VNET Group, Inc. (VNET): A Bull Case Theory

We came across a bullish thesis on VNET Group, Inc. on Agon Investments’s Substack. In this article, we will summarize the bulls’ thesis on VNET. VNET Group, Inc.'s share was trading at $11.85 as of February 20th. VNET’s forward P/E was 25.64 according to Yahoo Finance.

VNET Group, Inc. sits at the center of China’s AI infrastructure supercycle, providing hosting and related services to Internet companies, government entities, and enterprises through a large portfolio of carrier-neutral, cloud-neutral data centers across the country. The company is strategically positioned to capture outsized demand from Chinese hyperscalers, including ByteDance, Alibaba Cloud, and Tencent, as AI-related investment in China is projected to reach RMB 700 billion in 2025, up 48% year-over-year, with 57% funded through government mechanisms.

VNET’s multi-phase developments, pre-acquired land bank, and rapid 9–12 month delivery timeline versus the 14–18 month industry norm provide a structural advantage, enabling hyperscalers to operationalize GPU clusters faster and more cost-effectively. Its presence in key national computing hubs such as Inner Mongolia, Hebei, and the Yangtze River Delta offers 25–30% structural cost advantages in electricity, land, and permitting, while carrier-neutral architecture reduces latency and transport expenses.

Operational execution has been strong, with capacity expanding from 486 MW to 783 MW in nine months, mature facilities at 95% utilization, and under-construction capacity pre-committed at 98.7%, mitigating speculative build risk. Strategic partnerships, including Shandong Hi-Speed for renewable energy integration, provide margin stability and energy cost savings. Upside catalysts include accelerated ByteDance deployments potentially pulling forward RMB 400–600 million in revenue, wholesale revenue mix expansion driving 300+ basis points in EBITDA margin growth, and the potential for further hyperscaler contracts.

Key risks include customer concentration, macro policy uncertainty, and management execution, particularly following recent Blackstone-related corporate governance changes. Despite these risks, VNET offers asymmetric upside, with a conservative target price of $17.3 per share reflecting strong growth, durable contracts, and structural cost advantages in China’s AI infrastructure market.

VNET Group, Inc. is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

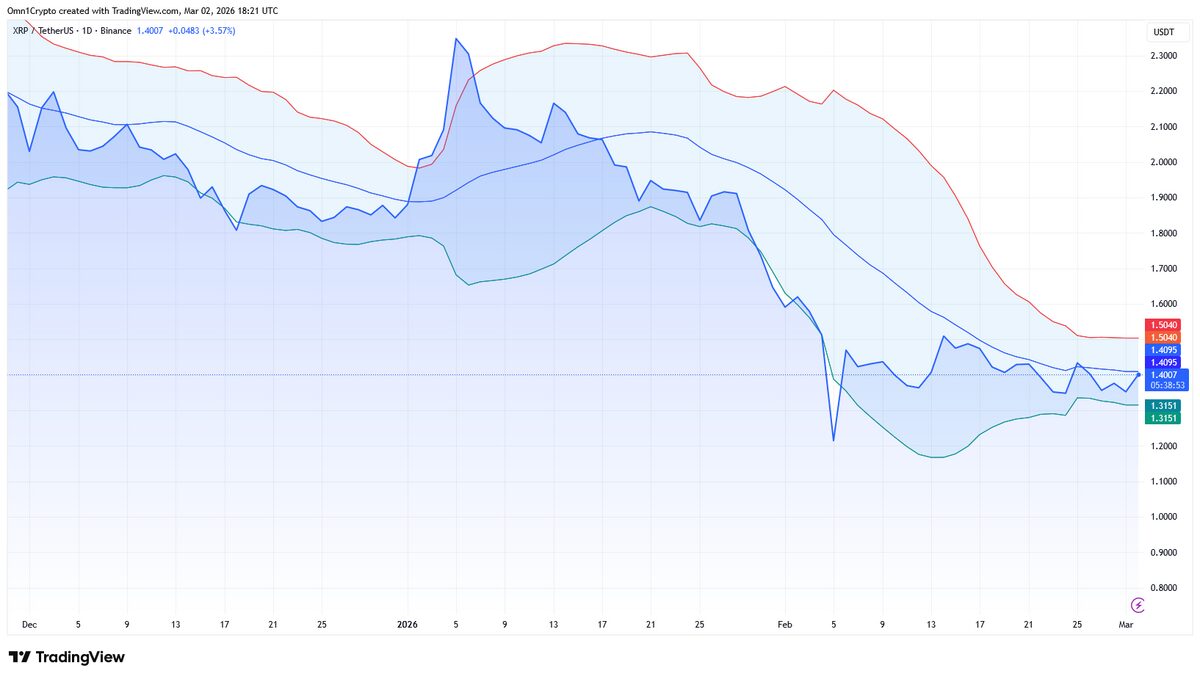

Is XRP Facing The Most Price Turbulence This Week?