3 Factors That Make TSLA a Risky Choice and One Alternative Stock to Consider

Tesla’s Recent Performance and Investor Considerations

Over the last half-year, Tesla’s stock has delivered a notable performance, surpassing the S&P 500 by 10.8%. The share price currently stands at $406.74, reflecting a 15.9% increase. Such gains may leave investors wondering about their next steps regarding Tesla’s stock.

Is this a good moment to invest in Tesla, or should you approach with caution before adding it to your holdings?

Why We Believe Tesla May Lag Behind

While it’s great to see investors benefit from Tesla’s rise, we remain cautious. Below are three reasons why we see more attractive opportunities elsewhere, along with a stock we prefer over Tesla.

1. Declining Demand and Falling Sales Volumes

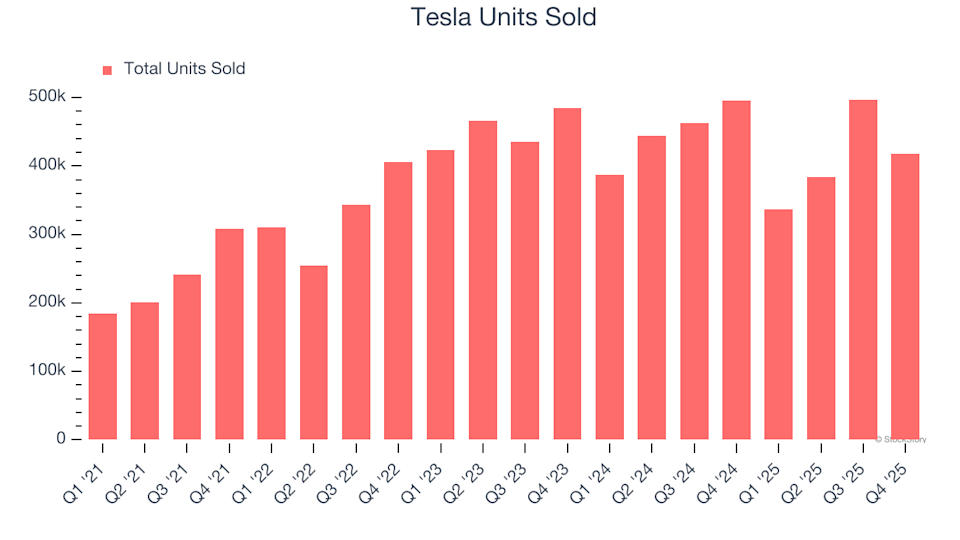

Revenue growth in the auto industry depends on both pricing and the number of vehicles sold. For car manufacturers, sales volume is especially critical, as there’s a limit to how much customers are willing to pay.

In the most recent quarter, Tesla sold 418,227 vehicles, representing a 4.9% annual decrease over the past two years. This downward trend suggests that Tesla may be facing stiffer competition or a saturated market. To boost growth, the company may need to cut prices or enhance its products—moves that could pressure short-term profits.

2. Shrinking Free Cash Flow Margins

Free cash flow, though not always highlighted in financial reports, is a crucial indicator because it reflects all operational and capital expenditures, making it difficult to manipulate. Ultimately, cash flow is vital for any business.

Over the past five years, Tesla’s free cash flow margin has dropped by 2.8 percentage points. Although there has been a recent uptick, investors are likely hoping for a return to historical levels. If the downward trend persists, it could indicate that Tesla is in the midst of heavy investment—possibly in new AI-driven ventures like robotaxis or humanoid robots. For the trailing twelve months, Tesla’s free cash flow margin was 6.6%.

3. New Investments Yet to Deliver as ROIC Falls

Return on invested capital (ROIC) measures how efficiently a company generates operating profit from its total capital base.

We favor companies with strong and improving ROIC. While Tesla’s ROIC has dipped recently due to price reductions, its longer-term trend remains positive, with current levels above those of previous years. This improvement is largely due to aggressive investments in AI opportunities. Whether these initiatives will translate into higher ROIC over time remains to be seen.

Our Verdict on Tesla

In our view, Tesla does not meet our quality criteria. Despite its recent outperformance, the stock is trading at a forward price-to-earnings ratio of 197.2 (or $406.74 per share), suggesting that much optimism is already factored in. At this valuation, we believe other companies offer stronger fundamentals.

Alternative Stocks to Consider

DON’T MISS: The Top 9 Stocks Outperforming the Market. The best-performing stocks consistently deliver strong results—time and again. These companies are characterized by impressive revenue growth, expanding free cash flow, and exceptional returns on capital. The market has already recognized their achievements.

Our AI-driven platform indicates that these stocks still have room to run. Discover which nine companies made our list this week—absolutely free.

Our selections include well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Tecnoglass, which delivered a 1,754% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Oil: Threats to Supply and Government Actions – Commerzbank

Gold: BNY reevaluates its safe haven status amid changing interest rates

Prediction markets have an insider trading problem