GeneDx Holdings Corp. (WGS): A Bull Case Theory

We came across a thesis on GeneDx Holdings Corp. on Danny’s Substack by Danny Green. In this article, we will summarize the bulls’ thesis on WGS. GeneDx Holdings Corp.'s share was trading at $92.04 as of February 18th. WGS’s trailing and forward P/E were 819.55 and 77.52 respectively according to Yahoo Finance.

GeneDx is emerging as a high-growth genomics diagnostics company with a differentiated clinical dataset and proprietary interpretation IP that supports strong diagnostic yield, particularly in rare-disease exome and genome testing. The business benefits from structural resilience, as healthcare spending is large and relatively insulated from broader economic cycles, while regulatory tailwinds—most recently the FDA’s Breakthrough Device designation for ExomeDx™ and GenomeDx™ tests—accelerate payer engagement and adoption.

Q3 2025 results underscore strong fundamentals, with revenue of $116.7 million, roughly 65% year-over-year growth in exome/genome test revenue, and adjusted net income of ~$14.7 million, reflecting several consecutive quarters of improving profitability and operating leverage. GeneDx conducted ~25,700 exome/genome tests in Q3, contributing to 41% of total testing volumes year-to-date, highlighting unit-scale as the primary revenue driver. Management has raised full-year guidance, signaling confidence in continued growth, margin expansion (~74% gross margin in Q3), and disciplined capital allocation in the lab’s operationally intensive scaling process.

While competitive pressures exist from large integrated diagnostics and platform players, the proprietary variant database and clinical curation provide a moderately durable moat that strengthens payer discussions. Key near-term risks include reimbursement delays, lab capacity constraints, and operational disruptions, all of which could materially impact volume-driven revenue. Catalysts include broader commercial payer coverage, accelerating exome/genome volumes, continued adjusted profitability, positive real-world evidence publications, and FDA engagement.

Given current growth and improving margins, GeneDx offers favorable asymmetric upside if reimbursement and scale continue, while a conservative portfolio allocation (0.5–1%) allows monitored exposure, with upside conviction (1–3%) contingent on careful tracking of payer developments, test volumes, and operational execution. Overall, the company represents a compelling, policy- and regulation-driven growth story in genomics diagnostics.

Previously, we covered a

GeneDx Holdings Corp. is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

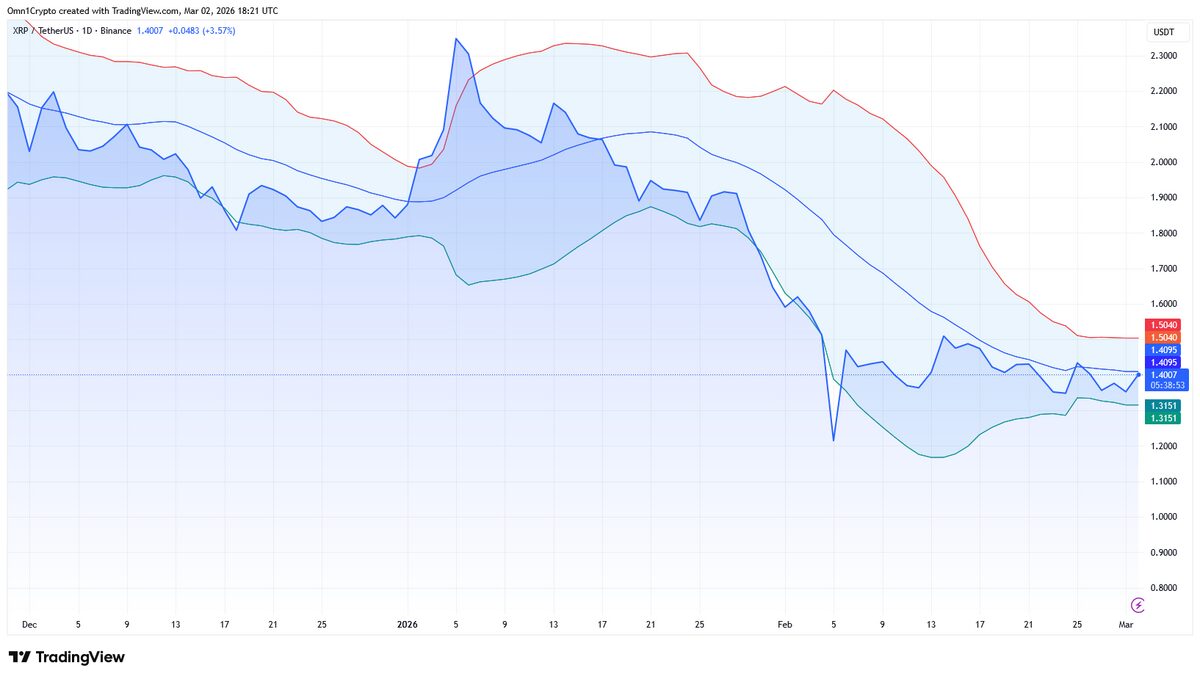

Is XRP Facing The Most Price Turbulence This Week?