Underwriting as Software: How On-Chain Innovations Break Open the Black Box of Traditional Capital Formation

The power of underwriting is shifting from banks to on-chain protocols.

Written by: Prathik Desai

Translation: Block unicorn

In 1688, a coffee house on London’s Tower Street became one of the most important venues in global commerce. Captains, shipowners, and merchants would walk into Edward Lloyd’s coffee house with a slip of paper describing the cargo, route, and vessel. They needed someone to bear the risks of the voyage. Those willing to take on part of the risk would sign below the slip. That’s where the term "underwriting" comes from.

The most powerful person in the room was the one who set the terms for ship tickets, including the premiums charged, the risks assumed, and the voyages they chose to support. No ship could set sail before this person had assessed the risk of its maiden voyage.

This arrangement helped the coffee house evolve over three centuries from a social gathering spot into Lloyd’s of London—one of the world’s largest insurance markets. Interesting, right? When I started reading this story, I discovered an insight that still holds true: any asset, project, or tradable thing needs a moment when someone decides: "this is worth supporting, at this price, under these terms."

Every time a new asset class emerges, we see this pattern repeatedly.

About two centuries after Edward’s coffee house was built, we saw J.P. Morgan underwrite stock for companies like the New York Central Railroad, supporting US publicly funded rail projects. This established Morgan’s reputation as a capital mobilizer and railroad finance expert.

His underwriting set the terms, picked investors, and profited from the spread between the issuer’s paid price and the public offering price. If Morgan refused to underwrite a project, it would not get built.

Modern IPOs are a digital version of the same mechanism. A handful of banks underwrite a company’s initial public offering (IPO), gauge demand from major clients, set the offer price, and allocate shares. The first-day "pop," meaning a 20-30% price surge, isn’t just a market phenomenon—it reflects the profit margin for underwriters.

For four centuries, investors’ only complaint was that insiders got the best allocations, initial pricing rarely reflected true demand, and the rest only entered after the spread had been captured.

Last week, James Evans released the HIP-6 proposal for token launch auctions on Hyperliquid, partly in response to these complaints. He disclosed on X that he held $HYPE tokens and collaborated with early-stage crypto VC Reciprocal Ventures.

In today’s deep dive, I’ll assess HIP-6 and other on-chain platforms to evaluate whether they can address persistent issues in capital formation.

Where Things Went Wrong

The book-building process that dominates traditional capital formation is inherently designed as a black box. Banks gauge demand from institutional clients behind closed doors, set prices based on conversations retail markets never know about, and allocate shares to "random" accounts. The issuer gets the offering price, and the public gets the leftovers.

Let’s look at two examples.

During Facebook’s (now Meta) IPO in 2021, lead underwriter Morgan Stanley lowered revenue projections during the investor roadshow. This negative news was immediately communicated to major institutional clients via analyst reports, while retail investors remained completely unaware. Facebook’s stock dropped nearly 50% in three months. Retail investors were hit the hardest: they were allocated the stock at an inflated price yet had no access to insider information.

A more recent example is Rivian’s 2021 IPO as an EV manufacturer. The IPO priced at $78/share, and on day one, soared to $179. Institutional clients with allocations from Goldman Sachs and J.P. Morgan captured the spread, while retail investors bought at open. Subsequently, Rivian’s share price fell about 40% within ten days. Investors later sued the company for allegedly concealing that its vehicle prices were below material costs. Rivian eventually agreed to a $250 million settlement but insisted it did not admit fault. Today, Rivian’s stock hovers below $16/share.

This approach has become so normalized as a business model that ordinary investors don’t even notice its flaws.

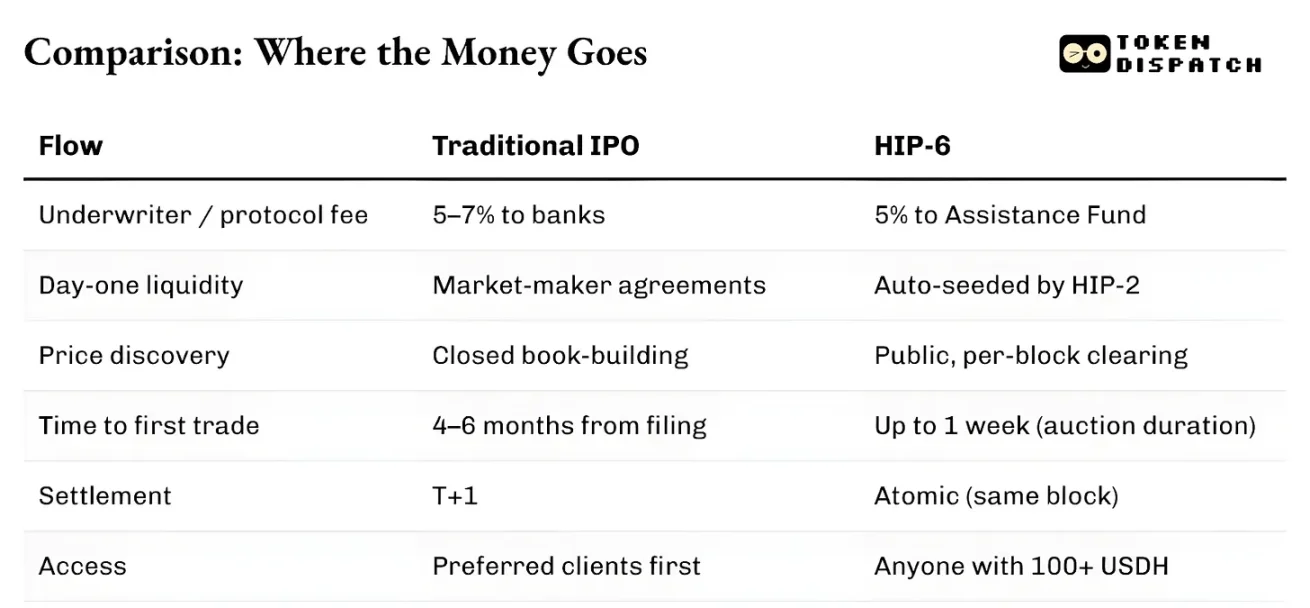

Beyond allocation, the infrastructure underpinning the entire system is slow and siloed. From submitting IPO paperwork to first trade, a listing typically takes four to six months. Settlement requires a full trading day. Assets can’t be used as collateral until clearing is done. Market makers operate under separate agreements that often come with spread guarantees. The entire system is also restricted by jurisdiction, so even if non-US retail investors are willing to take the same risks, they can’t participate in a New York IPO on equal terms.

The underwriters’ power comes precisely from these frictions. Inefficiencies like opaque pricing, slow settlement, and access barriers are utilized and turned into moats.

What Could On-Chain Underwriting Change?

On-chain underwriting is structurally different, with fewer intermediaries. Bonding curves or Continuous Clearing Auctions (CCA) publicly post all bids in real-time. On-chain liquidity is programmatically enabled from the first block. It’s hard-coded into the launch mechanism by calculation, not negotiation. Assets can exist, trade, and be used as collateral within the same block. There’s no waiting for T+1 or settlement cycles.

Gatekeeping still exists, but in different forms.

Pump.fun’s launches are open to anyone with sufficient wallet balance. Echo’s sales require KYC but allow participation from different jurisdictions. Hyperliquid’s HIP-6 sets a $100 minimum economic threshold but doesn’t limit by qualification. All these systems avoid the "priority customer" allocation approach of most traditional book-building processes.

The biggest difference is that on-chain underwriting treats each token sale as a purchase order for the ecosystem’s native token (whether SOL, USDC, USDH, or others). Traditional underwriting, other than fees, does not create any other form of ongoing demand.

This distinction matters more than you might think.

On March 20, 2025, Solana’s mainstream token launch platform pump.fun launched its own automated market maker (AMM), PumpSwap. Before this, all tokens graduating from pump.fun’s bonding curve were routed to Raydium, Solana’s largest decentralized exchange. This inflow became one of Raydium’s most important revenue sources. Overnight, this pipeline was cut off.

Raydium’s AMM revenue was estimated to have dropped by 35-40%. Its RAY token fell 30%. Raydium didn’t stand by: it responded by launching its own token launch product, LaunchLab, within 48 hours. RAY’s price briefly doubled in six months, then crashed to a two-year low. Since pump.fun launched its AMM, RAY’s price is down about 70%.

The lesson: Whoever controls where tokens are launched, controls downstream fee revenue. Launch means order flow.

The Two Paths to Token Creation

The subsequent pattern has been a split into two distinct paths.

One path is market formation—generating tradable charts at internet speed. Pump.fun is the best example, with a bonding curve, a $69,000 graduation threshold, and automatic liquidity injection via PumpSwap. It has generated nearly $1.5 billion in fees, launched over 16.8 million tokens, and uses over 98% of revenue to buy back its PUMP token, offsetting more than 27% of circulating supply.

The other is capital formation—structurally allocating capital to real users with compliance safeguards in place. In October 2025, Coinbase acquired Echo for $375 million, adding a KYC-based token sale platform with time-weighted deposits to its product line. Echo’s Sonar product is the opposite of pump.fun, taking a regulated, identity-verified, lead investor–driven approach.

Coinbase’s solution falls short on launch liquidity. Echo handles distribution but does not automatically bootstrap a trading market.

Where The Two Roads Converge

The HIP-6 proposal is the latest attempt to merge the two paths into a single protocol-level primitive.

The proposed mechanism is a Continuous Clearing Auction (CCA) embedded in the HyperCore consensus layer. In each block, the system uses a model based on the remaining block budget difference to calculate the clearing price using all valid bids.

This module isn’t entirely new. HIP-6 explicitly adopts Uniswap’s CCA module, which debuted in November 2025, first used by Aztec Network to raise $60 million from more than 17,000 bidders with no evidence of sniping or automation-based manipulation.

Both implementations share the same core concept: break a large auction into thousands of block-ordered mini-auctions, release tokens gradually, calculate a uniform clearing price per block, make bids within price bands irrevocable to prevent price collusion, and inject liquidity automatically at settlement.

This design solves the same legacy problems.

Fixed-price sales force investors to guess the correct opening price. Pro-rata allocations lead to vicious cycles of oversubscription. Dutch auctions enable professionals to game timing. CCA eliminates all three. In a CCA, the final seed price is the volume-weighted average collected during the closing window—an anti-manipulation measure making price manipulation very expensive.

The difference between Hyperliquid and Uniswap lies in their settlement architecture.

HIP-6 runs natively inside HyperCore’s consensus layer. Auction logic is executed inside the block transition function, not as an external contract. Settlement happens at the same layer as order matching.

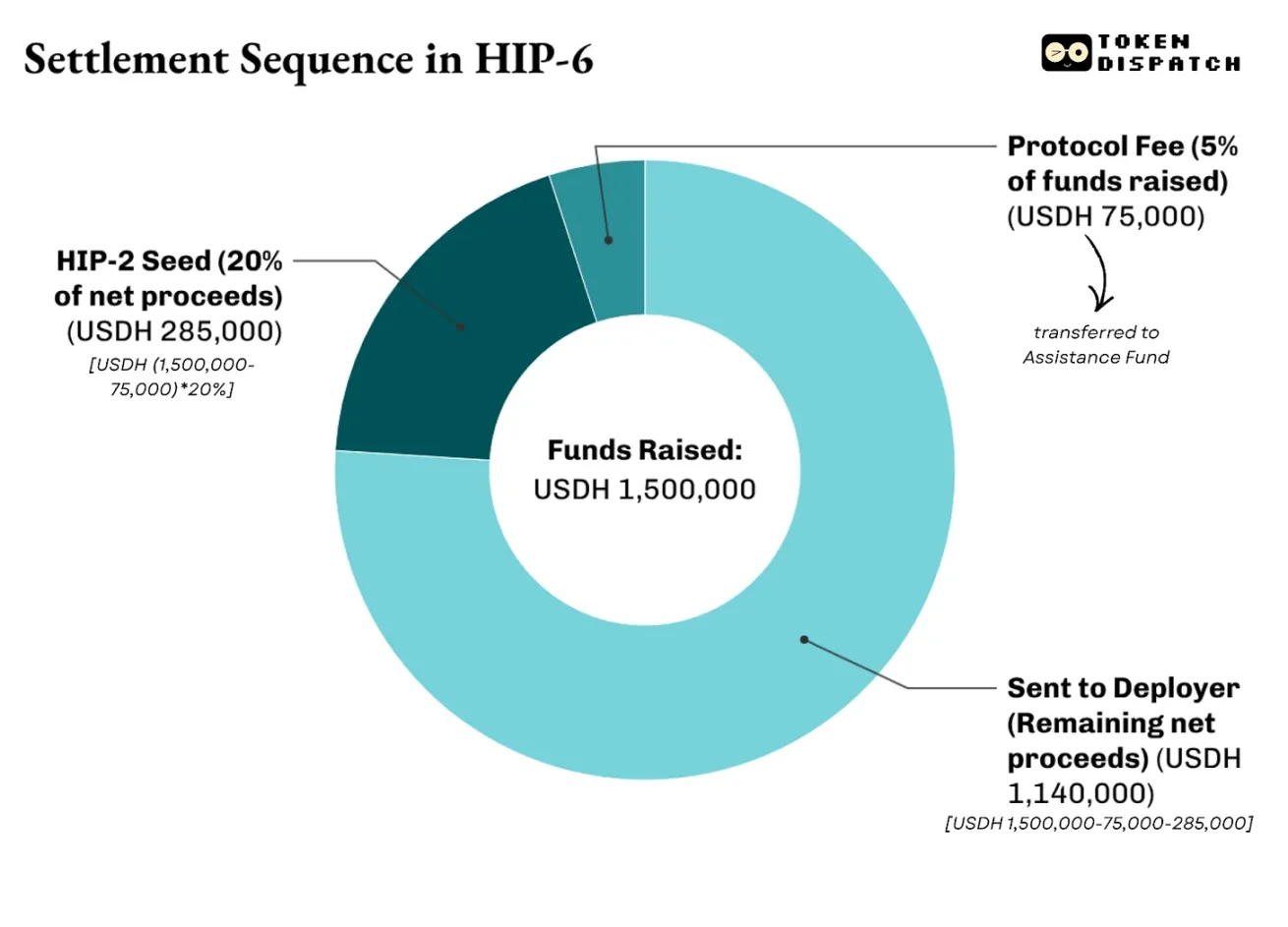

Settlement will be multi-tiered. The proposal states a 500 basis point protocol fee will be taken from total funds raised, going to an aid fund, which Hyperliquid uses for all $HYPE buybacks. Of the net proceeds (post-fee), 2,000–10,000 basis points (20–100%) will be used to bootstrap the HIP-2 market at the derived price. The rest is paid to the deployer.

For example, a $PROJ token auction on HIP-6 raises $1.5 million USDH for 10 million tokens, with 20% as HIP-2 seed funds. Settlement looks like this:

This is precisely where HIP-6 differs from Uniswap.

Uniswap builds CCA as a token launch tool, used to pipe funds into its existing AMM pools. With HIP-6, Hyperliquid is a full-stack infra: stakeholders can raise funds, discover prices, establish bilateral liquidity, and start trading on a central limit order book (CLOB).

More importantly, all of this is denominated in the asset the protocol wants you to hold—USDH (USD 1000).

Outstanding Issues

Although transparent price discovery, programmatic liquidity, and atomic settlement represent a clear upgrade over traditional models, on-chain underwriting carries its own problems.

None of these mechanisms fix project quality. Pump.fun’s bonding curve ensures price fairness but says nothing about the credibility of the project behind the token. HIP-6 acknowledges this very flaw. There’s nothing about token quality, governance, or holder protection.

Traditional underwriters bear reputational and legal responsibility for failed offerings. Seeing a bank’s name on a prospectus indicates a stakeholder vetted the issuer. On-chain mechanisms can’t provide a similar accountability route. Coinbase’s Echo gets closer with KYC, issuer disclosure, and sale restrictions, but reintroduces the access barriers on-chain underwriting aims to eliminate.

In most major jurisdictions, it remains unresolved whether a token launch constitutes a securities offering. A softer US enforcement environment has made permissionless launches easier, but underlying legal uncertainty hasn’t disappeared.

Still, it’s early days; I expect future iterations to become a better choice than legacy capital formation systems.

In finance, entities that control where assets originate always capture the most persistent fees.

Between 2012–2021, Goldman Sachs led more US IPOs than any other bank. But its benefits reached beyond the massive IPO fee haul. Once Goldman did an IPO, it was also likely to be lead adviser for follow-on offerings, M&A, and debt issues for the same firm.

We observe the same pattern with pump.fun: by providing a reliable platform and generating 16.8 million tokens, it has hauled in over $1 billion in revenue. Raydium’s crash mirrored this: once it lost control of token generation, 35–40% of revenue vanished overnight.

With on-chain underwriting, the system remains unchanged—the players shift. It’s no longer a bank or syndicate, but a protocol. The protocol provides a transparent, auditable token distribution process, with no need for insider relationships.

In return, it expects you to transact in a unit that contributes to the protocol’s treasury: its native token. I believe this is a worthwhile trade for investors. Steady demand for the native token leads to lockup of circulating capital, increasing liquidity.

This intensifies competition not just between traditional and on-chain underwriting, but also among on-chain players. The contest has shifted from secondary market share to control: who sets the opening price, allocates the first tokens, and decides what currency investors must use.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Silver Price Forecast: XAG/USD remains below $58.00 amid Fed hawkish pause

The Fed Decided to Do Nothing and That Decision Backfired: Here’s Why

AUD/USD Price Forecast: Struggles near 0.6950 as bears retain control below 100-EMA on H4