Position Shift: Crude Oil Snapped Up, Copper Neglected, 110,000 Short Positions Closed on 10-Year Treasury Bonds

Huitong Network, March 7 — According to data from the US Commodity Futures Trading Commission (CFTC), as of the week ending March 3, market speculators made significant changes in their positions across various financial products, revealing a subtle shift in market sentiment. Position data for precious metals, energy, foreign exchange futures, and US treasury bonds provide a window to discern market trends. Below is a detailed analysis of these key market position changes.

According to data from the US Commodity Futures Trading Commission (CFTC), as of the week ending March 3, market speculators made significant changes in their positions across various financial products, indicating a subtle shift in market sentiment. Position data for precious metals, energy, foreign exchange futures, and US treasury bonds offer insights into market trends. Below is a detailed analysis of these key position changes.

Precious Metals

Interpretation: The slight increase reflects a mild optimism toward gold’s safe-haven properties. The overall net long remains high, indicating relatively stable long-term bullish sentiment.

Interpretation: The slight reduction suggests a cooling in expectations for silver’s industrial demand. However, net longs remain positive, indicating speculators have not fully turned bearish.

Interpretation: The sizable reduction suggests short-term wavering in confidence on global economic recovery and industrial demand. Upward momentum in copper prices may face a test.

Energy

Interpretation: The substantial increase shows greater confidence in a medium-term oil price rebound, possibly driven by signals of tight supply or demand recovery. This was the most notable change in energy for the week.

Interpretation: The significant increase reflects optimism over seasonal gas demand or declining inventories, with market sentiment turning more bullish.

Foreign Exchange Futures

Interpretation: The euro remains the strongest bullish currency among FX futures, showing speculators continue to bet on the eurozone’s advantage over the US dollar.

Interpretation: The continued net short shows the market’s reduced reliance on the yen as a safe haven, with expectations for a strong US dollar persisting.

Interpretation: The large net short suggests cautious attitudes toward the UK’s economic outlook or policy uncertainty.

Interpretation: Persistent net shorts indicate weakening safe-haven demand for the Swiss franc amid a risk-on environment.

US Treasury Bonds

Overall Treasury futures (from a composite US Treasury perspective): Speculators' net long positions increased by 15,191 contracts to 20,265 contracts.

Interpretation: Turning net long with a slight increase signals speculators are warming to lower long-term rates or an economic slowdown, sending an overall bullish signal for treasuries.

Breakdown by maturities:

Interpretation: Short pressure has eased slightly, with short-term rate expectations stabilizing.

Interpretation: Sharply increased shorts indicate strong bets on higher medium-term yields.

Interpretation: The substantial reduction is the most significant change in treasuries this week, reflecting a clear relaxation in expectations for higher long-end rates.

Interpretation: The reduction suggests renewed appeal for long-duration bonds, with increased worries over recession or slowing inflation.

Agricultural Products

Interpretation: A large cut in shorts shows short covering or a shift in sentiment, with a marked recovery in corn market sentiment.

Interpretation: A slight reduction, but net longs remain high with an overall bullish outlook unchanged.

Interpretation: Heavier shorts reflect dominant expectations of supply pressure or weak demand.

Interpretation: The reduction in shorts shows weakening confidence in bearish positions, allowing for potential short-term rebound.

Interpretation: The sharp reduction shows enhanced market expectation for a price bottom in sugar.

Interpretation: A marginal increase, maintaining low net longs with limited sentiment change.

Interpretation: Shorts continue to increase, with supply-side pressures likely to remain dominant.

This week’s CFTC data shows speculators are clearly more bullish on crude oil, natural gas, the euro, and overall treasuries, while copper, silver, most agricultural products, as well as currencies like the pound, franc, and yen, maintain or deepen net shorts. The most significant change in treasuries is a reduction of shorts at the long end, reflecting a phase of market adjustment in response to expectations for a soft economic landing, easing inflation, and a strong US dollar.

FAQ

A: Net long WTI crude oil increased by 16,794 contracts to 97,851 contracts, the largest single long addition of the week. This indicates speculators are most confident in an oil price rebound, often a leading indicator of shifts in supply-demand expectations or geopolitical risks and a bellwether for overall commodity sentiment.

A: Overall treasury futures’ net longs rose to 20,265 contracts, indicating a bullish bias (expectations for lower rates), but sharp increases in 5-year shorts and major reductions in 10-year and ultra-long shorts suggest the curve is flattening or medium-term rates remain under upward pressure, while recession worries are rising at the long end. This divergence often signals growing market disagreement on the Fed’s future path.

A: The euro is the only FX future with a large-scale net long, suggesting speculators see the eurozone as more resilient relative to the US, or they’re betting on a pullback in the high US dollar index. The pound, franc, and yen net shorts show the market still sees the US dollar as a strong currency and increased risk appetite is weighing on traditional safe havens.

A: Divergences between copper and crude oil are common when economic expectations diverge: more crude oil longs reflect optimism over energy demand or supply tightness, while the cut in copper longs signals a lack of confidence in global manufacturing recovery in industrial metals, possibly dragging on by China’s demand or trade issues. Further convergence between the two merits attention.

A: The large reduction in corn shorts (still net short by 55,485 contracts) is the sharpest shift among agricultural products this week, typically indicating technical short-covering or long inflows driven by improving weather or inventory data. If the reduction continues, it could signal a temporary bottom, but this should be validated with actual supply-demand reports.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

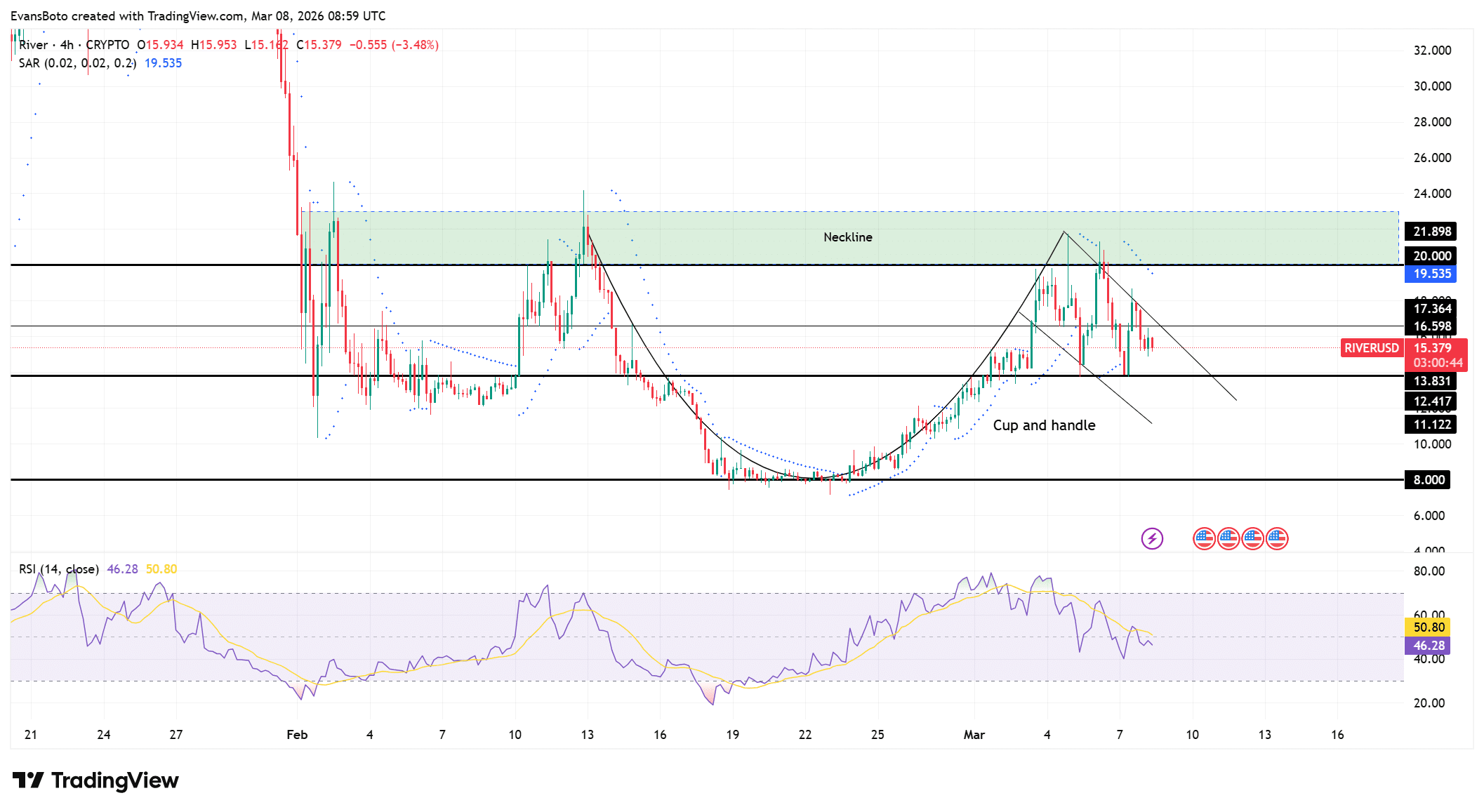

River crypto primed for $20 breakout? THIS structure hints at…

Strategy could buy Bitcoin again

Finance job openings at 2012 levels, US lost 92K jobs last month

Why Monero (XMR) Price Is Down Today: Key Drivers Explained