Is American Express Worth Buying Now Even With Its High Valuation?

American Express Valuation Compared to Industry Peers

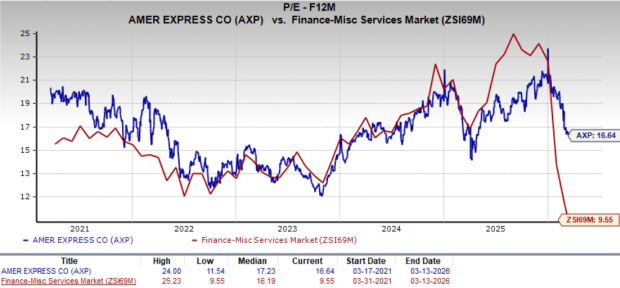

American Express Company (AXP) is currently valued at a forward price-to-earnings ratio of 16.64, which is notably higher than the industry average of 9.55. However, this figure is still below the company’s five-year median of 17.23, indicating that its current valuation premium is not excessive when viewed against its historical standards.

In contrast, major competitors such as Visa Inc. and Mastercard Incorporated are trading at even loftier forward P/E multiples of 22.55 and 24.89, respectively. This disparity highlights the fundamental differences in their business structures. While Visa and Mastercard primarily serve as payment networks with minimal credit risk, American Express integrates issuing, lending, and network operations within a single platform.

Image Source: Zacks Investment Research

Market Headwinds Impacting Payment Companies

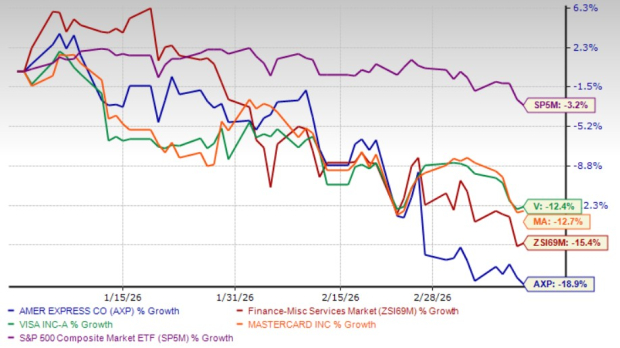

Shares of American Express have dropped 18.9% so far this year, reflecting a broader downturn in the payments sector. Both Visa and Mastercard have also experienced declines as investors reevaluate growth prospects. The S&P 500 has fallen by approximately 3.2% year-to-date, weighed down by concerns over slowing consumer spending and ongoing economic uncertainty.

There is growing caution among investors regarding the potential impact of new technologies, such as artificial intelligence, on employment trends and long-term consumer behavior. Additionally, persistent geopolitical tensions are likely to keep inflation elevated, which could dampen discretionary spending and reduce transaction volumes across the payments industry.

Stock Performance: AXP, Visa, Mastercard, Industry & S&P 500

Image Source: Zacks Investment Research

Strengths of American Express

Despite the challenging environment, the negative sentiment toward American Express may be somewhat overstated. Unlike many payment firms that depend on broad consumer spending, AmEx benefits from a clientele with higher incomes, who tend to maintain spending even during economic downturns.

Recent data points to increasing revolving loan balances, consistent growth in card fees, and ongoing expansion in cardholder spending—all of which support a positive revenue outlook. This resilience in spending helps buffer the company against fluctuations in consumer activity.

American Express distinguishes itself with a vertically integrated model, acting as both a card issuer and a payment network. This allows the company to capture a greater share of transaction value and maintain stronger profit margins. The integrated approach also provides valuable data, enabling AmEx to tailor rewards, enhance customer engagement, and reinforce its premium brand image.

Looking forward, the company is targeting affluent Gen Z and Millennial consumers, who typically spend more on travel, dining, and lifestyle experiences—areas where AmEx’s rewards programs are especially competitive. As these younger customers’ incomes grow, they are expected to become significant, long-term contributors to the company’s revenue. By engaging them early, AmEx aims to foster lasting relationships that will drive future growth.

Earnings Outlook and Performance Surprises

Analyst consensus projects that American Express will achieve earnings per share of $17.50 in 2026, representing a 13.8% increase, with another 14.5% growth anticipated for 2027. Over the longer term, earnings are expected to rise at a mid-teens percentage rate. The company has surpassed earnings estimates in three of the past four quarters, with an average positive surprise of 3.9%.

Revenue is forecast to climb 9% year-over-year in 2026 to reach $78.7 billion, followed by an additional 8.2% increase in 2027.

Potential Risks Facing American Express

While American Express holds a strong position in the market, several challenges persist. The company is more reliant on the U.S. market than competitors like Visa and Mastercard, both of which have established extensive international payment networks. AmEx’s growth is closely tied to card lending and spending volumes, which could make it slower to adapt to emerging payment technologies that are transforming the industry.

Because AmEx acts as both a card issuer and a payment network, it is directly exposed to credit risk from its customers. This dual role requires diligent management of both operational performance and the quality of its loan portfolio, especially during periods of economic instability.

Operating costs are also on the rise. Total expenses increased to 73.6% of revenues in 2025, up from 72.6% in 2024, largely due to higher spending on rewards and customer engagement. Rewards and cardmember services alone made up nearly 46% of total expenses.

Leverage remains a concern as well. As of December 31, 2025, American Express reported $57.8 billion in debt, with a long-term debt-to-capital ratio of 62.8%, which is significantly higher than the industry average of 42.7%. Interest expenses related to long-term debt and other borrowings rose by 10% in 2025.

Conclusion

In summary, American Express continues to exhibit strong business fundamentals despite recent market turbulence. While its valuation is above the industry average, it remains below its historical median and is still less expensive than Visa and Mastercard. The company’s affluent customer base, integrated payments model, and consistent spending trends provide a solid foundation for long-term growth. However, rising costs, credit risk, and elevated leverage levels should be closely monitored in the current uncertain economic climate.

With steady earnings growth projected but some structural risks present, American Express currently holds a Zacks Rank #3 (Hold), indicating that investors may wish to wait for clearer signs of momentum before making new investments.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

IWM Options Indicate Bearish Sentiment Under $240 — Strategies for Navigating the Volatility

GrabAGun Expands Market Presence Amid Firearm Industry Slowdown, Driven by Superior Logistics and Online Ease

Here’s why these specialists recommend investing in energy stocks instead of the S&P 500 at this moment