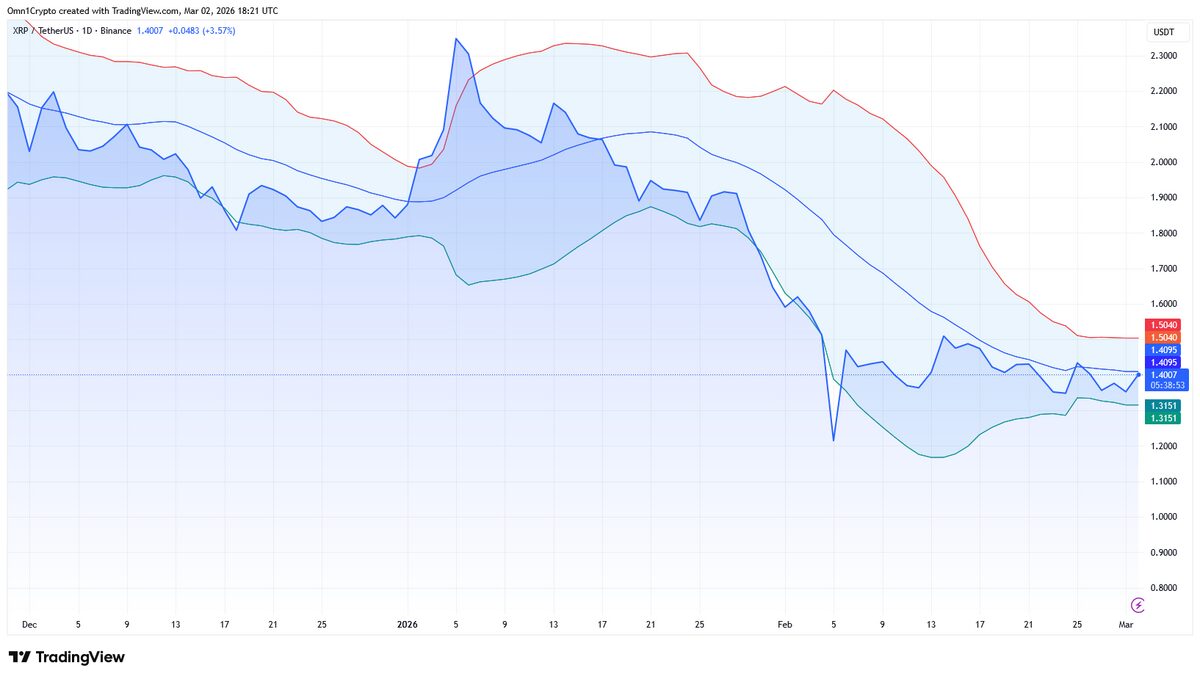

Is XRP Facing The Most Price Turbulence This Week?