Rowe Price Group, Inc. (TROW): A Bull Case Theory

We came across a bullish thesis on T. Rowe Price Group, Inc. on CompoundingLab’s Substack. In this article, we will summarize the bulls’ thesis on TROW. T. Rowe Price Group, Inc.'s share was trading at $94.36 as of February 19th. TROW’s trailing and forward P/E were 10.15 and 9.23 respectively according to Yahoo Finance.

Rowe Price Group, Inc. is a publicly owned investment manager. The firm provides its services to individuals, institutional investors, retirement plans, financial intermediaries, and institutions.TROW is trading as if it were a structurally declining asset manager, but the underlying financials suggest a high-quality franchise being priced with excessive pessimism. Persistent underperformance versus the S&P 500, ongoing active-fund outflows, and negative sentiment around fee pressure have driven the narrative that the business is deteriorating, yet the core economics remain robust.

The firm continues to generate double-digit returns on capital, with a roughly 10-year median ROIC near 19%, placing it among elite financial franchises rather than distressed ones. Its balance sheet is exceptionally strong, with essentially zero leverage, eliminating refinancing risk and providing resilience in cyclical market downturns. Current valuation implies skepticism that appears disconnected from earnings power: an earnings yield around 8% reflects strong operating margins, high capital efficiency, and limited reinvestment needs, yet the stock trades near 10× earnings despite fundamentals that support closer to 15× based on ROIC and modest long-term growth assumptions.

Growth itself has been steady rather than spectacular, with historical revenue expansion around 6% and forward expectations near 4%, consistent with industry asset growth. Importantly, T. Rowe maintains meaningful market share in active mutual funds and retirement channels, supported by brand strength, distribution relationships, and long performance records that create a narrow but durable moat.

Operating margins near 41% further reinforce that the business retains pricing power and scale advantages. While drawdowns have historically tracked market cycles, recoveries have followed as flows stabilize. Using intrinsic value estimates around $107 per share versus a roughly $95 price suggests a modest discount, highlighting a quality compounder priced like a melting ice cube, which creates the central investment opportunity.

Previously, we covered a

Rowe Price Group, Inc.isnot on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

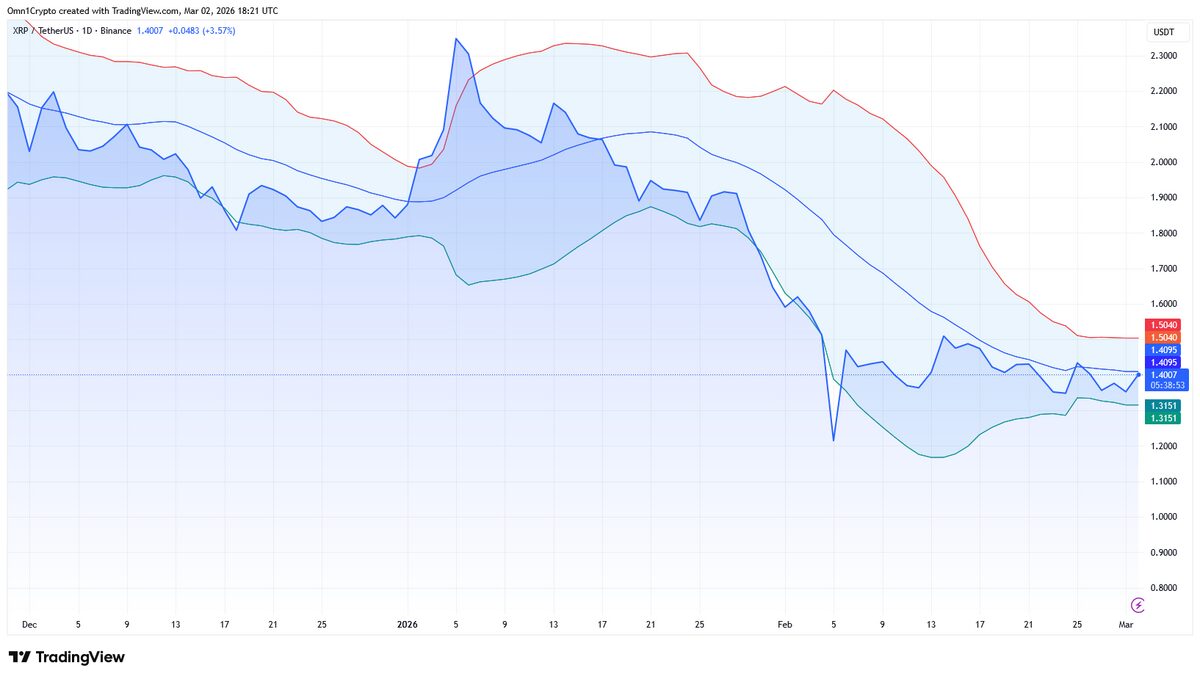

Is XRP Facing The Most Price Turbulence This Week?