Winners And Losers In Q4: How West Pharmaceutical Services (NYSE:WST) Compared To Other Drug Development Inputs & Services Stocks

Q4 Review: Drug Development Inputs & Services Stocks Performance

As the latest earnings season wraps up, it's a perfect opportunity to reflect on which companies excelled and which struggled. Here, we examine the Q4 results for drug development inputs and services stocks, beginning with West Pharmaceutical Services (NYSE:WST).

Industry Overview

Firms that provide inputs and services for drug development are vital to the pharmaceutical and biotech sectors. Their offerings—ranging from drug discovery support to preclinical testing and manufacturing—are in steady demand, as many pharmaceutical companies outsource these specialized tasks through long-term agreements. While this creates a stable revenue base, the industry faces challenges such as significant capital needs, reliance on a limited number of clients, and sensitivity to changes in R&D spending or regulatory shifts. Looking forward, the sector stands to benefit from rising investments in biologics, cell and gene therapies, and precision medicine, all of which require advanced tools and services. The trend toward outsourcing for greater agility and cost savings continues to support industry growth. However, ongoing efforts to control healthcare costs may lead to pricing pressures, and regulatory changes could slow innovation or dampen client activity.

Q4 Earnings Snapshot

Among the eight drug development inputs and services companies we monitor, Q4 results were mixed. Collectively, these companies surpassed revenue expectations by 1.5%.

Despite the revenue beats, share prices have struggled, with the group’s average stock price falling 12.4% since their earnings announcements.

West Pharmaceutical Services (NYSE:WST)

Established in 1923, West Pharmaceutical Services plays a pivotal role in the pharmaceutical supply chain by producing specialized packaging, containment solutions, and delivery systems for injectable medications and healthcare products.

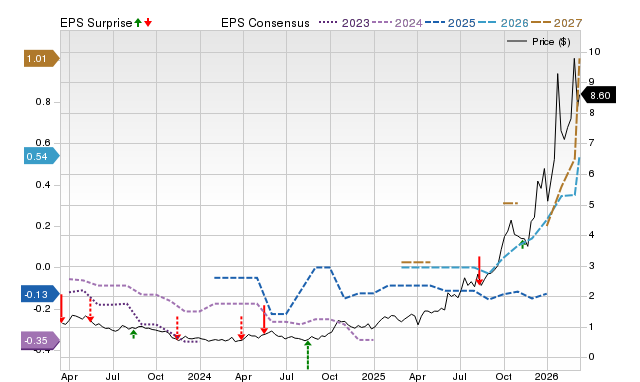

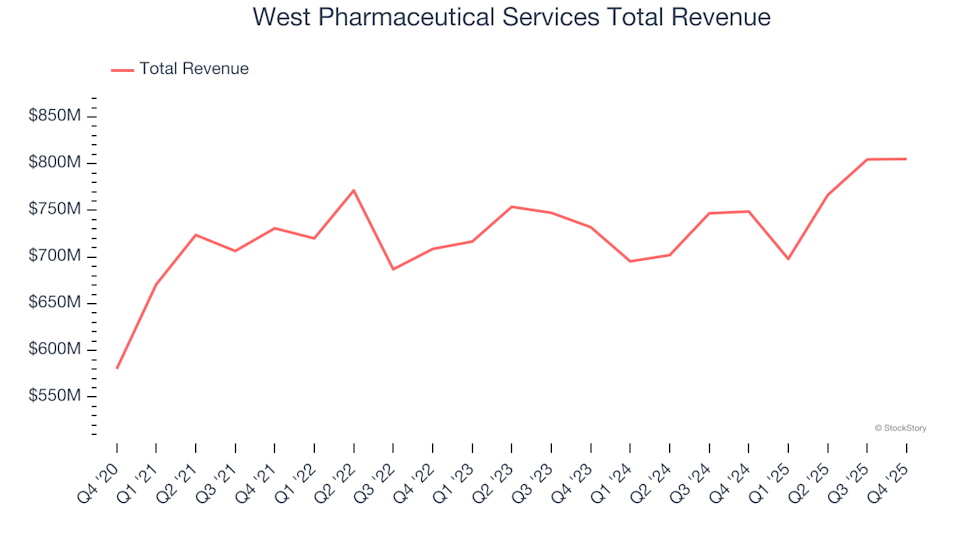

In Q4, West Pharmaceutical Services posted $805 million in revenue, marking a 7.5% increase from the previous year and exceeding analyst forecasts by 1.5%. The company also outperformed expectations for both full-year and quarterly EPS.

Eric M. Green, President, CEO, and Board Chair, commented: “Our strong finish to 2025 was a result of the team's relentless execution of our growth strategy.”

Despite these positive results, West Pharmaceutical Services’ stock has declined 5% since the report and is currently trading at $233.84.

Top Performer in Q4: Medpace (NASDAQ:MEDP)

Founded in 1992, Medpace set out to offer a science-driven alternative to traditional contract research organizations. The company provides outsourced clinical trial management and research services to pharmaceutical, biotech, and medical device firms developing new therapies.

Medpace reported Q4 revenue of $708.5 million, a 32% year-over-year increase and 3.3% above analyst expectations. The company delivered robust results, surpassing both organic revenue and full-year EPS guidance estimates.

Medpace led its peers with the largest revenue beat and fastest growth, yet its stock has dropped 12% since the earnings release, now trading at $466.87.

Q4 Laggard: Fortrea (NASDAQ:FTRE)

Fortrea, which became independent from Labcorp in 2023, focuses solely on clinical research services. The company supports pharmaceutical, biotech, and medical device clients in bringing new products to market through clinical trials and related services.

For Q4, Fortrea reported $660.5 million in revenue, a 5.2% decline from the prior year and 0.9% below analyst projections. The company also missed full-year revenue and EPS guidance by a significant margin.

Fortrea recorded the weakest performance among its peers, with the slowest revenue growth and the most disappointing guidance update. Its stock has fallen 12% since the earnings announcement and is now at $9.10.

Repligen (NASDAQ:RGEN)

Since 2012, Repligen has expanded its bioprocessing capabilities through more than 13 strategic acquisitions. The company develops and manufactures advanced technologies to enhance the efficiency and adaptability of biologic drug production.

Repligen’s Q4 revenue reached $197.9 million, up 18.1% year over year and 2.7% above analyst expectations. While the company beat organic revenue estimates, it fell short on full-year EPS guidance.

Shares of Repligen have dropped 10.1% since the earnings release, with the stock now priced at $121.66.

Azenta (NASDAQ:AZTA)

Azenta specializes in safeguarding critical biological materials, offering sample management, storage, and genomic services to help pharmaceutical and biotech companies preserve and analyze essential research assets.

In Q4, Azenta reported $148.6 million in revenue, unchanged from the previous year but 1.1% above analyst forecasts. However, the company missed EPS expectations by a wide margin.

Azenta’s stock has tumbled 38.2% since the earnings report and is currently valued at $22.80.

Looking for High-Quality Growth Stocks?

If you’re interested in companies with strong fundamentals and momentum, explore our Strong Momentum Stocks list. These businesses are well-positioned to thrive regardless of economic or political shifts.

The StockStory analyst team—comprised of experienced professional investors—leverages quantitative analysis and automation to deliver timely, high-quality market insights.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Leonardo DRS, Inc. (DRS) Shows Promising Technical Prospects Following Significant Golden Cross

PBR Allocates $28.7 Million to Libra Rocks Initiative to Enhance Mero Field Studies

Preformed Line Products Q4 Profit Declines, Revenue Increases 4% Year Over Year