Coeur Mining Shares Surge 340% Over the Last Year: What Factors Are Fueling This Growth?

Coeur Mining's Impressive Market Surge

Over the past year, Coeur Mining, Inc. (CDE) has experienced a remarkable share price increase of 341.3%. This performance far outpaces the 88.2% gain seen in the broader Mining-Non Ferrous sector and the S&P 500’s 23.2% advance during the same period.

Other companies in the sector, such as First Majestic Silver Corp. (AG) and Hecla Mining Company (HL), have also posted substantial gains, rising 365.4% and 295.9% respectively over the last twelve months.

Comparing Price Trends: CDE, Industry, S&P 500, AG, and HL

According to technical analysis, CDE has consistently traded above both its 50-day and 200-day simple moving averages, with the shorter-term average trending above the longer-term one—a classic indicator of bullish momentum.

Let’s delve into CDE’s core business metrics for a deeper understanding of its recent performance.

Operational Advancements Fueling Production Growth

In the fourth quarter of 2025, Coeur Mining delivered robust production results, achieving 112,429 ounces of gold and 4.7 million ounces of silver—representing year-over-year increases of 29% and 47%, respectively. These improvements were driven by higher ore grades and the ongoing ramp-up of key assets.

The Rochester Mine was a standout contributor, benefiting from its expansion project. During the quarter, the mine processed approximately 6.4 million tons of ore and placed 9.3 million tons on the leach pad, resulting in 17,722 ounces of gold and 1.75 million ounces of silver.

Kensington Mine also saw gold output climb to 29,567 ounces, up nearly 10% from the previous year, thanks to improved grades and increased milling rates.

At the Wharf Mine, gold production dipped sequentially to 24,759 ounces due to a fire at the tertiary crusher, which temporarily limited capacity. Nevertheless, this figure was higher than the 21,976 ounces produced in the same quarter last year.

Palmarejo Mine maintained steady results, producing 25,662 ounces of gold and 1.6 million ounces of silver, while the recently acquired Las Chispas Mine added 14,719 ounces of gold and 1.4 million ounces of silver, supported by strong grades.

Overall, Coeur’s fourth-quarter output highlights the positive impact of its ongoing operational improvements and strategic asset integration, setting the stage for continued growth.

Strengthening Financial Position Through Cash Generation

During the fourth quarter, Coeur generated $374.6 million in operating cash flow, a significant jump from $64 million a year earlier. This was driven by higher production, increased sales, and favorable gold and silver prices. Free cash flow for the quarter reached approximately $313 million.

By the end of 2025, the company’s cash and equivalents had soared to $553.6 million—a 904% increase year-over-year—while total debt was reduced to about $340.5 million, down 42% from the end of 2024. The debt-to-capital ratio dropped to 9.3% from 34.3%.

Coeur also continued its share repurchase program, buying back around $2.3 million in shares during the quarter, for a total of $9.6 million in 2025. Capital expenditures for the quarter were $61.4 million, with 78% allocated to sustaining operations and the remainder to development projects.

This strong financial performance gives Coeur greater flexibility to fund new growth initiatives and pursue strategic acquisitions.

Growth Driven by New Projects and Acquisitions

Coeur advanced several major projects and initiatives in the fourth quarter of 2025, reinforcing its long-term growth strategy. The ongoing expansion at the Rochester Mine has positioned it as one of the leading primary silver producers in the U.S., with increased ore processing capacity and improved recovery rates.

The acquisition of SilverCrest Metals brought the high-grade Las Chispas Mine into Coeur’s portfolio, adding a valuable source of gold and silver production and enhancing the company’s exposure to high-grade underground mining.

Work also continues at the Silvertip Project, where exploration and development efforts are focused on assessing the potential restart of its high-grade silver-lead-zinc deposit.

Additionally, Coeur has announced plans to acquire New Gold Inc., a deal expected to close in the first half of 2026. This acquisition would add the New Afton and Rainy River mines, further diversifying Coeur’s asset base across gold, silver, and copper production.

Upward Earnings Revisions Signal Optimism

Analyst expectations for CDE’s earnings in 2026 and 2027 have been revised upward over the past two months.

The current consensus projects earnings of $1.95 per share for 2026, representing a 144% increase from the prior year. For 2027, earnings are estimated at $1.83 per share, indicating a slight year-over-year decrease of 6%.

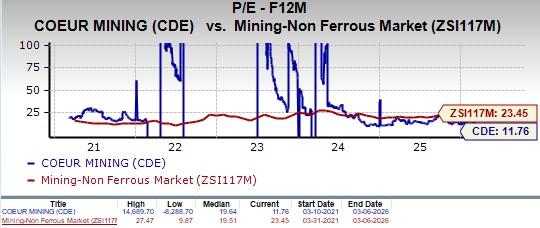

Valuation: CDE Trades at a Discount

CDE’s forward 12-month price-to-earnings ratio stands at 11.76, which is below the industry average of 23.45 and its own five-year median.

For comparison, First Majestic (AG) and Hecla Mining (HL) have forward P/E ratios of 3.29 and 11.23, respectively.

In terms of value metrics, CDE holds a Value Score of C, while AG and HL both have a score of F.

Conclusion: Hold Rating for Coeur Mining

Coeur Mining continues to build operational momentum and strengthen its financial position, supported by rising production, robust cash flow, and significant debt reduction. Expansion projects like Rochester and the integration of Las Chispas are set to further enhance its long-term growth prospects.

Nonetheless, operational risks remain, as evidenced by the temporary production setback at the Wharf Mine following a fire. With CDE trading at a lower valuation than its industry peers, current shareholders may consider holding their positions while keeping an eye on the company’s operational execution and growth initiatives.

CDE currently carries a Zacks Rank of #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Reflecting on Q4 Results for Personal Loan Stocks: Affirm (NASDAQ:AFRM)

Ethereum Foundation to stake 70K ETH as network staking nears one-third of supply

Consumers anticipated minimal shifts in inflation prior to the Iran conflict

Ether holds $2K as traders make push toward overhead short liquidity