Integra Q4 Results Surpass Projections, Revenue Exceeds Expectations, Margins Decline, Shares Rise

Integra LifeSciences Holdings Corporation Q4 2025 Earnings Overview

Integra LifeSciences Holdings Corporation (IART) reported adjusted earnings per share of $0.83 for the fourth quarter of 2025, surpassing the Zacks Consensus Estimate by 4.7%. However, this figure represents a 14.4% decline compared to the same period last year.

The adjusted results exclude one-time items such as costs related to structural changes, divestitures, acquisitions, integration, and compliance with EU Medical Device Regulation, among others.

On a GAAP basis, the company posted a net loss of $0.02 per share for the quarter, compared to earnings of $0.25 per share in the prior year.

For the full year 2025, adjusted EPS came in at $2.23, reflecting a 12.9% decrease year over year.

Revenue Performance

Fourth-quarter total revenue reached $434.9 million, a 1.7% decrease from the previous year, but slightly ahead of the Zacks Consensus Estimate by 0.1%. Organic revenue dropped 2.5% year over year.

For the entire year, revenue totaled $1.63 billion, up 1.5% from 2024, though organic revenue slipped 0.7% compared to the prior year.

Following the earnings release, IART shares rose 0.4% last Friday.

Segment Highlights

In the Codman Specialty Surgical segment, reported revenue increased by 2.7% year over year (1.6% organic growth), reaching $323.3 million.

- Neurosurgery sales grew 1.4% organically, driven by strong demand for products like CereLink, Mayfield capital, Aurora, and CUSA.

- Instrument sales rose 2.3% organically, keeping pace with the broader market.

- ENT sales advanced 2.2% organically, supported by AERA, TruDi navigated disposables, and MicroFrance instruments.

The Tissue Technologies division generated $111.6 million in revenue for the quarter, marking a 12.8% decline both on a reported and organic basis.

- Wound Reconstruction sales fell 21.4% organically, mainly due to previously announced remediation efforts for MediHoney and a tough comparison for Integra Skin.

- Private Label sales jumped 20.1%, benefiting from stronger partner orders.

Profitability and Margins

Gross profit for the quarter was $220.9 million, down 11.3% year over year. The gross margin narrowed by 549 basis points to 50.8%, reflecting a 10.6% rise in the cost of goods sold.

Selling, general, and administrative expenses declined 5.2% to $169.3 million, while research and development spending dropped 20.6% to $24.8 million.

Adjusted operating profit stood at $26.8 million, a 31.9% decrease from the previous year, with the adjusted operating margin shrinking by 272 basis points to 6.2%.

Financial Position

At the end of the fourth quarter of 2025, Integra held approximately $235 million in cash and cash equivalents, compared to $246.4 million a year earlier.

Net cash from operating activities for the year totaled $50.4 million, down from $129.4 million at the end of 2024.

2026 Outlook and Q1 Guidance

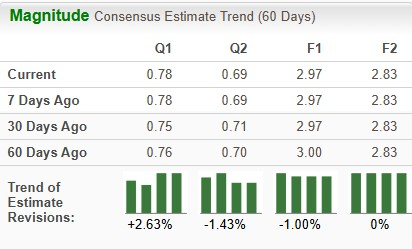

For the full year 2026, Integra anticipates revenue between $1.66 billion and $1.70 billion, representing growth of 1.6% to 4.1%. The Zacks Consensus Estimate stands at $1.68 billion, suggesting a 3% year-over-year increase.

Adjusted EPS is projected to range from $2.30 to $2.40, with the consensus estimate at $2.32 per share.

For the first quarter of 2026, the company expects revenue between $375 million and $390 million, compared to the consensus estimate of $395 million. Adjusted EPS is forecasted between $0.37 and $0.45, with the consensus at $0.43 per share.

Analysis and Company Progress

Integra closed the fourth quarter of 2025 with results that exceeded expectations for both earnings and revenue, despite year-over-year declines in both metrics.

During the quarter, the company made significant operational improvements and maintained a strong focus on serving customers and patients. Throughout 2025, Integra enhanced its quality management system, advanced its Compliance Master Plan, and made progress on remediation initiatives, strengthening its foundation for long-term operational success. Key achievements included improved supply reliability for Integra Skin products, healthier inventory levels, and the early relaunch of PriMatrix and Durepair.

However, the contraction in profit margins during the quarter remains a concern.

Zacks Rank and Notable Peers

Integra currently holds a Zacks Rank #3 (Hold).

Other medical sector stocks with higher Zacks rankings include:

- Intuitive Surgical (ISRG): Zacks Rank #1 (Strong Buy). Reported Q4 2025 adjusted EPS of $2.53, beating estimates by 12.4%, with revenue of $2.87 billion exceeding expectations by 4.7%. The company has a projected long-term earnings growth rate of 15.7%, outpacing the industry average of 12.7%, and has surpassed earnings estimates in each of the past four quarters with an average surprise of 13.24%.

- Cardinal Health (CAH): Zacks Rank #2 (Buy). Delivered Q2 fiscal 2026 adjusted EPS of $2.63, topping estimates by 10%, and revenue of $65.6 billion, up 0.9% over expectations. The company’s long-term earnings growth rate is 15%, compared to the industry’s 9.6%, and it has exceeded earnings estimates in the last four quarters with an average surprise of 9.3%.

- Align Technology (ALGN): Zacks Rank #2. Posted Q4 2025 adjusted EPS of $3.29, 10.1% above estimates, with revenue of $1.05 billion, 5.3% above consensus. The company’s estimated long-term earnings growth rate is 10.1%, compared to the industry’s 9.5%, and it has beaten estimates in three of the last four quarters, with an average surprise of 6.16%.

5 Stocks Poised for Significant Growth

Zacks analysts have identified five stocks with the potential to double in value in the coming months:

- Stock #1: A disruptive company demonstrating strong growth and resilience

- Stock #2: Positive indicators suggest a buying opportunity

- Stock #3: Considered one of the most attractive investments currently available

- Stock #4: A leader in a rapidly expanding industry

- Stock #5: A modern omni-channel platform ready for expansion

Many of these stocks are not yet widely recognized on Wall Street, offering early investment opportunities. Previous recommendations have achieved gains of +171%, +209%, and +232%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

XRP Price About To Enter ‘Face-Melting Phase’, And The Target Is $27

Keep An Eye on These 4 Bank Stocks With Recent Dividend Hikes

Keep An Eye on These 4 Bank Stocks With Recent Dividend Hikes

Pfizer Stock: Buy, Sell or Hold After Its 11% Rally So Far in 2026?