2 Reasons to Appreciate COF and 1 Reason for Caution

Capital One’s Recent Stock Performance

Over the past six months, Capital One has experienced a significant decline, with its share price falling by 20.3% since September 2025, now standing at $179.85. This drop has been influenced in part by weaker quarterly earnings, prompting investors to reconsider their positions.

With this recent downturn, could this present a favorable entry point for those interested in COF?

What Makes Capital One a Topic of Discussion?

Founded in 1988 as a credit card provider, Capital One (NYSE:COF) has evolved into a full-scale financial institution. Today, it delivers a range of services including credit cards, auto financing, banking, and commercial loans to both individuals and businesses.

Positive Aspects of Capital One

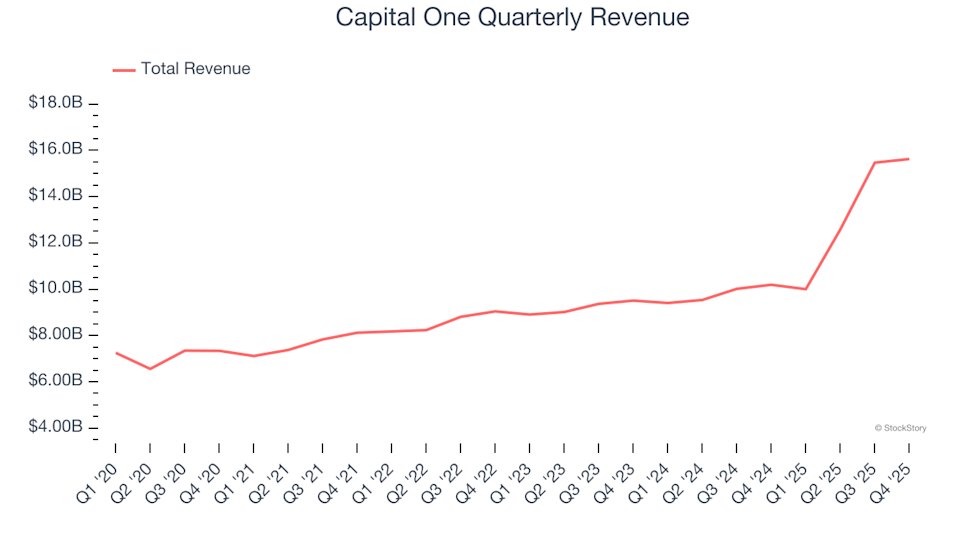

1. Impressive Long-Term Revenue Expansion

Assessing a company’s track record over several years can reveal its underlying strength. While many firms may see brief periods of growth, the most successful ones maintain momentum over the long haul.

Capital One has achieved an annualized revenue increase of 13.5% over the past five years, outpacing the average for its sector. This consistent growth indicates that its products and services continue to appeal to customers.

2. Robust Long-Term EPS Growth

Looking at the growth in earnings per share (EPS) over time helps determine if a company’s additional sales are translating into real profits, rather than being driven by heavy spending on marketing or promotions.

Capital One’s EPS has climbed at a compounded annual rate of 27.6% in the last five years, outstripping its revenue growth. This suggests the company has become more efficient and profitable for each share as it has scaled up.

A Cautionary Note

Stagnant Tangible Book Value Per Share (TBVPS)

Tangible book value per share (TBVPS) is a key indicator of the real value of a company’s equity, excluding intangible assets like goodwill that may not hold value in adverse situations.

For Capital One, TBVPS has only grown by 2.7% annually over the past five years. More concerning, this figure has barely budged in the last two years, remaining around $100.98 per share, signaling a halt in asset growth.

Overall Assessment

Despite some concerns, Capital One’s strengths outweigh its weaknesses. Following the recent price drop, the stock is trading at 8.8 times forward earnings, or $179.85 per share. Is this the right moment to invest?

Other Stocks Worth Considering

Don’t Miss: This Week’s Top 6 Stock Picks — The current market environment is quickly distinguishing high-quality stocks from overpriced ones. With AI rapidly reshaping entire industries, having more than just a list of promising companies is essential.

Our AI-driven platform identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia prior to its 1,178% climb. Each week, it highlights six new stocks that meet the same rigorous criteria.

Our recommendations have included well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Comfort Systems, which delivered a 782% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Ether is Down Over 60% From Its 2025 High, But TradFi Isn’t Walking Away— Here’s Why

JPMorgan Chase (JPM): Should You Buy, Sell, or Hold After Q4 Results?

Coherent’s InP Expansion Is the Critical Infrastructure Play for AI’s Next S-Curve—But Can It Scale Fast Enough?