Reflecting on Q4 Results for Personal Loan Stocks: Affirm (NASDAQ:AFRM)

Personal Loan Stocks: Q4 Performance Overview

As earnings season wraps up, it's an opportune moment to identify promising stocks and evaluate how companies are navigating the current economic landscape. Here’s a summary of how Affirm (NASDAQ:AFRM) and its peers in the personal loan sector performed in the fourth quarter.

Industry Snapshot

Companies in the personal loan space provide unsecured loans to meet a variety of consumer needs. This industry is bolstered by streamlined digital applications, growing consumer trust in online finance, and the ability to serve customers who may not have access to traditional credit. However, these businesses face challenges such as managing credit risk, adhering to regulatory requirements, and contending with fierce competition from both established banks and fintech newcomers, all of which can put pressure on profit margins.

Q4 Results Across the Sector

Among the eight personal loan providers monitored, the group collectively delivered a robust fourth quarter. Revenue figures surpassed Wall Street expectations by 2.3%, though guidance for the next quarter came in 0.9% below consensus forecasts.

Despite these positive results, share prices have struggled, with the group’s average stock price declining by 7% since the latest earnings announcements.

Q4 Laggard: Affirm (NASDAQ:AFRM)

Affirm, established by Max Levchin—one of PayPal’s co-founders—aims to offer transparent and fair financial products. The company enables consumers to make purchases and pay over time through clear, flexible installment plans.

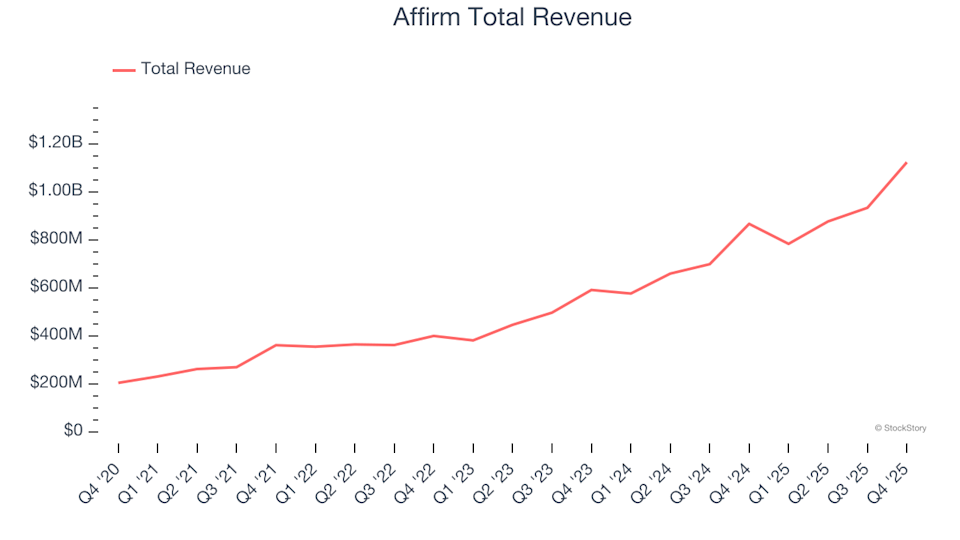

For Q4, Affirm posted $1.12 billion in revenue, marking a 29.6% increase year over year and beating analyst projections by 6.3%. While the company outperformed on EBITDA, it fell short on EPS, resulting in a mixed quarter overall.

Affirm delivered the largest revenue beat among its peers, yet investor sentiment remained negative. The stock has dropped 17.4% since the earnings release and is currently trading at $51.62.

Curious if Affirm is a buy at these levels?

Q4 Standout: Sezzle (NASDAQ:SEZL)

Launched in 2016 to provide younger consumers with an alternative to credit cards, Sezzle allows shoppers to divide their purchases into four interest-free payments over six weeks at participating merchants.

Sezzle reported $129.9 million in revenue for the quarter, a 32.2% year-over-year increase and 2.7% above analyst expectations. The company exceeded estimates for both EPS and EBITDA, making it a standout performer this quarter.

The market responded positively, with Sezzle’s stock rising 17.4% since the earnings announcement. Shares are now trading at $73.52.

Thinking about investing in Sezzle?

Other Notable Performers

OneMain (NYSE:OMF)

With roots dating back to 1912, OneMain Holdings specializes in personal loans, auto financing, and credit cards for nonprime borrowers who may not qualify for traditional banking products.

OneMain’s Q4 revenue reached $1.28 billion, an 8.8% year-over-year increase and in line with analyst forecasts. The company narrowly beat net interest income expectations but posted the slowest revenue growth among its peers. Its stock has declined 14.3% since the results and is now at $54.15.

SoFi (NASDAQ:SOFI)

Originally founded in 2011 to refinance student loans, SoFi Technologies has evolved into a comprehensive digital financial platform, offering lending, banking, investing, and more to help members manage their finances.

SoFi reported $1.01 billion in revenue for Q4, up 37% year over year and 2.7% above analyst estimates. The company also provided full-year EPS guidance that exceeded expectations and delivered a strong EBITDA beat. However, its full-year outlook was the weakest among its competitors. Shares have fallen 23.9% since the earnings report and currently sit at $18.55.

LendingClub (NYSE:LC)

Once a pioneer in peer-to-peer lending, LendingClub has transitioned into a digital bank, connecting borrowers and lenders for personal loans, auto refinancing, and banking services.

LendingClub’s Q4 revenue came in at $266.5 million, a 22.7% increase year over year and 1.8% above analyst projections. The company also provided full-year EPS guidance above expectations and outperformed on revenue. Despite these results, the stock has dropped 25.5% since the report and is now trading at $14.59.

Market Context

The Federal Reserve’s interest rate hikes in 2022 and 2023 have helped bring inflation closer to the 2% target. Remarkably, the economy has avoided a recession, leading to cautious optimism about a soft landing. Recent rate cuts—a half-point in September 2024 and a quarter-point in November—have further boosted markets, especially after the November election results drove major indices to record highs. Still, investors face uncertainties around tariffs, corporate tax policy, and the economic outlook for 2025.

Looking for companies with strong fundamentals? Explore our Top 5 Quality Compounder Stocks—these businesses are well-positioned to thrive regardless of political or economic shifts.

The StockStory analyst team, comprised of experienced professional investors, leverages data-driven analysis and automation to deliver timely, high-quality market insights.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

ARIA (Aria.AI) fluctuated by 49.4% in 24 hours: Trading volume surged by 796%, driving intense price volatility

DeFi Withdrawals Underscore Changing Investor Attitudes and Infrastructure Issues

Dogecoin eyes $0.111 after $0.0872 retest – But DOGE’s move holds IF…

Workers Cling to Their Positions Amid Sluggish Hiring and Increasing Layoffs