Halozyme Therapeutics, Inc. (HALO): A Bull Case Theory

We came across a bullish thesis on Halozyme Therapeutics, Inc. on 24K Research’s Substack. In this article, we will summarize the bulls’ thesis on HALO. Halozyme Therapeutics, Inc.'s share was trading at $70.98 as of February 20th. HALO’s trailing and forward P/E were 16.41 and 8.19, respectively according to Yahoo Finance.

Halozyme Therapeutics Inc (HALO), based in San Diego, California, is a pharmaceutical technology company that has built a high-margin, royalty-driven business by transforming complex IV biologics into simple, rapid subcutaneous injections. Its flagship ENHANZE platform has revolutionized treatments such as DARZALEX SC, Phesgo, and VYVGART Hytrulo, cutting multi-hour cancer and autoimmune therapies down to five-minute or patient-administerable doses.

This proprietary technology provides Halozyme with a durable, annuity-like revenue stream that is insulated from typical biotech R&D risk, while offering substantial earnings visibility. The company’s royalty model, tied to blockbuster drugs across multiple partners, is recurring, high-margin, and expected to potentially double by 2028, with Adjusted EBITDA margins projected to rise from 59–61% in 2024 to 74–75% by 2028, reflecting operational leverage and capital discipline.

Halozyme’s growth is further secured by an extensive ENHANZE pipeline, ongoing IV-to-SC conversions, and strong patent protection, which collectively ensure continued royalty expansion without reliance on speculative drug development. The Hypercon acquisition enhances long-term durability by enabling ultra-concentrated biologics for at-home auto-injectors, extending Halozyme’s intellectual property into the 2040s and positioning it as a critical enabler of decentralized, AI-assisted healthcare. This dual-platform strategy amplifies patient autonomy, improves care efficiency, and aligns Halozyme with the future of personalized biologics.

While risks include patent expiration, litigation, partner concentration, and the eventual 2030–2035 revenue cliff, Halozyme’s predictable, high-margin model, combined with a robust technology moat and disciplined execution, underpins a compelling investment case. With EPS projected to accelerate and royalties expanding, the company is positioned for strong earnings growth, making it a high-quality mid-cap compounder with a $75–$90 price target by 2026.

Halozyme Therapeutics, Inc. is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

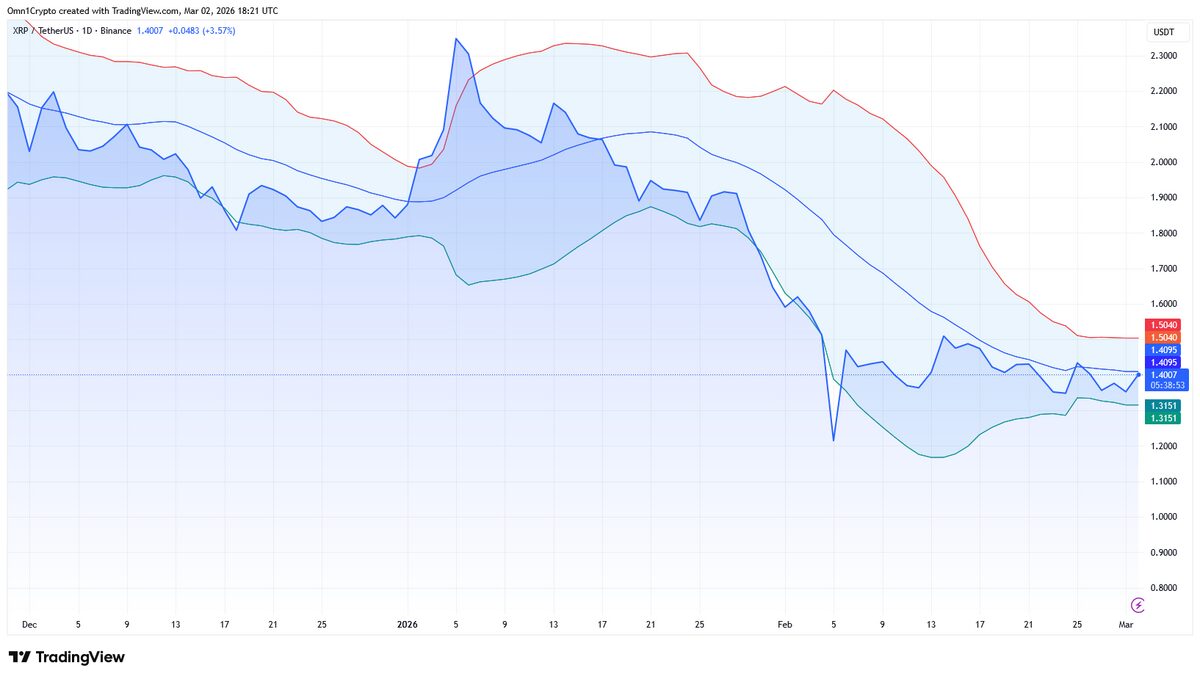

Is XRP Facing The Most Price Turbulence This Week?