Becton, Dickinson and Company (BDX): A Bull Case Theory

We came across a bullish thesis on Becton, Dickinson and Company on X.com by @MoneyShow. In this article, we will summarize the bulls’ thesis on BDX. Becton, Dickinson and Company's share was trading at $176.66 as of February 26th. BDX’s trailing and forward P/E were 35.03 and 12.82, respectively according to Yahoo Finance.

Becton, Dickinson and Company (BDX) remains a steady healthcare leader supported by durable, recurring demand across medical devices and diagnostics, positioning it as an attractive total return opportunity into 2026. The company operates through five segments—Medical Essentials, Connected Care, BioPharma Systems, Interventional, and Life Sciences—providing critical products such as IV catheters, medication delivery systems, pre-fillable drug solutions, and advanced patient monitoring platforms.

With a global footprint spanning the U.S., China, Germany, and other key markets, BDX serves hospitals, laboratories, researchers, and pharmaceutical companies, reinforcing its diversified and resilient revenue base.

Despite this stability, the stock appears discounted relative to historical dividend yield ranges. Based on its current $4.20 dividend, the historically repetitive high dividend (undervalued) yield of 1.6% implies a $255 share price, while shares recently traded near $192, reflecting a 2.1% yield and roughly a 33% discount to that undervalued threshold. On the other end, the historically repetitive low dividend (overvalue) yield of 1.1% suggests a theoretical valuation of $355 per share, representing as much as 90% upside from current levels.

Internally, fundamentals remain sound: ROIC stands at 10%, free cash flow yield at 4%, and P/EBV at 0.9. Economic EPS of $6.45 exceeds reported GAAP EPS of $5.81, and economic book value is $217.66 per share, above the current price. While analysts have highlighted near-term concerns, those risks appear embedded in the stock, whereas cash flow metrics and valuation signals point to mispricing. The recommended action is to buy BDX.

Previously, we covered a

Becton, Dickinson and Company is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Here's Why You Should Retain Honeywell Stock in Your Portfolio

Dycom Gears to Report Q4 Earnings: Here's What to Expect This Season

US tariff lawsuits returned to trade court to determine next steps

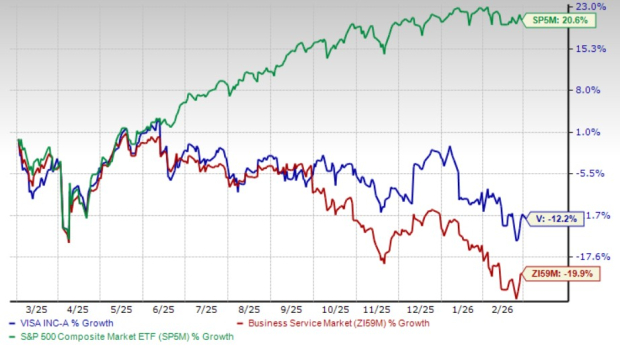

Why Visa's Prisma and Newpay Deals Come at a Critical Moment