Crown Holdings, Inc. (CCK): A Bull Case Theory

We came across a bullish thesis on Crown Holdings, Inc. on Canadian Cashflow’s Substack. In this article, we will summarize the bulls’ thesis on CCK. Crown Holdings, Inc.'s share was trading at $115.10 as of February 23rd. CCK’s trailing and forward P/E were 20.41 and 12.20 respectively according to Yahoo Finance.

Crown Holdings, Inc. operates largely behind the scenes, manufacturing aluminum beverage cans, aerosol containers, and food packaging that consumers interact with daily without recognizing the supplier. The company’s importance stems from its deep integration into global supply chains, serving major beverage and consumer goods companies that depend on consistent, compliant, and large-scale production. Once embedded, these relationships are difficult to displace because customers prioritize reliability over marginal cost savings, creating durable demand that has persisted for decades.

Although packaging may appear commoditized, Crown benefits from meaningful competitive advantages, including long-term partnerships with global brands such as The Coca-Cola Company and PepsiCo, significant scale that would require billions for competitors to replicate, and contractual cost pass-through mechanisms that protect margins from aluminum price volatility. Demand is also resilient, supported by steady beverage consumption across economic cycles and diversification into energy drinks, alcohol, and canned food products.

Management appears conservative and execution-focused, with a track record of cautious guidance and shareholder-friendly capital allocation. Recent actions include raising 2025 EPS guidance by 12% and free cash flow expectations by 25% to roughly $1 billion, alongside $400 million returned to shareholders through buybacks and dividends while maintaining moderate leverage near 2.5× EBITDA.

Financially, Crown demonstrates improving cash generation, with free cash flow rising from negative levels in 2022 to $789 million in 2024, or approximately $6.66 per share, supported by normalized capital spending and operational recovery. At a share price near $105, this implies a roughly 6.4% free cash flow yield, positioning the company as a mature, cash-generative industrial investment capable of delivering returns through steady growth and capital returns rather than multiple expansion.

Overall, Crown represents a durable, essential business that offers stability and diversification relative to high-growth technology stocks, with achievable growth requirements and long-term compounding potential.

Previously, we covered a

Crown Holdings, Inc. is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

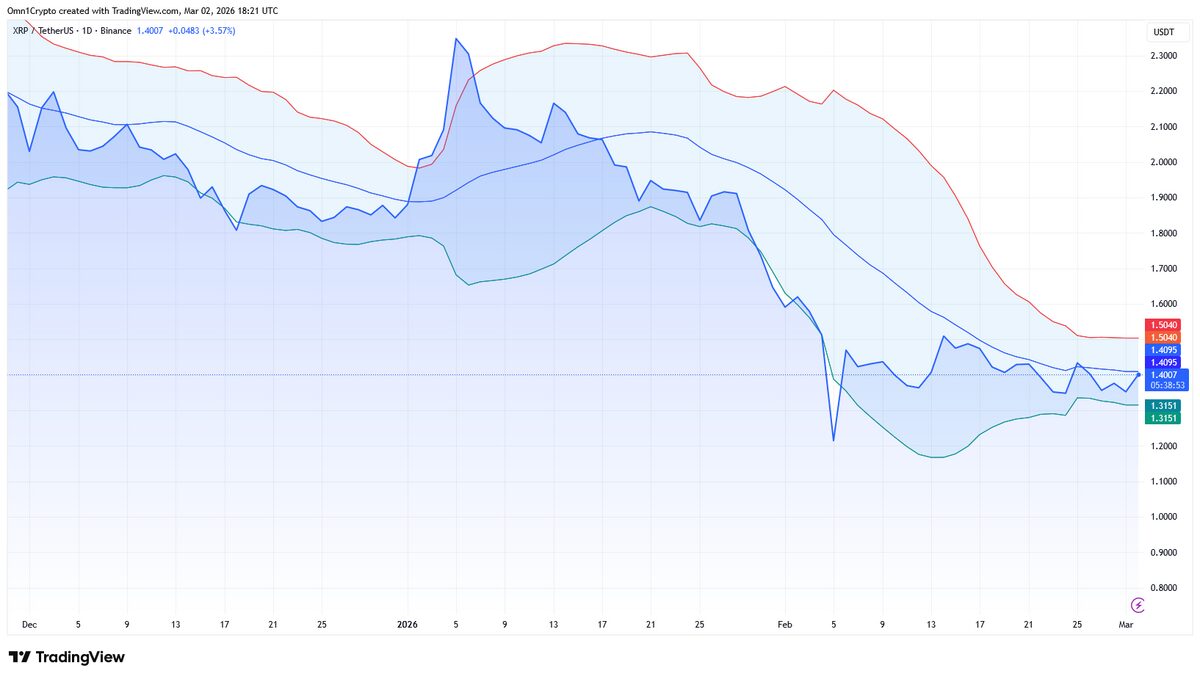

Is XRP Facing The Most Price Turbulence This Week?