Fabrinet Eyes 800ZR and Co-Packaged Optics as Growth Catalysts

Fabrinet’s FN next-generation 800ZR is a clear upcoming trigger. These products have not yet ramped, making production timing an incremental catalyst as Datacenter Interconnect (DCI) demand is expected to accelerate sequentially in the third quarter of fiscal 2026. Beyond the near-term ramps, FN is engaged in co-packaged optics with three customers and is also involved in optical circuit switching, with timing tied to customer roadmaps.

Datacom transceiver builds for hyperscalers directly and for merchant vendors are positioned as “quarters away, not years” from meaningful revenue, with second-source approvals serving as a gating item. Building 10 and the Pinehurst conversion are intended to reduce bottleneck risk as demand builds, and both are being funded without debt. That capacity readiness also supports potential share gains tied to the company’s second-source position on the AWS-related High-Performance Computing program.

Fabrinet’s EMS Model Limits Downside

FN’s pure-play electronics manufacturing services (EMS) model avoids margin stacking and does not compete with customers’ products, a positioning that can support program wins and help limit downside when mix and utilization shift.

Investors should watch for milestones, including evidence of DCI acceleration, 800ZR entering production and datacom constraint easing that sustains sequential growth. Additional confirmation points include High-Performance Computing (HPC) automation qualification supporting scale and how forex-related volatility flows through quarterly results.

In the second quarter of fiscal 2026, HPC contributed $85.6 million, and management expects the current program to exceed $150 million per quarter within the next couple of quarters, with double-digit sequential growth guided for the third quarter of fiscal 2026.

Fabrinet Offers Positive Q3 Guidance

For fiscal third quarter, Fabrinet expects revenues in the $1.15-$1.20 billion range. Non-GAAP earnings are expected between $3.45 per share and $3.60 per share, with sequential growth expected in Telecom, Datacom and HPC.

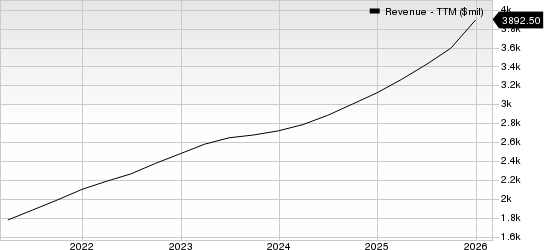

Fabrinet Revenue (TTM)

Fabrinet revenue-ttm | Fabrinet Quote

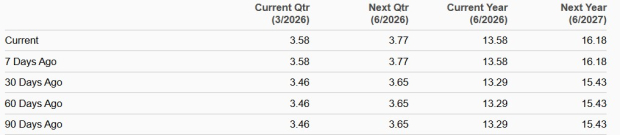

The Zacks Consensus Estimate for third-quarter fiscal 2026 revenues is currently pegged at $1.19 billion, indicating 36.2% growth from the figure reported in the year-ago quarter. The consensus estimate for the fiscal third quarter is pegged at $3.58 per share, up 3.5% over the past 30 days and indicating 42.1% growth from the figure reported in the year-ago quarter.

Consensus Estimate Trend

Image Source: Zacks Investment Research

Zacks Rank and Other Stocks to Consider

Fabrinet currently has a Zacks Rank #2 (Buy).

Advanced Energy Industries AEIS, Seagate STX and Western Digital WDC are some other top-ranked stocks in the broader Zacks Computer and Technology sector. All three stocks currently sport a Zacks Rank #1 (Strong Buy) each. Long-term earnings growth for Advanced Energy Industries, Seagate and Western Digital is pegged at 19.36%, 38.04% and 51.11%, respectively. In terms of share price movement, Advanced Energy Industries, Seagate and Western Digital have appreciated 215.1%, 292.7% and 486.7%, respectively, outperforming FN’s 192.1% return in a year.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Gold price to accelerate and hit new record highs after this event – technical analyst

Gold price to accelerate and hit new record highs after this event – technical analyst

The Zacks Analyst Blog Highlights Allstate, Koninklijke Philips and Heineken

Gold price to accelerate and hit new record highs after this event – technical analyst