Pinterest, Inc. (PINS): A Bull Case Theory

We came across a bullish thesis on Pinterest, Inc. on The Wealth Dynasty Report’s Substack. In this article, we will summarize the bulls’ thesis on PINS. Pinterest, Inc.'s share was trading at $17.77 as of February 20th. PINS’s trailing and forward P/E were 11.56 and 14.79 respectively according to Yahoo Finance.

Pinterest, Inc. operates as a visual search and discovery platform in the United States, Canada, Europe, and internationally. PINS is positioned as a highly liquid, cash-rich digital advertising platform trading at what appears to be a significant valuation discount relative to its fundamentals. The company holds approximately $2.7 billion in liquid assets against just $398 million in current liabilities, resulting in an exceptional 8.8x current ratio and zero long-term debt, which together create a fortress balance sheet rarely seen in the technology sector.

Pinterest operates a visual discovery platform with roughly 553 million monthly active users who actively search for inspiration across categories such as fashion, home décor, and travel, placing them closer to purchase intent than users on traditional social media platforms and making the advertising model particularly attractive to brands. The business remains primarily North America–driven but continues expanding internationally while maintaining a capital-light structure that produces high margins and strong cash generation.

Financial performance reflects steady growth, with revenue rising to $3.65 billion in 2024 and operating cash flow surging to $965 million, translating into approximately $940 million of free cash flow and a 26% margin. Management has reinforced shareholder returns through nearly $1 billion of stock buybacks, supported by $3.1 billion in working capital and substantial net cash per share.

Despite these strengths, the stock trades near 9x earnings, roughly 70% below sector averages, largely due to market concerns around near-term guidance and advertising cyclicality. This disconnect creates a compelling risk-reward profile: downside appears limited by liquidity, profitability, and buybacks, while upside could emerge from revenue reacceleration, margin expansion, continued capital returns, or strategic interest from larger platforms. Overall, Pinterest represents a financially resilient, cash-generative business with meaningful rerating potential if market sentiment normalizes.

Previously, we covered a

Pinterest, Inc. is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

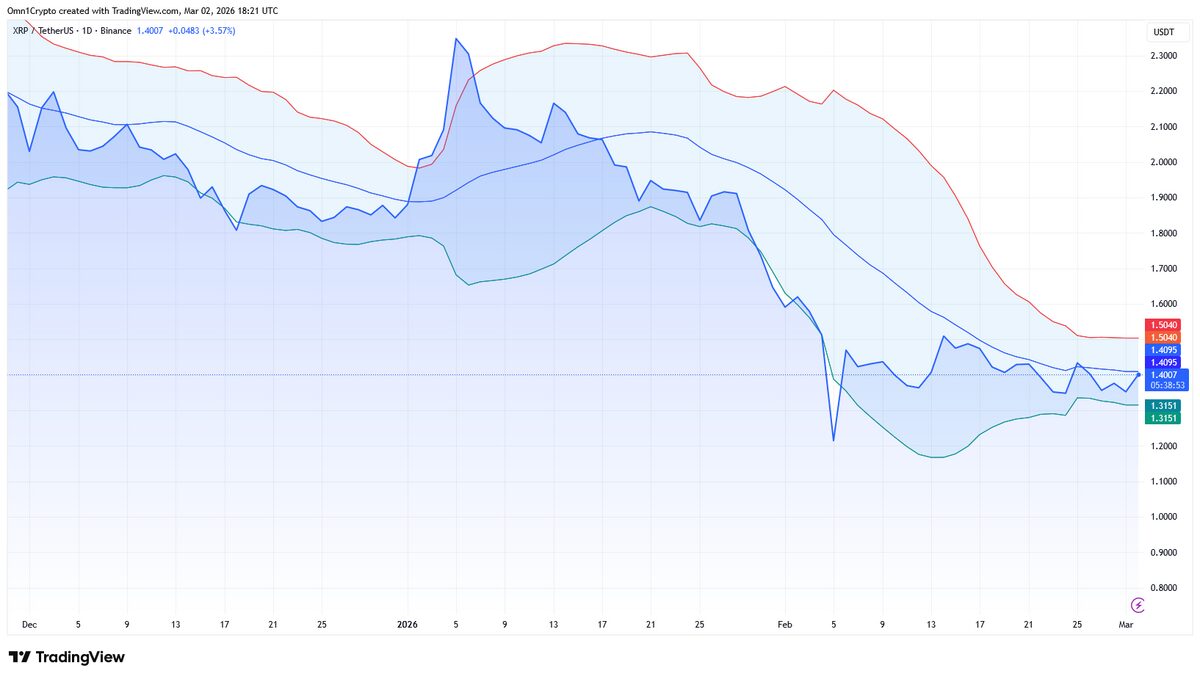

Is XRP Facing The Most Price Turbulence This Week?