WDAY or IBM: Which Enterprise Software Company Is the Superior Investment Choice Today?

Comparing Workday and IBM: Leaders in Enterprise Cloud Solutions

Workday, Inc. (WDAY) and International Business Machines Corporation (IBM) are both prominent names in the enterprise software and cloud technology sectors, serving large-scale organizations worldwide. Workday is recognized for its cloud-based platforms that unify human resources and financial management, enabling businesses to streamline operations and gain actionable insights. Meanwhile, IBM delivers a broad spectrum of cloud and data services, supporting companies in their digital transformation journeys. Its offerings include hybrid cloud solutions, advanced IT infrastructure, quantum and supercomputing, enterprise software, and storage technologies.

This analysis explores the competitive positioning of both companies to determine which may hold a stronger place in the current market landscape.

Workday’s Strengths and Challenges

Workday has been steadily expanding its offerings beyond its core human capital management products, venturing into financial solutions and tailoring its services for various sectors such as education, government, and finance. This diversification has resulted in high customer retention and a growing client base, as organizations seek to optimize spending and boost efficiency. Notably, Workday’s Prism Analytics and Adaptive Insights planning tools are gaining traction, contributing to its consistent customer growth. Strategic partnerships, such as those with Alight for integrated payroll solutions in Europe and collaborations with AWS Marketplace, have further extended Workday’s reach.

The company is also heavily investing in artificial intelligence and machine learning, embedding these technologies into its products to enhance automation, decision-making, and productivity. Recent innovations include Workday Illuminate, which leverages generative AI to provide workforce insights.

However, Workday’s revenue remains heavily concentrated in the United States, accounting for about 75% of its total income. This limited geographic diversification exposes the company to regional economic and regulatory risks. Additionally, intense competition from established players like Oracle has led to pricing pressures, while rising operational and marketing expenses continue to impact profit margins.

IBM’s Opportunities and Hurdles

IBM is well-positioned to capitalize on the growing demand for hybrid cloud and AI-driven solutions, which are fueling growth in its Software and Consulting divisions. The increasing adoption of cloud-native workloads and generative AI is prompting enterprises to manage more complex and dynamic IT environments, driving demand for IBM’s hybrid cloud offerings. The recent acquisition of HashiCorp has further strengthened IBM’s capabilities in managing intricate cloud infrastructures, complementing its Red Hat portfolio and enhancing its multi-cloud strategy.

Despite these advantages, IBM faces stiff competition from major cloud providers such as Amazon Web Services (AWS) and Microsoft Azure. This competitive landscape has led to margin compression and inconsistent profitability. The company’s ongoing transition from traditional business models to cloud-based services is a lengthy and challenging process, and fluctuations in foreign exchange rates add another layer of risk.

Financial Outlook: Zacks Estimates for Workday and IBM

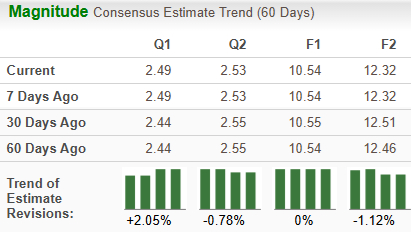

According to Zacks, Workday’s projected sales and earnings per share (EPS) for fiscal 2027 suggest annual increases of 11.6% and 14.2%, respectively, with EPS estimates remaining steady over the past two months.

Source: Zacks Investment Research

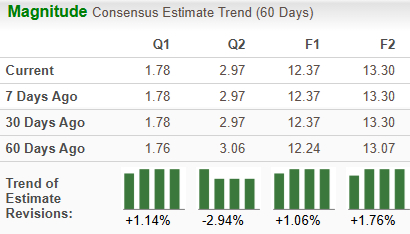

For IBM, forecasts for 2026 indicate expected year-over-year growth of 5.5% in sales and 6.7% in EPS, with EPS estimates rising by 1.1% in the last 60 days.

Source: Zacks Investment Research

Stock Performance and Valuation

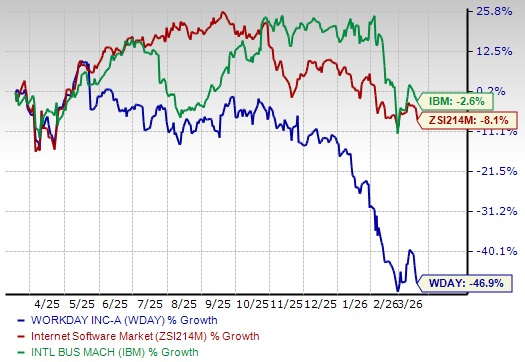

In the past twelve months, Workday’s stock has declined by 46.9%, significantly underperforming its industry’s average drop of 8.1%. IBM, by contrast, has seen a more modest decrease of 2.6% over the same period.

Source: Zacks Investment Research

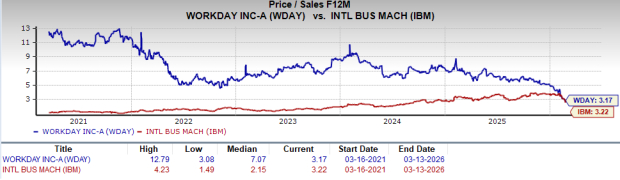

From a valuation perspective, Workday appears slightly more appealing. IBM’s forward price-to-sales ratio stands at 3.22, just above Workday’s 3.17.

Source: Zacks Investment Research

Which Stock Is the Better Choice?

Both Workday and IBM currently hold a Zacks Rank #3 (Hold). While both are expected to see improvements in sales and earnings this fiscal year, IBM has demonstrated stronger stock performance and more favorable estimate revisions, albeit at a slightly higher valuation. Workday has maintained consistent revenue and EPS growth, whereas IBM’s results have been more volatile. Investors seeking rapid growth and exposure to the expanding SaaS market may prefer Workday, while those looking for a diversified technology investment might lean toward IBM. Overall, IBM appears to have a slight advantage across several key metrics, making it a potentially stronger investment at this time.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Gold-Backed Tokens Power Surging Tokenized Commodity Market

Canadian Dollar Outlook: USD/CAD opens the week on a downward trend after the release of Canada’s CPI figures

Simmons First National (SFNC) Might Be an Excellent Option

Why ENGIE BRASL EGA (EGIEY) Stands Out as an Excellent Dividend Stock Today