Vertiv Stock Slides 1.07% Amid 42nd-Ranked $1.98 Billion Trading Volume Despite 19% Revenue Surge and Upbeat 2026 Guidance

Market Snapshot

On March 12, 2026, Vertiv HoldingsVRT-1.07% (VRTX) closed with a 1.07% decline, trading at $265.38 per share. The stock saw a trading volume of 7.45 million shares, amounting to $1.98 billion in total value—a rank of 42nd in market activity for the day. This decline followed a mixed performance in recent months, with the stock hitting a 52-week high of $266.67 earlier in the session. The pullback came despite strong revenue growth and upbeat guidance for 2026, reflecting investor caution ahead of the April 29 earnings report.

Key Drivers

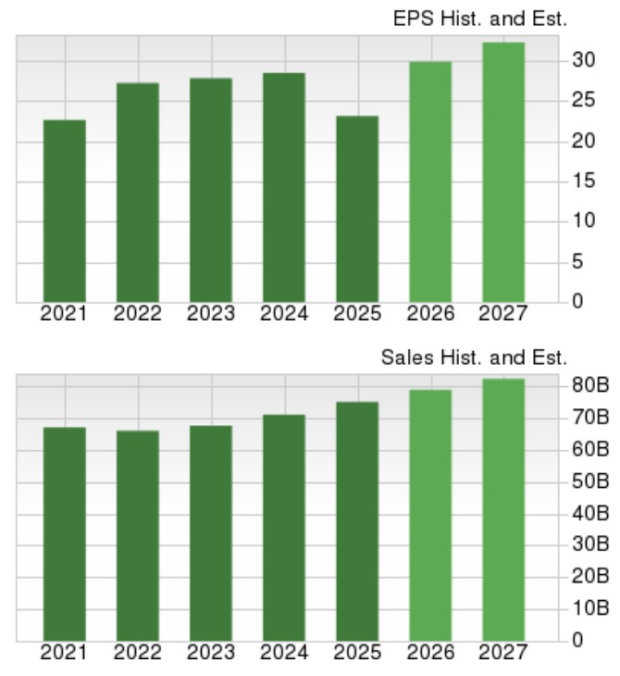

Vertiv’s recent earnings report and strategic updates highlight both momentum and challenges shaping its stock performance. The company reported Q4 2025 revenue of $2.88 billion, a 19% year-over-year increase, but fell short of analyst expectations for EPS of $1.30, delivering $1.14 instead. However, adjusted diluted EPS rose 37% YoY, driven by cost discipline and operational efficiency. The earnings miss was partially offset by a record $15 billion backlog, doubling from the prior year, and the launch of new products such as OneCore and SmartRun, which position VertivVRT-1.07% to capitalize on AI infrastructure demand.

The stock’s pre-market surge of 17.07% to $233.70—despite the earnings shortfall—underscored investor confidence in the company’s long-term prospects. Executives, including CEO Gio Albertazzi and Chairman Dave Cote, emphasized optimism about future growth, with Albertazzi stating the company is “excited about future prospects” and Cote declaring “We ain’t done yet.” This sentiment was reinforced by 2026 guidance projecting adjusted diluted EPS of $6.02 (a 43% increase) and net sales of $13.5 billion with 28% organic growth. These figures signal robust expectations for market share expansion, particularly in data center cooling and power solutions.

Analyst activity further fueled market dynamics. Mizuho, Barclays, and Deutsche Bank upgraded their price targets, with Mizuho raising its objective to $290 and Barclays to $281, reflecting confidence in Vertiv’s AI-driven infrastructure offerings. Conversely, Wolfe Research downgraded the stock to “peer perform,” highlighting valuation concerns. The stock’s forward P/E ratio of 43x—well above the industry average of 14.1x—suggests investors are paying a premium for anticipated growth. Analysts also noted Vertiv’s strong earnings surprises in the last four quarters, including a 37% beat in Q4 2025, as a key differentiator in a competitive sector.

A dividend announcement on March 12 added to the stock’s appeal. Vertiv declared a quarterly dividend of $0.0625 per share, payable on March 26, with an ex-dividend date of March 17. This represents a 7.33% payout ratio and a 0.1% yield, aligning with the company’s strategy to return value to shareholders amid its growth phase. However, the dividend’s modest size and the stock’s elevated valuation metrics—such as a trailing P/E of 77.82 and a PEG ratio of 1.33—highlight the balance between growth optimism and value skepticism.

While the stock’s 1.07% decline on March 12 suggests short-term profit-taking, the broader narrative remains one of resilience. Vertiv’s ability to secure a record backlog, innovate in high-growth areas, and outperform revenue forecasts despite EPS misses demonstrates its adaptability in a rapidly evolving market. The company’s focus on AI infrastructure, coupled with strategic product launches and strong leadership messaging, positions it to benefit from the second wave of AI adoption, even as valuation metrics remain a point of contention among analysts.

Outlook and Strategic Context

Looking ahead, Vertiv’s performance will hinge on its execution against 2026 guidance and the broader AI infrastructure cycle. The company’s 28% organic sales growth target implies continued demand for its cooling and power solutions, particularly as hyperscale data centers expand to meet AI workloads. However, competition from peers like Genpact and industry-wide margin pressures could test its ability to maintain profitability. Investors will closely monitor upcoming earnings reports and product adoption rates to gauge whether the stock’s premium valuation is justified by sustained growth. For now, the mix of strong fundamentals, strategic momentum, and analyst optimism suggests Vertiv remains a key player in the AI infrastructure ecosystem, even as its stock navigates near-term volatility.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

UAI (UnifAINetwork) 24-hour amplitude 69.5%: Trading volume surges over 140% driving price rebound

XRP ETF Posts $6M Outflow While Bitcoin ETFs Attract Inflows

Asian stocks slide as Iran war keeps oil near $100, dents rate-cut bets

Lockheed Martin and RTX Shares: Emerging Cornerstones of Contemporary Defense