3 Reasons to Steer Clear of WSC and One Alternative Stock Worth Buying

WillScot Mobile Mini: Recent Performance and Outlook

Investors in WillScot Mobile Mini have faced a challenging half-year, with the share price falling by 22.1% to $17.68. This decline can be attributed in part to weaker-than-expected quarterly results, prompting many to reconsider their investment strategy.

Is WillScot Mobile Mini a smart addition to your portfolio, or does it carry more risk than reward?

Reasons for Caution with WillScot Mobile Mini

Although the current share price may seem attractive, we are choosing to stay on the sidelines for now. Below are three key concerns about WSC, along with an alternative stock we prefer.

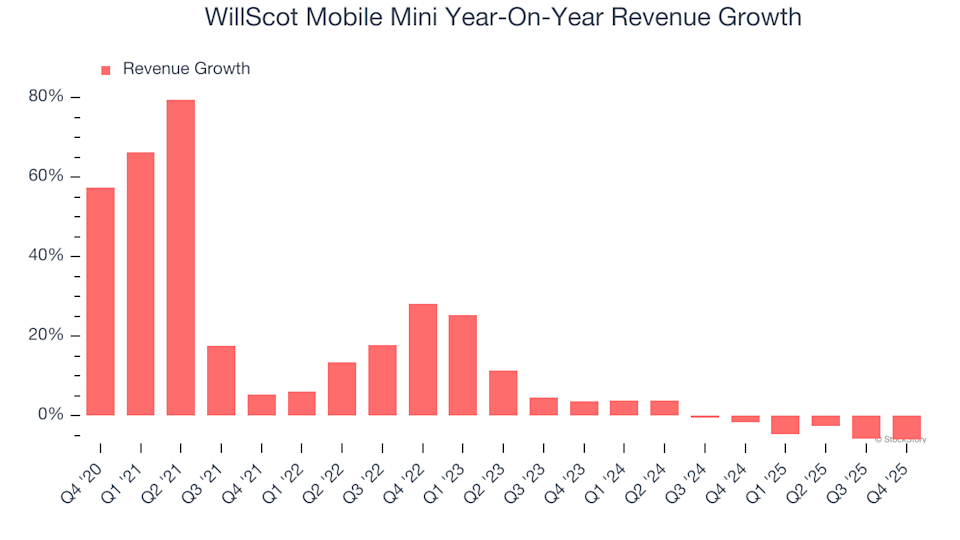

1. Declining Revenue

At StockStory, we prioritize sustainable long-term growth. However, in the industrial sector, focusing solely on long-term trends can overlook important industry cycles or unique opportunities such as major contract wins. WillScot Mobile Mini has recently diverged from its five-year pattern, with revenue decreasing at an average annual rate of 1.8% over the past two years.

2. Falling Operating Margins

Operating margin is a crucial indicator of a company's profitability, reflecting the percentage of revenue remaining after covering core expenses such as production costs, marketing, and salaries. This metric is particularly useful for comparing companies with varying debt and tax structures, as it excludes interest and tax expenses.

WillScot Mobile Mini's operating margin has dropped by 10.5 percentage points over the last five years. This downward trend is concerning, especially since revenue growth should typically improve cost efficiency and boost margins. For the most recent 12 months, the company reported an operating margin of 8%.

3. Earnings Per Share on the Decline

Tracking changes in earnings per share (EPS) over time helps determine if a company's additional sales are translating into real profits, rather than being driven by heavy spending on marketing or promotions.

Unfortunately, WillScot Mobile Mini's EPS has fallen by an average of 1.6% per year over the past five years, despite a 10.8% annual increase in revenue. This indicates that the company has become less profitable on a per-share basis as it has grown.

Our Verdict

While we appreciate companies that deliver value to their customers, we are not optimistic about WillScot Mobile Mini at this time. After the recent drop, the stock is trading at a forward P/E ratio of 16.7 (or $17.68 per share). Although this valuation is not excessive, we do not see significant upside potential right now. There are more promising opportunities available. For example, consider exploring .

Top Stocks for Every Market Environment

Don't Miss: This Week's Top 6 Stock Picks. The current market is quickly distinguishing high-quality stocks from overpriced ones, with AI-driven shifts impacting entire industries overnight. In such a fast-moving environment, a simple list of good companies isn't enough.

Our AI-powered system identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia before its 1,178% climb. Each week, we highlight six new stocks that meet our rigorous criteria.

Our selections have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Exlservice, which delivered a 354% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why April Might Mark the Breakthrough Rivian Shareholders Have Anticipated

2 Undervalued Stocks We’re Tracking and 1 That Falls Short

Bull of the Day: Sanmina (SANM) 改写后: Top Stock Pick Today: Sanmina (SANM)

uCloudlink Group Inc. Sponsored ADR (UCL) Announces Fourth Quarter Loss, Falls Short of Revenue Projections