Procore Technologies, Inc. (PCOR): A Bull Case Theory

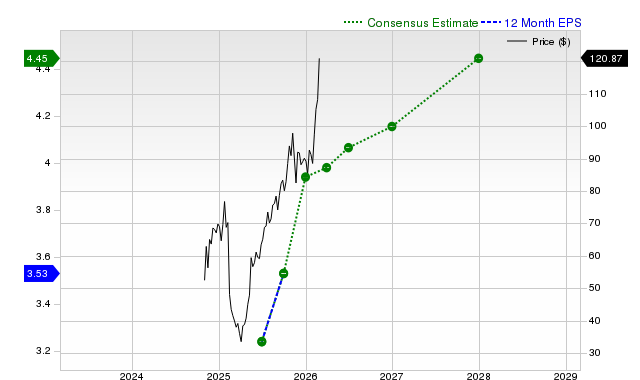

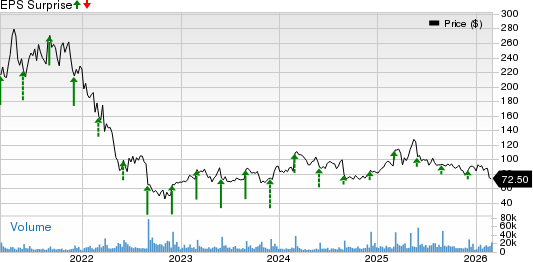

We came across a on Procore Technologies, Inc. on Zenoble’s Substack by Zenoble Research. In this article, we will summarize the bulls’ thesis on PCOR. Procore Technologies, Inc.'s share was trading at $48.86 as of February 23rd. PCOR’s forward P/E was 42.73 according to Yahoo Finance.

Procore Technologies sits at a critical inflection point that investors appear to be mispricing, creating what could be a compelling opportunity with substantial upside through 2027. The company’s valuation has compressed significantly, with its EV/Sales multiple declining from roughly 20x to about 5x despite improving fundamentals, as broader SaaS multiple contraction and higher interest rates have weighed on sentiment toward construction-exposed software companies.

Slowing commercial construction activity, reflected in weak Architecture Billings Index readings, has led the market to assume structurally impaired growth, even though early indicators suggest project demand may be stabilizing. Against this backdrop, Procore is executing a strategic transformation centered on Procore Helix, an AI-powered analytics and workflow engine designed to evolve the platform from a passive system of record into an autonomous construction intelligence layer.

By embedding generative AI, agentic workflows, and proprietary construction data across its ecosystem, Helix aims to automate complex tasks such as RFIs, scheduling risk analysis, and project coordination, positioning Procore as the operating system for construction rather than simply a software vendor. Strategic acquisitions, including Novorender, FlyPaper, and Datagrid, further strengthen this vision by enabling real-time model processing, automated design coordination, and autonomous workflow execution across third-party systems.

Procore’s competitive differentiation lies in its field-first data approach and construction-volume pricing model, which aligns customer growth with platform revenue while increasing switching costs and data capture.

Although consensus forecasts assume modest growth, the thesis anticipates reacceleration beginning in late 2026 as Helix commercialization, macro normalization, and leadership execution drive stronger revenue and margin expansion, potentially leading to multiple re-rating. Even under conservative assumptions, the company offers attractive risk-reward, with significant upside if Helix adoption establishes a durable competitive moat and construction activity recovers.

Procore Technologies, Inc. is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

AECOM Secures Key Role in Seattle's $1B Transit Modernization

Okta Set to Report Q4 Earnings: What's in Store for the Stock?

Earnings Estimates Rising for Everus Construction Group, Inc. (ECG): Will It Gain?