J&J versus Merck: Crucial Considerations Investors Should Evaluate at This Moment

Comparing Johnson & Johnson and Merck: A Closer Look at Two Healthcare Leaders

Johnson & Johnson (JNJ) and Merck (MRK) are two of the most prominent names in the American healthcare sector, making them natural choices for a side-by-side evaluation.

Both companies have established themselves in areas such as oncology, immunology, and neuroscience. Johnson & Johnson, however, offers a more extensive range of products, including treatments for cardiovascular and metabolic conditions, pulmonary hypertension, infectious diseases, and a robust medical devices division.

Merck, on the other hand, is particularly strong in vaccines, virology, and acute hospital care.

As both companies face looming patent expirations and changes from the Medicare Part D overhaul, investors may wonder which stock currently presents a better opportunity. Examining their fundamentals, growth prospects, and potential risks can provide valuable insight.

Johnson & Johnson: Strengths and Challenges

Johnson & Johnson’s diversified structure, with operations in both pharmaceuticals and medical devices, is a key advantage. The company operates over 275 subsidiaries and has 28 products or platforms each generating more than $1 billion in annual sales. This broad base helps J&J weather economic fluctuations. The company also enjoys strong cash flow and has increased its dividend for 63 consecutive years.

The Innovative Medicine division has shown steady growth, with a 4.1% organic sales increase in 2025, despite the loss of exclusivity for Stelara and the impact of Medicare Part D changes. Leading drugs such as Darzalex, Erleada, and Tremfya, along with new launches like Carvykti, Tecvayli, Talvey, Rybrevant, and Spravato, have fueled this momentum.

The MedTech segment has also seen improvement over the last three quarters, driven by acquisitions like Abiomed and Shockwave, as well as growth in Surgical Vision and wound closure products. Electrophysiology has contributed to this positive trend, with MedTech sales up 4.3% organically in 2025.

In 2025, J&J made significant progress in its research pipeline, achieving important clinical and regulatory milestones. Notable approvals include Inlexzoh/TAR-200 for high-risk non-muscle invasive bladder cancer and Imaavy (nipocalimab) for generalized myasthenia gravis. The company invested over $32 billion in R&D and acquisitions, including Intra-Cellular Therapies and Halda Therapeutics.

J&J anticipates that 10 of its new or pipeline products in the Innovative Medicine segment could each reach peak sales of $5 billion, including Talvey, Tecvayli, Imaavy, Caplyta, Inlexzo, Rybrevant, Lazcluze, and Icotyde.

Despite these strengths, J&J faces challenges such as ongoing litigation related to talc products, the patent expiration for Stelara, upcoming loss of exclusivity for Opsumit and Simponi, and weaker performance in the MedTech segment in China.

Merck: Opportunities and Risks

Merck’s portfolio includes more than six blockbuster drugs, with Keytruda being the primary revenue driver. Keytruda, approved for multiple cancer types, accounts for about 55% of Merck’s pharmaceutical sales and has been central to the company’s consistent revenue growth. In 2025, Keytruda generated $31.7 billion in sales, a 7% increase from the previous year.

Keytruda’s expansion into earlier-stage cancer indications and continued strength in metastatic settings are fueling its growth. Merck expects this momentum to continue until the drug’s patent expires in 2028.

To support Keytruda’s long-term prospects, Merck is pursuing various strategies and expects the drug to reach peak sales of $35 billion by 2028. Other oncology products, such as Welireg, Lynparza (in partnership with AstraZeneca), and Lenvima (with Eisai), are also contributing to revenue growth.

Merck’s Animal Health division is another important growth driver, with expectations for sales to more than double by the mid-2030s.

The company’s late-stage pipeline has nearly tripled since 2021, thanks to both internal development and acquisitions. Promising new products include Capvaxive, a 21-valent pneumococcal conjugate vaccine, and Winrevair for pulmonary arterial hypertension, both of which have had successful launches and are expected to generate substantial long-term revenue.

In response to Keytruda’s upcoming patent expiration, Merck has been active in acquisitions. The 2025 purchase of Verona brought Ohtuvayre, a novel maintenance therapy for chronic obstructive pulmonary disease, which has started strong commercially. In January 2026, Merck acquired Cidara Therapeutics, adding MK-1406, a long-acting antiviral agent currently in late-stage trials for influenza prevention in high-risk individuals.

However, Merck is experiencing declining sales for Gardasil, its second-largest product, particularly in China due to weak demand amid economic slowdown. Gardasil’s outlook for 2026 remains subdued. Other vaccines, including Proquad, M-M-R II, Varivax, Rotateq, and Pneumovax 23, also saw lower sales in 2025. Additionally, demand for diabetes treatments (Januvia/Janumet) is falling, and some drugs are facing generic competition.

Merck’s heavy reliance on Keytruda raises concerns about future growth in its non-oncology segments, especially as the drug approaches loss of exclusivity in 2028. Competition is also intensifying, with new dual PD-1/VEGF inhibitors like Summit Therapeutics’ ivonescimab potentially challenging Keytruda’s dominance.

Nevertheless, Merck’s new product launches, pipeline advancements, and expansion into respiratory and infectious diseases through acquisitions have strengthened its long-term outlook.

Comparing Analyst Estimates for JNJ and MRK

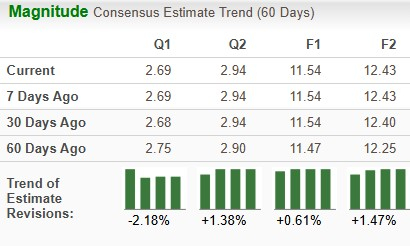

For 2026, analysts expect Johnson & Johnson’s sales and earnings per share to rise by 6.5% and 7.0%, respectively. Over the past two months, consensus earnings estimates for 2026 have increased from $11.47 to $11.54 per share, and for 2027 from $12.25 to $12.43.

JNJ Estimate Trends

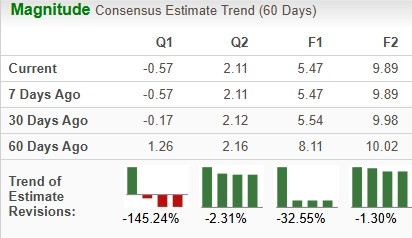

For Merck, the consensus forecast for 2026 points to a 2.6% increase in sales but a 39% drop in earnings per share. EPS estimates for both 2026 and 2027 have declined significantly over the last 60 days.

MRK Estimate Trends

Stock Performance and Valuation

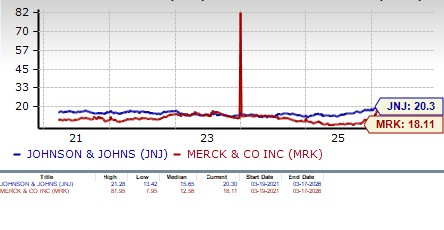

In the past year, Johnson & Johnson’s stock price has climbed 46.0%, while Merck’s shares have gained 23.2%. Both outperformed the broader pharmaceutical industry’s 10.6% growth.

From a valuation perspective, Merck appears more appealing. Johnson & Johnson currently trades at a forward price/earnings ratio of 20.30, above the industry average of 17.65 and its five-year average of 15.65. Merck’s forward P/E is 18.11, also higher than the industry and its own five-year average of 12.58.

Johnson & Johnson offers a dividend yield of 2.18%, while Merck’s yield is slightly higher at 2.93%.

Which Stock Is the Better Choice?

Both Merck and Johnson & Johnson currently hold a Zacks Rank #3 (Hold), making it a close call for investors.

Merck’s portfolio is anchored by Keytruda, one of the world’s top-selling drugs, and its pipeline includes several promising candidates. However, the company faces near-term headwinds, including ongoing challenges for Gardasil in China, potential competition for Keytruda, and increased generic pressure on some products. Recent estimate reductions are also linked to acquisition-related expenses.

In contrast, Johnson & Johnson exceeded financial expectations in 2025 and is optimistic about maintaining strong momentum in 2026, targeting approximately $100 billion in revenue. The company anticipates higher sales growth across both major divisions next year.

With its strong price performance, rising analyst estimates, steady earnings and revenue growth, positive outlook for 2026, successful new product launches, rapid pipeline progress, and ongoing acquisitions, Johnson & Johnson stands out as the stronger pick compared to Merck.

Special Report: Capitalizing on the Next AI Boom

The upcoming wave of artificial intelligence innovation is expected to generate massive wealth for early investors, potentially adding trillions to the global economy and transforming many aspects of daily life.

Those who invested in companies like Nvidia at the right time have seen substantial returns.

However, the explosive growth of the initial AI leaders may soon plateau, paving the way for a new group of innovative companies to drive the next phase of exponential growth.

Zacks’ report, AI Boom 2.0: The Second Wave, highlights four lesser-known companies that could become the next stars in the AI sector.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why First American Financial (FAF) Stands Out as a Leading Dividend Choice for Investors

SouthState's Organic Expansion Robust: What Drives Revenue Growth?

ACM or BCKIY: Which Stock Offers Greater Value?

PIPR vs. CRCL: Which Stock Offers Greater Value at This Moment?